{kind=link}

The Internet as the Place We Live

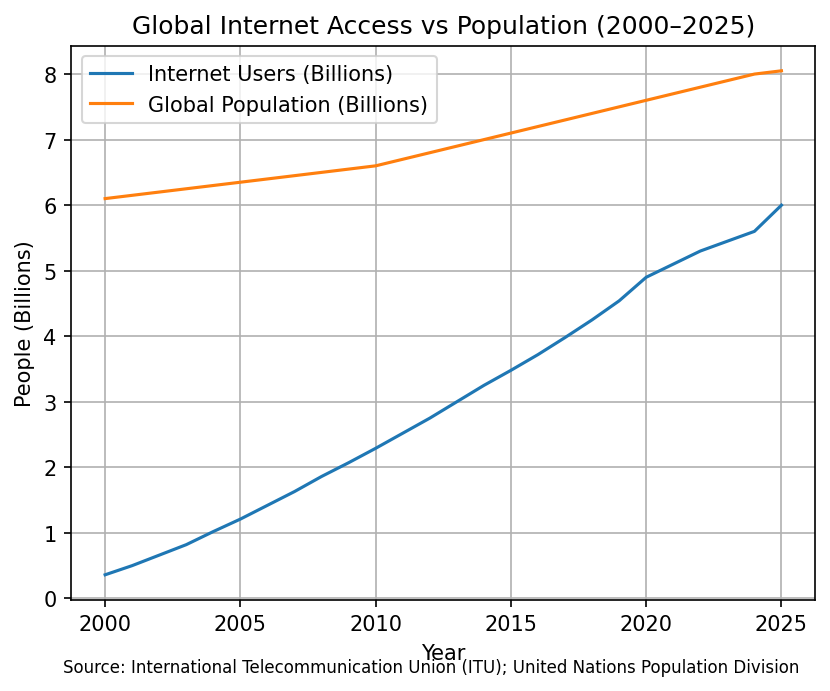

The internet is no longer something most people “go on.” It is where modern life happens, quietly, constantly, and by default. More than six billion people are online today, representing roughly three-quarters of humanity, while approximately 2.2 billion people remain offline. Even among those who are connected, the dividing line is no longer access alone. It is speed, affordability, reliability, and skills. The quality of connection increasingly determines whether the internet meaningfully expands daily life or merely hovers at its edges.

That distinction matters because the internet is no longer just a communications layer. It now functions as infrastructure. It underpins finance, logistics, healthcare coordination, education delivery, commerce, news, and public services. For a growing share of the global population, participation in economic and civic life assumes digital access by default. The internet has become an economic system humans now live inside, rather than a tool they occasionally use.

In high-income contexts, connected living is increasingly ambient. Homes regulate temperature and security automatically. Cars route around traffic in real time and anticipate maintenance. Wearables monitor sleep, movement, and heart rhythms. Work flows through always-on platforms, shared documents, and real-time dashboards where decisions move faster than meetings. The most noticeable change is not the technology itself, but the tempo of life. Expectations rise. Responsiveness becomes normative. Convenience shifts from benefit to baseline.

In much of the middle-income world, the experience looks different. Here, the internet functions as a master key. Super-apps and mobile platforms integrate payments, transport, banking, shopping, and communication into single interfaces. A market vendor accepts QR payments. A parent schedules a clinic visit by phone. A small business reaches customers beyond its immediate geography. Connectivity does not merely add convenience. It rewires participation. At the same time, integration creates dependency. When platforms suspend accounts, change rules, or alter pricing, daily life can stall immediately.

In lower-income contexts, the internet is often not an add-on at all. It is a substitute for missing infrastructure. Connectivity can affect survival as much as efficiency. The scale of financial inclusion illustrates this shift. Global account ownership rose from just over half of adults in 2011 to more than three-quarters by 2021, driven largely by digital finance and mobile money. Long-run research in Kenya found that mobile money lifted roughly two percent of all households out of extreme poverty, with particularly strong effects for women entering business activity and achieving more resilient income patterns.

