{kind=link}

A System in Transition

What most consumers experience as a simple online purchase rests on top of a system that has quietly expanded into something far more complex than the interface suggests. A product appears at a compelling price, often sourced from thousands of miles away, and arrives after a delay that, until recently, felt acceptable. That surface has remained stable even as the underlying system scaled into billions of individual shipments moving across borders each year, with more than one billion entering the United States alone under de minimis thresholds. The moment feels ordinary. The machinery behind it no longer is.

By 2025, the imbalance becomes difficult to ignore. Customs systems built for containerized trade now process parcel flows at a scale they were never designed to handle, with fewer than 1 percent of shipments inspected despite failure rates exceeding 20 percent among those checked. Misclassification, undervaluation, and safety violations are not exceptions. They are recurring outcomes. At that volume, even small inconsistencies accumulate into system-level exposure, not just for regulators, but for the platforms that depend on uninterrupted flow.

Early e-commerce operated within a narrower frame. Domestic fulfillment dominated, and cross-border trade remained secondary, measured in pallets and containers rather than individual parcels. As platforms connected consumers directly to overseas manufacturers, that balance shifted. What began as a marginal efficiency became a structural advantage, particularly when duty exemptions could account for 10 to 15 percent of product value. The advantage was not designed. It emerged.

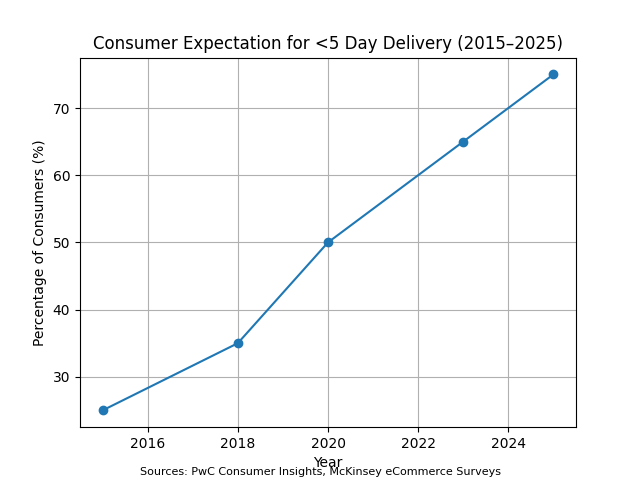

Consumers adjusted in predictable ways. More than 70 percent accepted delivery windows stretching two to three weeks in exchange for lower prices, often refreshing tracking links that offered little clarity and tolerating quality variability as part of the transaction. The system worked because expectations were calibrated to its limits.

That calibration is breaking.

As volumes moved into the billions, friction surfaced in places that had previously absorbed it. Networks designed for bulk throughput now process fragmented, data-intensive flows. Compliance requirements have tightened. Tariffs once avoided are increasingly enforced. A five-dollar product that once arrived in three weeks can now cost closer to eight when duties and handling are applied, yet arrive in two days through local inventory. The shift is not incremental. It is structural.

Bulk importation, regional staging, and domestic distribution are replacing direct-from-origin fulfillment at scale. What appears externally as faster delivery is, in practice, the result of inventory repositioning, placing goods closer to demand before purchase occurs. The interface remains familiar. The system has reorganized beneath it, quietly removing the conditions that once made ultra-low prices possible.

Evolution of E-Commerce System Structure

| Dimension | Era 1: Parcel Arbitrage | Era 2: Structured Commerce |

|---|---|---|

| Primary Flow | Direct cross-border parcels | Bulk import + local distribution |

| Cost Advantage | Duty exemptions, low oversight | Operational efficiency, scale control |

| Consumer Trade-Off | Low price vs long delivery | Reliability vs marginal price increase |

| Logistics Model | Fragmented parcel networks | Integrated regional fulfillment |

| System Visibility | Low (opaque flows) | High (data-driven, traceable) |

Source: IoIE Analysis; OECD; European Commission

What Is Happening

Rather than a sudden disruption, what is unfolding is a rebalancing of cost, control, and responsibility across a system that now exceeds one trillion dollars in global cross-border e-commerce. Functions that were once distributed across sellers, logistics providers, and governments are being consolidated, increasingly within platforms themselves, where coordination can be enforced with fewer points of failure.