Global Connectivity Status by Income Group

| Income Group | Internet Penetration | Connection Quality | Affordability | Digital Skills Gap |

|---|---|---|---|---|

| High-income | >90% | High | Moderate | Low |

| Middle-income | 60–85% | Uneven | Moderate–High | Moderate |

| Low-income | <40% | Low | High | High |

| Sources: ITU; World Bank; OECD | ||||

Connectivity also reshapes the surrounding environment, not just individual households. Information flows support disease detection and care coordination. Digital monitoring improves sanitation, logistics, and service delivery. Agricultural forecasting and market data raise yields and reduce waste. Central government databases, when implemented effectively, improve recordkeeping, reduce administrative loss, and expand access to public services. Yet these benefits remain uneven. By the mid-2020s, advanced mobile networks reached a majority of the global population, but coverage and performance still varied sharply by income and geography. Quality, not access alone, increasingly defines who truly benefits from being connected.

This leads to the central premise: The internet now connects nearly every business and a majority of humanity. In doing so, it reshapes daily life: how people work, spend, learn, heal, and relate. Humans do not simply use the internet anymore. They adapt to it. That adaptation, across regions and income levels, increasingly shapes opportunity, social structure, and environmental outcomes.

What Connectivity Has Made Possible

The most visible success of the internet is expanded access. Information that once belonged to institutions now reaches individuals directly. Markets that once required physical presence, capital, or intermediaries are accessible through a phone. Services that once depended on proximity, including banking, education, healthcare, and government, now travel digitally, lowering barriers to participation across much of the world.

Economically, connectivity reshapes opportunity. Small businesses reach customers beyond local geography. Freelancers sell skills globally. Digital marketplaces allow informal enterprises to participate in formal value chains. For households, remittances move faster and at lower cost, reducing vulnerability to shocks. These effects are especially pronounced in regions where physical infrastructure lagged demand.

Financial inclusion represents one of the clearest gains. Digital payments and mobile money expand access where traditional banking was limited or absent. By the early 2020s, more than three-quarters of adults globally held an account, up sharply from a decade earlier. In many countries, mobile money penetration now exceeds bank branch coverage, enabling saving, borrowing, and payment at scale.

Global Financial Account Ownership (2011–2021)

| Year | Adults with an Account (%) |

|---|---|

| 2011 | 51% |

| 2014 | 62% |

| 2017 | 69% |

| 2021 | 76% |

| Sources: World Bank Global Findex Database | |

Productivity has also changed form. Remote work, cloud computing, and collaborative software allow firms to operate across time zones and talent pools. Automation handles routine tasks in logistics, finance, and administration, increasing output per worker. In business services and knowledge work, digital tools reduce coordination costs and enable faster decision-making.

Healthcare delivery illustrates both reach and impact. Telemedicine extends care to rural and underserved populations. Remote monitoring enables earlier intervention for chronic conditions. Digital health systems improve appointment scheduling, recordkeeping, and supply coordination. During health emergencies, digital platforms support surveillance, communication, and response at scale.

Telemedicine and Digital Health Usage Growth

| Year | Population Using Telemedicine (%) |

|---|---|

| 2015 | 10% |

| 2017 | 18% |

| 2019 | 25% |

| 2021 | 38% |

| 2023 | 45% |

| Sources: World Health Organization; OECD Health at a Glance | |

Education and skills development have similarly expanded. Online platforms distribute training at scale, from basic literacy to advanced technical skills. Connectivity supports lifelong learning, reskilling, and access to educational resources that were previously constrained by location or cost. While quality varies, reach has increased dramatically.

Connectivity also improves coordination in physical systems. In agriculture, digital forecasting and market data help farmers improve yields and reduce waste. In logistics, routing optimization cuts fuel use and delivery times. In energy and water management, digital monitoring improves efficiency and reliability. These gains translate into measurable resource savings when implemented effectively.

At the institutional level, digital public infrastructure strengthens state capacity. Centralized databases improve recordkeeping. Digital identity systems expand access to services. Online portals reduce administrative friction and corruption risk when governance aligns with design. These systems matter most where legacy bureaucracy struggled to scale.

Global Connectivity Status by Income Group

| Income Group | Internet Penetration | Connection Quality | Affordability | Digital Skills Gap |

|---|---|---|---|---|

| High-income | >90% | High | Moderate | Low |

| Middle-income | 60–85% | Uneven | Moderate–High | Moderate |

| Low-income | <40% | Low | High | High |

| Sources: ITU; World Bank; OECD | ||||

Taken together, these strengths explain why connectivity has become foundational. The internet expands access, lowers barriers, improves coordination, and raises productive capacity across sectors. While benefits vary by region and income level, the overall effect is clear. Connectivity has expanded what is possible for individuals, firms, and governments alike.

The Pressures Embedded in Connected Living

The same systems that expand access and efficiency also introduce pressures that accumulate gradually and unevenly. These pressures rarely arrive as sudden shocks. Instead, they embed themselves into daily routines, expectations, and defaults, reshaping how people allocate attention, absorb risk, and experience stability over time. Connectivity increases capacity, but it also changes what individuals and institutions are expected to manage on their own.

Key Pressure Points of Connected Living

| Pressure Type | Description | Typical Impact |

|---|---|---|

| Cognitive | Always-on demands | Burnout, fatigue |

| Financial | Frictionless spending | Debt stress |

| Labor | Platform volatility | Income instability |

| Informational | Misinformation | Poor decision-making |

| Environmental | Energy and e-waste | Local ecological harm |

| Sources: OECD; ILO; WHO; IEA | ||

In high-income contexts, the most visible pressure is cognitive saturation. Always-on connectivity normalizes constant availability and rapid response. Workers now spend much of their day interacting with digital systems across multiple platforms. Research links persistent interruption to decision fatigue, reduced focus, and rising burnout, even when measured output remains high. Productivity does not collapse, but recovery time erodes, turning efficiency into a source of strain.

Economic risk has also shifted downward. Platform-mediated work expands access to income opportunities, but it frequently transfers volatility from firms to individuals. Hundreds of millions of people now rely on digital platforms for part or all of their income, yet only a minority have access to formal social protections such as unemployment insurance, paid leave, or employer-provided benefits. Algorithmic management increasingly replaces human discretion, often without transparency, explanation, or meaningful avenues for appeal.

Financial systems reveal another form of friction. Digital payments, subscriptions, and embedded credit reduce barriers at the moment of spending, but can increase pressure later. Auto-renewals, one-click purchasing, and buy-now-pay-later models lower salience and delay consequence. Households now manage multiple subscriptions and recurring payments, many of which are forgotten or underused, contributing to rising debt stress and financial fatigue over time.

In middle-income contexts, pressures are more structural than cognitive. Connectivity often integrates daily life through platforms that combine payments, transport, commerce, and communication. While this integration improves efficiency and access, it also concentrates dependency. When accounts are suspended, rules change, or algorithms shift, income and service access can be disrupted immediately. Platform workers in these economies experience significantly higher income volatility than comparable offline workers.

In lower-income contexts, connectivity frequently substitutes for missing infrastructure rather than supplementing it. Mobile money replaces bank branches. Digital identity systems gate access to services. Health, education, and welfare coordination increasingly move online. These substitutions deliver large gains, but with limited redundancy. When digital systems fail through outages, identity mismatches, or administrative errors, access to income or essential services can disappear entirely, often without an offline alternative.

Cultural and social pressures compound these dynamics. Algorithmic systems favor scale, speed, and engagement, amplifying dominant languages and narratives while marginalizing local context. Younger populations adapt quickly, shaping identity around visibility, metrics, and continuous performance. Older populations face growing exclusion as services digitize faster than support systems expand. Many languages and local cultures remain underrepresented or absent online, narrowing whose voices are visible in digital spaces.