Costs are no longer externalized.

At the level of a single transaction, the change appears small. A few dollars added for duties, compliance, or handling. Multiplied across millions of orders, it becomes decisive. In categories like apparel, where margins often sit between 20 and 40 percent and return rates exceed 25 percent, even a modest increase in cost can eliminate profitability. The system begins to impose discipline not through policy alone, but through arithmetic.

Precision replaces speed as the governing constraint. Classification, origin tracking, and valuation must now be accurate at the level of each unit, across millions of transactions where misclassification rates can exceed 10 percent. A one percent error rate, which might once have been absorbed, now translates into tens of thousands of disrupted orders. At that scale, approximation is no longer a viable strategy.

Infrastructure

| Function | Earlier Model | Current Model |

|---|---|---|

| Role | Marketplace intermediary | Integrated retail operator |

| Inventory Control | Seller-managed | Platform-influenced or controlled |

| Logistics | Third-party dependent | Owned / orchestrated networks |

| Compliance | External / fragmented | Embedded into transaction flow |

| Revenue Capture | Fees and commissions | End-to-end value chain capture |

Source: IoIE Analysis; McKinsey; Company Filings

In response, a new layer of infrastructure is forming, absorbing billions in investment. Compliance automation, tax calculation systems, and supply chain visibility platforms are no longer peripheral tools. They are embedded conditions of participation. The transaction becomes a coordinated event across data systems before a product moves physically, reversing the sequence that once defined e-commerce.

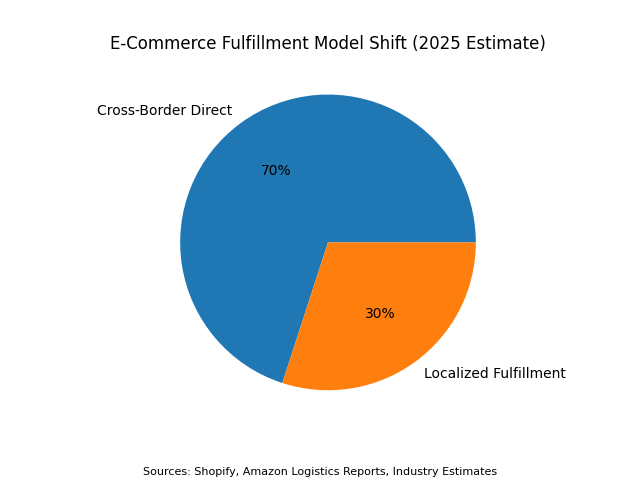

Physical networks evolve in parallel. Direct cross-border shipping persists, but it is increasingly supplemented by hybrid models where bulk imports feed regional warehouses, enabling delivery windows that reach over 70 percent of U.S. consumers within one to two days. Speed is no longer a function of transit. It is a function of placement.

Business models diverge along this line. Platforms built on direct cross-border fulfillment encounter rising friction as compliance costs increase, while those with localized infrastructure operate with greater stability. Control becomes less about ownership and more about orchestration. That distinction determines who can scale without breaking.

Impact Across Industry and Consumers

Across the system, pressure redistributes unevenly, shaping behavior in ways that are visible at the margins before they become obvious at scale.

Platforms reflect the shift first. What began as asset-light marketplaces now resemble integrated retail systems, combining digital interfaces with physical infrastructure that spans hundreds of fulfillment centers and increasingly dense last-mile networks. In some cases, more than 60 percent of volume is fulfilled internally, reducing reliance on external coordination. The platform becomes the system.