Information integrity presents another systemic weakness. Health, financial, and civic decisions increasingly rely on digital information flows, yet misinformation spreads through the same channels. For individuals, evaluating credibility becomes an ongoing cognitive burden rather than an occasional task, adding friction to everyday decision-making.

Environmental costs remain largely externalized. Data centers, networks, and connected devices now account for a measurable share of global electricity demand, with growth accelerating as data-intensive and AI workloads scale. At the consumption end, electronic waste continues to rise, much of it processed in regions with limited environmental safeguards. These impacts are physical, localized, and cumulative, even when they remain largely invisible to end users.

Regional Successes and Failure Modes

| Region | Primary Success | Primary Failure Mode |

|---|---|---|

| US | Convenience and speed | Burnout, volatility |

| Europe | Resilience | Slower innovation |

| China | Coordination | System-wide exposure |

| Asia | Inclusion | Thin buffers |

| Africa | Poverty reduction | Fragility |

| Middle East | Efficiency | Labor inequality |

| Latin America | Financial access | Trust risks |

| Sources: World Bank; ILO; OECD | ||

Taken together, these weaknesses reveal a consistent pattern. Connectivity expands capacity, but it also embeds pressure. Benefits diffuse broadly, while costs often concentrate locally and personally. These outcomes are not the result of misuse alone. They reflect incentive structures, scale effects, and governance frameworks that have not yet fully adapted to the realities of connected living. These pressures do not distribute evenly. They surface differently across income levels, institutions, and regions, shaping how connected living is experienced in practice.

Regions: How Connected Living Differs Across the World

The internet now reaches nearly every region on Earth, but it does not generate a uniform human experience. Instead, it interacts with income levels, institutional capacity, labor markets, and governance structures, amplifying what already exists. The same technologies—smartphones, platforms, cloud systems, and digital payments—can optimize daily life in one place, integrate fragmented systems in another, or substitute for infrastructure that never fully existed elsewhere.

Across regions, several recurring patterns of connected living have emerged. In higher-income contexts, connectivity tends to optimize mature systems, producing what feels like smart living. In many middle-income contexts, the internet integrates daily life through platforms, creating deeply connected living. In lower-income contexts, connectivity often arrives through leapfrogging, replacing missing infrastructure and reshaping survival outcomes. These are not stages along a single path, but overlapping modes of living inside the same global digital system.

Business Digital Adoption by Region

| Region | Small-Medium Businesses Using Digital Tools (%) |

|---|---|

| High-income economies | 90% |

| East Asia | 75% |

| South Asia | 65% |

| Latin America | 70% |

| Sub-Saharan Africa | 55% |

| Sources: World Bank Enterprise Surveys; OECD | |

In high-income economies, smart living optimizes systems that already function. Work, finance, healthcare, mobility, and consumption increasingly run through digital interfaces. Companies such as Amazon, Apple, Google, and Microsoft provide the invisible backbone of cloud services, identity systems, and consumer platforms that structure everyday life. Digital government portals, AI-assisted productivity tools, and subscription-based services reduce friction across tasks that once required time, paperwork, or physical presence. The success is measurable efficiency. The failure mode is cognitive overload and quiet risk transfer.

In middle-income economies, connected living integrates daily life through platforms that serve as both opportunity and infrastructure. Firms such as Grab, Gojek, Mercado Libre, and Alibaba enable millions of small businesses to reach customers, process payments, and manage logistics without building standalone systems. Income mobility and market access expand rapidly. At the same time, these platforms centralize control. When algorithms change, fees rise, or accounts are suspended, income can pause instantly. Success takes the form of inclusion. Failure appears as volatility and dependence.

In lower-income economies, connectivity most often arrives through leapfrogging. The internet substitutes for missing infrastructure rather than optimizing what already exists. Mobile money systems such as M-Pesa in Kenya and MTN Mobile Money across West Africa replace bank branches, enabling saving, payments, and remittances at national scale. Digital identity systems increasingly gate access to welfare, healthcare, and education. The gains are large and measurable, particularly in poverty reduction and service coordination. The risk is fragility. When systems fail, there is often no offline fallback.

What follows applies this income lens to specific regional realities. Each region reflects one or more of these patterns, not perfectly but clearly enough to explain why daily life under the internet feels fundamentally different from place to place.

United States: In the United States, connected life most closely resembles smart living. Internet penetration exceeds 92 percent, and daily routines are mediated through digital finance, remote work platforms, healthcare portals, subscriptions, smart homes, connected vehicles, and AI-assisted tools. Firms such as Amazon Web Services, Google Cloud, Microsoft Azure, Stripe, and Salesforce quietly underpin business operations for millions of enterprises. Roughly 35 to 40 percent of workers can work remotely at least part time, and more than 60 percent of adults manage healthcare interactions through online systems.

The tangible layer is familiar. Tap-to-pay via Apple Pay or Google Pay. Same-day delivery tracked through Amazon or Instacart. Telehealth visits conducted through Epic-linked portals or Teladoc. Small businesses operate through Square, Shopify, and Meta advertising dashboards. The success is speed and convenience at scale. The failure appears as subscription sprawl, constant notification load, and rising burnout in knowledge-intensive sectors.

Platform-mediated work illustrates the tradeoff clearly. Companies such as Uber, DoorDash, and Instacart provide income flexibility for tens of millions of Americans, yet fewer than 20 percent of gig workers receive employer-provided benefits. Income expands, but volatility increases. Efficiency rises, while responsibility shifts downward to individuals.

Europe: Europe also reflects smart living, but with stronger institutional mediation. Internet penetration exceeds 90 percent, and digital public infrastructure plays a central role. Systems such as Estonia’s X-Road, Sweden’s BankID, and the EU’s expanding digital identity framework integrate authentication, healthcare, taxation, and public services into everyday life. Connectivity here is embedded into governance, not treated solely as consumer convenience.

The success is resilience. When platforms fail or disputes arise, labor protections and consumer safeguards absorb some of the shock. Platform workers in Europe experience lower income volatility than counterparts in less regulated markets. The failure is speed. Regulatory complexity can slow innovation and cross-border digital integration, particularly for startups navigating fragmented compliance regimes.

Environmental costs are also addressed more explicitly. Europe leads global e-waste collection and recycling rates, and energy efficiency standards constrain data center expansion. These measures do not remove the footprint, but they distribute responsibility more visibly across firms, consumers, and the state.

China: China represents the most integrated form of connected living at national scale. Super-app ecosystems operated by Tencent (WeChat), Alibaba (Alipay), and Meituan combine messaging, payments, commerce, mobility, and services for more than one billion users. Mobile payments dominate urban transactions, and logistics firms such as Cainiao and JD Logistics deliver same-day service across hundreds of cities.

The success is coordination. Cities function as tightly coupled systems where time, payment, and access friction are minimized. The failure mode is concentration. When regulatory enforcement tightens or platform policies shift, millions of users and businesses can feel the impact simultaneously. High efficiency comes with system-wide exposure.

Asia (excluding China): Across Southeast and South Asia, connected living dominates through mobile-first platforms. Companies such as Grab, Gojek, Shopee, and Paytm integrate payments, transport, commerce, and credit for hundreds of millions of users. Platform ecosystems support small merchants, drivers, and delivery workers at unprecedented scale.

India’s Unified Payments Interface illustrates the success. By August 2025, UPI processed over 20 billion transactions in a single month, becoming default payment infrastructure for street vendors, clinics, schools, and households. The failure appears during outages or fraud events, when access to money itself can pause. Speed increases inclusion, but buffers remain thin.

Labor volatility remains a defining challenge. Platform workers experience income swings two to three times higher than formal peers, and logistics growth increases congestion and environmental strain. Opportunity expands faster than protection.

Africa: In Africa, connectivity arrives most clearly through leapfrogging. Mobile money platforms such as M-Pesa, Airtel Money, and MTN MoMo serve as national financial infrastructure. In several countries, digital financial access exceeds traditional banking by 30 to 40 percentage points. Long-run research links these systems to poverty reduction, particularly for women and small entrepreneurs.