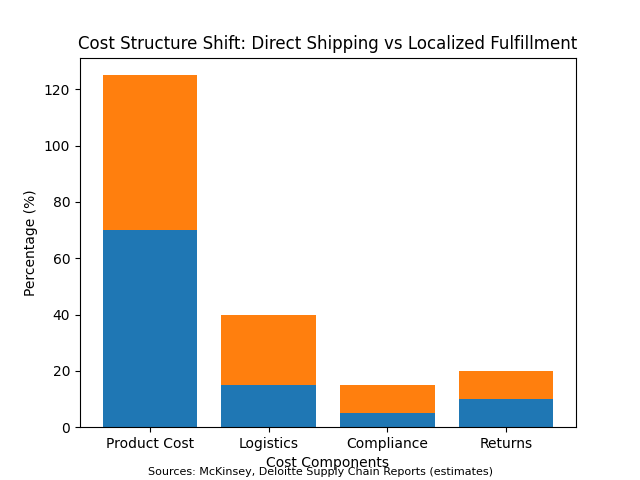

For sellers, particularly those built on cross-border arbitrage, the transition introduces constraints that compound quickly. A merchant once dependent on direct-from-origin shipping now faces rising duties, stricter compliance, and delivery expectations that compress timelines from weeks to days. Meeting those expectations often requires staging inventory locally, where logistics alone can account for 15 to 25 percent of product cost. What was once optional becomes necessary.

Margins compress with little room for recovery. A seller operating at 20 percent gross margin may find that incremental increases in compliance or fulfillment cost erase profitability across entire product lines. The flexibility that once enabled rapid scaling becomes a liability when precision is required. Independence narrows.

Seller Economics: Then vs Now

| Factor | Parcel Model | Structured Model |

|---|---|---|

| Margin Structure | Driven by price arbitrage | Driven by operational efficiency |

| Inventory Strategy | Ship-on-demand | Pre-positioned inventory |

| Risk Exposure | Low compliance exposure | High compliance accountability |

| Operational Complexity | Low | High (multi-layer coordination) |

| Scalability | High via volume | High via integration |

Source: IoIE Analysis; Deloitte; Shopify Reports

Consumers encounter the shift differently. Price remains important, but it now competes directly with delivery speed, reliability, and ease of return. Reducing delivery time from a week to two days can increase conversion rates by 20 to 40 percent, suggesting that certainty carries measurable value. The decision shifts from what something costs to what it guarantees.

This introduces a more subtle change. Consumers are no longer evaluating products alone. They are evaluating outcomes, including the likelihood that an order arrives as expected and can be resolved easily if it does not. Delays and inconsistencies, once tolerated, now function as friction that is priced into behavior.

Beneath that experience, complexity increases. Each transaction requires coordination across multiple layers, including data validation, duty calculation, compliance checks, and logistics optimization, before movement occurs. The interface remains simple. The system behind it becomes less forgiving with each additional requirement.

Demand does not contract under these conditions. It reorganizes toward consistency. Consumers gravitate toward platforms that deliver predictable outcomes, even at slightly higher prices, narrowing the space in which variability can exist without penalty.

Consumer Behavior Shift

| Behavioral Dimension | Earlier Pattern | Current Pattern |

|---|---|---|

| Primary Driver | Lowest price | Reliability + speed + price |

| Delivery Expectation | 2–3 weeks acceptable | 2–5 days expected |

| Tolerance for Variability | High | Low |

| Trust Model | Implicit (price-driven) | Explicit (platform-driven) |

| Decision Framework | Cost vs time | Outcome certainty vs friction |

Source: IoIE Analysis; PwC Consumer Insights; McKinsey

Regional Fragmentation and Divergence

The transition to a more structured e-commerce system is not uniform. While the underlying shift toward control, compliance, and localized fulfillment is global, its expression varies significantly across regions based on regulatory maturity, economic structure, and digital infrastructure.

United States

The U.S. is moving toward tighter enforcement of trade policy and de minimis restrictions, with over 1 billion de minimis shipments entering annually. Policy focus is increasingly centered on tariffs and domestic competitiveness, pushing platforms toward localized fulfillment and hybrid models.

Europe

Europe is at the forefront of formal integration, processing approximately 5.8 billion low-value imports annually. Comprehensive customs reform and platform accountability frameworks are accelerating the transition toward structured, regionally controlled systems focused on compliance and tax capture.

China

China continues to operate as the primary production and export engine of global e-commerce, accounting for a dominant share of cross-border parcel flows. At the same time, it is strengthening domestic consumption and logistics capabilities to adapt to tightening external regulations.

Asia (Ex-China)

Markets across Southeast Asia and broader Asia are experiencing rapid e-commerce growth, with regional GMV expected to exceed $300 billion in the near term. Regulatory environments remain mixed, with some markets tightening controls while others prioritize digital inclusion and expansion.

Middle East

The Middle East is investing heavily in logistics infrastructure, with countries such as the UAE and Saudi Arabia positioning themselves as regional fulfillment hubs. E-commerce growth rates exceeding 15–20% annually are driving parallel regulatory development.

Africa

E-commerce in Africa remains in an earlier stage, with penetration rates below 10% in many markets. Growth is driven by mobile adoption and digital access, while regulatory and logistics systems develop more gradually.

Latin America

Latin America is balancing rapid adoption—growing at over 20% annually in key markets like Brazil and Mexico—with economic volatility. Cross-border commerce remains important, though localization is increasing as systems mature.

Low-Income Markets

In low-income markets, e-commerce expansion is closely tied to digital access and affordability. Regulatory enforcement remains limited, and cross-border models continue to play a significant role, often accounting for a disproportionate share of available goods.

Middle-Income Markets

Middle-income markets are at the center of the transition, where growth and regulation intersect. These economies are increasingly formalizing e-commerce through tax policy and compliance requirements while maintaining openness to cross-border trade.

High-Income Markets

High-income markets are leading the shift toward structured e-commerce systems, supported by advanced logistics and regulatory frameworks. These markets set the standards for compliance, consumer protection, and fulfillment expectations.

Across regions, the direction is consistent but the pace varies. E-commerce is fragmenting into a set of regionally governed systems, each reflecting local economic priorities, regulatory capacity, and consumer behavior.

Governance, Regulation, and Economic Realignment

What appears externally as tightening regulation is better understood as a system correcting for its own scale, where volume has made previous gaps visible. Billions of shipments, many historically bypassing duties, now move through systems that must reconcile flow with accountability, particularly as global counterfeit trade linked to e-commerce exceeds 450 billion dollars annually.

At this scale, alignment becomes structural.

Supply chains begin to reorganize around visibility instead of velocity. Rather than reacting to each transaction with fragmented parcel flows, goods are increasingly imported in bulk, classified in advance, and staged within regional systems before sale. Movement becomes planned. Data becomes prerequisite. Uncertainty becomes cost.

The redistribution of value follows with similar clarity. Activities that once occurred across diffuse global pathways, including sorting, handling, delivery, and returns, are increasingly localized within domestic economies. In the United States, fulfillment and delivery expansion has generated hundreds of thousands of logistics roles over the past decade. Digital demand resolves into physical work.

System-Level Transformation

| System Layer | Before | After |

|---|---|---|

| Trade Integration | Partially detached | Fully integrated |

| Data Role | Secondary / incomplete | Primary driver of movement |

| Logistics Structure | Decentralized parcels | Coordinated regional networks |

| Regulatory Interface | Border enforcement | Embedded compliance systems |

| Economic Model | Arbitrage-driven | Infrastructure-driven |

Source: IoIE Analysis; OECD; World Bank; EU Commission

Measurement improves as bypassing becomes more difficult.

Platforms occupy a central position within this transition. Compliance is no longer enforced solely at the border, where inspection rates remain below 1 percent, but embedded directly into the transaction itself. Product data, including origin, classification, and valuation, must be validated before movement occurs. The constraint shifts from physical inspection to informational completeness.

Goods and data move together or not at all.

At the same time, geopolitical dynamics exert greater influence. Trade tensions, tariffs, and enforcement mechanisms increasingly shape how e-commerce operates across borders, particularly between major economies. Platforms must navigate systems defined not only by efficiency, but by policy constraints that shift over time.

They operate within national frameworks while remaining globally distributed.