The success is tangible. School fees, wages, clinic bills, and emergency remittances move through phones. In Kenya, monthly mobile money transactions exceeded 300 million in 2024. The failure is fragility. Outages, identity mismatches, or regulatory freezes can interrupt access to income or services entirely, with few offline alternatives.

E-waste and informal device processing concentrate physical risk locally, exposing communities to environmental harm generated elsewhere. Leapfrogging accelerates gains, but it also concentrates dependence.

Middle East: The Middle East contains multiple modes of connected living. High-income Gulf states exhibit smart living through state-led platforms. Saudi Arabia’s Absher and the UAE’s UAE PASS integrate identity, payments, and public services at national scale, reducing bureaucracy and transaction time.

The success is administrative efficiency. The failure appears in uneven labor outcomes. Migrant workers, who comprise up to 80 percent of the labor force in some states, rely heavily on digital remittance and platform systems while lacking labor protections. Connectivity delivers convenience for citizens and precarity for others.

Latin America: Latin America reflects connected living shaped by volatility. Digital payments, e-commerce, and platform work expanded rapidly during economic shocks. Firms such as Mercado Libre, Nubank, and Rappi provide payment rails, credit, and logistics to millions of households and small businesses.

Brazil’s Pix system demonstrates success at scale. By 2024, Pix reached nearly 170 million users and processed over BRL 11 trillion annually. Instant payments became national default infrastructure. The failure mode is trust risk. Fraud, scams, and account freezes move as fast as money itself, turning security into a daily maintenance task.

Connected Living Models by Region

| Region | Dominant Model | Defining Feature |

|---|---|---|

| United States | Smart living | Optimization of mature systems |

| Europe | Smart living | Institution-mediated connectivity |

| China | Connected living | Super-app integration |

| South & SE Asia | Connected living | Platform-based inclusion |

| Africa | Leapfrogging | Mobile-first infrastructure |

| Middle East | Mixed | State-led digital services |

| Latin America | Connected living | Platform-driven payments |

| Sources: World Bank; OECD; UNDP | ||

What the Regions Reveal:

Taken together, the regions show that the internet does not flatten inequality. It interacts with it. Smart living optimizes abundance while concentrating cognitive and behavioral strain. Connected living expands participation while amplifying volatility. Leapfrogging delivers transformative gains with limited tolerance for failure.

The same global system produces fundamentally different human realities depending on where responsibility, risk, and recovery ultimately fall, and whether governance can keep pace with platforms that now shape daily life faster than institutions respond.

The Pressures Embedded in Connected Living

The same systems that expand access and efficiency also introduce pressures that accumulate gradually and unevenly. These pressures rarely arrive as sudden shocks. Instead, they embed themselves into daily routines, expectations, and defaults, reshaping how people allocate attention, absorb risk, and experience stability over time. Connectivity increases capacity, but it also changes what individuals and institutions are expected to manage on their own.

In high-income contexts, the most visible pressure is cognitive saturation. Always-on connectivity normalizes constant availability and rapid response. Workers now spend an average of eight to ten hours per day interacting with digital systems, often across multiple platforms simultaneously. Research links persistent interruption to decision fatigue, reduced focus, and rising burnout, even when measured output remains high. Productivity does not collapse, but recovery time erodes, turning efficiency into a source of strain.

Economic risk has also shifted downward. Platform-mediated work expands access to income opportunities, but it frequently transfers volatility from firms to individuals. Hundreds of millions of people now rely on digital platforms for part or all of their income, yet fewer than one-quarter have access to formal social protections such as unemployment insurance, paid leave, or employer-provided benefits. Algorithmic management increasingly replaces human discretion, often without transparency, explanation, or meaningful avenues for appeal.

Financial systems reveal another form of friction. Digital payments, subscriptions, and embedded credit reduce barriers at the moment of spending, but can increase pressure later. Auto-renewals, one-click purchasing, and buy-now-pay-later models lower salience and delay consequence. Household surveys show consumers manage between eight and twelve subscriptions on average, many of which are forgotten or underused, contributing to rising debt stress and financial fatigue over time.