Efficiency remains necessary, but it is bounded by compliance. Pricing begins to reflect the full cost of movement, including duties and data requirements, while domestic industries encounter more balanced competitive conditions. Smaller sellers, lacking scale or infrastructure, face higher barriers to entry. Participation becomes conditional.

System-Level Transformation

| System Layer | Before | After |

|---|---|---|

| Trade Integration | Partially detached | Fully integrated |

| Data Role | Secondary / incomplete | Primary driver of movement |

| Logistics Structure | Decentralized parcels | Coordinated regional networks |

| Regulatory Interface | Border enforcement | Embedded compliance systems |

| Economic Model | Arbitrage-driven | Infrastructure-driven |

Source: IoIE Analysis; OECD; World Bank; EU Commission

Outlook: The Near-Term Future of E-Commerce

The next phase of e-commerce is defined less by expansion of access and more by reorganization of function, where growth continues but shifts toward infrastructure capable of sustaining scale under constraint. Investment patterns make this visible, with billions flowing into logistics orchestration, compliance systems, and supply chain technology that operates behind the consumer interface.

The movement of goods follows the same logic. High-volume, low-value products are increasingly managed through bulk importation and regional distribution rather than individual cross-border shipments, reducing reliance on long-distance parcel flows that once defined the model. Inventory is positioned closer to demand, compressing delivery windows to one or two days for a majority of consumers in mature markets.

Speed becomes proximity.

Financial systems evolve in parallel. Payments become more tightly integrated with tax and compliance frameworks, increasing complexity for legacy models while accelerating the adoption of systems that embed payments directly within commerce and logistics flows. In parts of Asia, unified ecosystems already process billions of transactions annually within integrated platforms, collapsing multiple steps into a single interaction.

Retail changes shape as a result. Physical stores do not disappear. They are repurposed into nodes within distribution networks, supporting fulfillment, returns, and inventory management, with a growing share of online orders fulfilled through store-based systems. The store becomes part of the network rather than separate from it.

The structure that emerges resists simple categorization. Platforms coordinate standards and execution, supply chains remain globally distributed, and regulation defines operational boundaries without eliminating flexibility entirely.

Stability begins to take form here. What once appeared as millions of independent transactions becomes a coordinated system in which goods, data, and payments move together through integrated infrastructure. Variability gives way to predictability.

The transition is not complete. Data standards remain inconsistent across jurisdictions, logistics networks continue to adjust, and regulatory frameworks evolve unevenly. Friction persists, but it reflects alignment in progress rather than failure.

E-commerce is not slowing.

It is becoming embedded.

Key Takeaways

- E-commerce is transitioning from a parcel arbitrage economy to structured commerce

- Cost advantages from duty exemptions are being removed, reshaping pricing and margins

- Platforms are evolving into infrastructure-driven, stateless retailers

- Consumers are shifting from price-driven to reliability-driven behavior

- Supply chains are moving toward localized, just-in-place inventory systems

- The system is fragmenting into regionally governed markets

- E-commerce is becoming an integrated component of global trade infrastructure

Sources

- European Commission; E-commerce VAT and Customs Reform (Low-Value Consignments Data); – Link

- United States Customs and Border Protection (CBP); Section 321 / De Minimis Shipments Overview;– Link

- OECD; Trade in Counterfeit and Pirated Goods: Mapping the Economic Impact;– Link

- UNCTAD; Global E-Commerce and Development Report;– Link

- Pitney Bowes; Parcel Shipping Index (Global Parcel Volume Trends);– Link

- McKinsey & Company; Global Logistics and Supply Chain Transformation Insights;– Link

- PwC; Global Consumer Insights Survey (Delivery Expectations & Behavior);– Link

- Deloitte; Global Supply Chain and Operations Trends;– Link

- Shopify; Future of Commerce Report (Global E-Commerce Trends);– Link

- Amazon; Annual Report / Fulfillment & Logistics Infrastructure;– Link

- Walmart; Annual Report (Omnichannel & Store Fulfillment Transformation);– Link

- World Bank; Trade and Global Value Chains Data & Reports;– Link