In middle-income contexts, pressures are more structural than cognitive. Connectivity often integrates daily life through platforms that combine payments, transport, commerce, and communication. While this integration improves efficiency and access, it also concentrates dependency. When accounts are suspended, rules change, or algorithms shift, income and service access can be disrupted immediately. Studies indicate that platform workers in these economies experience two to three times higher income volatility than comparable offline workers.

In lower-income contexts, connectivity frequently substitutes for missing infrastructure rather than supplementing it. Mobile money replaces bank branches. Digital identity systems gate access to services. Health, education, and welfare coordination increasingly move online. These substitutions deliver large gains, but with limited redundancy. When digital systems fail through outages, identity mismatches, or administrative errors, access to income or essential services can disappear entirely, often without an offline alternative.

Cultural and social pressures compound these dynamics. Algorithmic systems favor scale, speed, and engagement, amplifying dominant languages and narratives while marginalizing local context. Younger populations adapt quickly, shaping identity around visibility, metrics, and continuous performance. Older populations face growing exclusion as services digitize faster than support systems expand. Globally, more than 40 percent of languages remain underrepresented or absent online, narrowing whose voices are visible in digital spaces.

Information integrity presents another systemic weakness. Health, financial, and civic decisions increasingly rely on digital information flows, yet misinformation spreads through the same channels. Public health agencies link online misinformation to delayed care-seeking, reduced vaccination uptake, and heightened anxiety during crises. For individuals, evaluating credibility becomes an ongoing cognitive burden rather than an occasional task, adding friction to everyday decision-making.

Environmental costs remain largely externalized. Data centers, networks, and connected devices account for roughly 1.5 to 2 percent of global electricity demand, with growth accelerating as data-intensive and AI workloads scale. At the consumption end, the world generates more than 60 billion kilograms of electronic waste annually, most of it processed in low- and middle-income countries with limited environmental safeguards. These impacts are physical, localized, and cumulative, even when they remain largely invisible to end users.

Taken together, these weaknesses reveal a consistent pattern. Connectivity expands capacity, but it also embeds pressure. Benefits diffuse broadly, while costs often concentrate locally and personally. These outcomes are not the result of misuse alone. They reflect incentive structures, scale effects, and governance frameworks that have not yet fully adapted to the realities of connected living. These pressures do not distribute evenly; they surface differently across income levels, institutions, and regions, shaping how connected living is experienced in practice.

Where Connected Living Is Headed

The next phase of the internet will not be defined by access. For most businesses and a majority of the global population, connectivity is already assumed. What now matters is how deeply digital systems shape everyday decisions, who absorbs risk when systems fail, and whether governance evolves quickly enough to keep pace with technologies operating at real-time speed. Disconnection is no longer an inconvenience. It is a systemic shock.

In practice, the internet has shifted from a tool people log into to an environment people live inside. Artificial intelligence and automation accelerate this shift. Automated systems already screen job applicants, set dynamic prices, route deliveries, flag financial fraud, and moderate online content at scale. In large organizations, the majority of résumés are reviewed by automated systems, while AI-driven pricing engines adjust millions of prices per day across global retail platforms.

Digital Connectivity: Sector-Level Gains

| Sector | Primary Digital Gain | Illustrative Outcome |

|---|---|---|

| Finance | Financial inclusion | Mobile money, instant payments |

| Healthcare | Access expansion | Telemedicine, remote monitoring |

| Education | Scale and reach | Online learning platforms |

| Logistics | Efficiency | Route optimization, tracking |

| Government | Administrative capacity | Digital ID, e-government |

| Sources: World Bank; OECD; WHO; UNESCO | ||

For individuals, this means decisions are increasingly shaped before humans encounter them. Ride-hailing fares fluctuate minute by minute. Streaming platforms determine which creators gain visibility. Online retailers personalize product placement and pricing based on behavioral data. In finance, automated scoring models now influence most consumer credit decisions in advanced economies. The benefit is reduced friction. The cost is opacity. When systems function well, life feels smoother. When they misfire through incorrect fraud flags, account freezes, or mis-scored credit, individuals often lack clear explanations or effective paths to appeal.

Work will remain the most immediate pressure point. Remote and hybrid arrangements now account for more than one-third of jobs in advanced economies. Collaboration platforms, performance dashboards, and AI copilots increasingly shape daily output. At the same time, platform-mediated work continues to expand globally, supporting hundreds of millions of workers and sellers. Fewer than one-quarter of platform workers, however, have access to formal social protections. Flexibility expands. Volatility travels with it.

Near-Term vs Long-Term Pressures of Connected Living

| Timeframe | Dominant Pressure | System Impact |

|---|---|---|

| 18–24 months | AI automation | Labor volatility |

| 18–24 months | Platform expansion | Risk concentration |

| Post-2030 | Energy demand | Infrastructure strain |

| Post-2030 | E-waste | Environmental stress |

| Sources: IEA; OECD; UN Environment Programme | ||

Over the next decade, this duality is likely to intensify. Digital platforms will continue lowering barriers to entrepreneurship and global trade, allowing workers and small firms to reach international markets instantly. Cross-border digital services already account for a large share of global services trade growth, with small firms disproportionately represented. At the same time, livelihoods tied to opaque systems remain exposed to sudden ranking changes, enforcement actions, or rule shifts. Without updated labor standards and dispute mechanisms, connectivity risks becoming a source of permanent precarity rather than sustained mobility.

Environmental consequences will move from abstract concern to lived reality. Data centers currently consume between 1.5 and 2 percent of global electricity, with demand projected to rise sharply as AI workloads scale. In water-stressed regions, a single large data center can consume millions of liters of water per day for cooling. Meanwhile, global electronic waste is on track to exceed 75 million tonnes annually by the early 2030s, with less than one-quarter formally recycled. These are not side effects. They are structural costs of connected living.

Governance will determine whether these pressures stabilize or compound. Countries investing in digital public infrastructure—secure digital identity, interoperable payments, and data governance—show greater resilience. Where these systems are absent or weak, platform dominance fills the gap, concentrating power and risk.

Governance Levers for Stabilizing Connected Living

| Governance Tool | Primary Function | Pressure Mitigated |

|---|---|---|

| Digital public infrastructure | Service resilience | Access fragility |

| Labor protection | Income stability | Volatility |

| Data governance | Transparency | Opacity |

| Consumer protection | Trust | Financial stress |

| Environmental regulation | Cost internalization | Externalities |

| Sources: World Bank; OECD; UNDP | ||

Looking ahead, the central question is no longer whether the internet improves lives. It clearly does, and already has. The harder question is under what conditions, for which people, and at what cost. Smart living can optimize abundance. Connected living can expand participation. Leapfrogging can transform survival. Without intentional design, all three can magnify strain, volatility, and fragility.

The regional differences described throughout are not anomalies. They are expressions of the same global system operating under different institutional, economic, and governance conditions. The lesson is not that one model of connected living should be replicated, but that each requires deliberate design choices to prevent capacity from turning into pressure.

The internet has become a shared global system, but not a shared human experience. The coming decade will be defined by whether societies learn to govern connected living with the same seriousness once reserved for physical infrastructure. Roads, power grids, and water systems were never left entirely to chance. The internet should not be either.

Key Takeaways

-

The internet has shifted from a tool people use to an environment people live inside, shaping daily economic, social, and civic activity by default.

-

Access alone no longer defines digital inclusion; connection quality, affordability, reliability, and skills determine who truly benefits.

-

Connectivity has expanded opportunity by lowering barriers to markets, finance, education, healthcare, and government services across income levels.

-

The same systems that increase efficiency also embed pressure, transferring cognitive load, financial volatility, and risk from institutions to individuals.

-

Digital platforms enable inclusion and scale, but they also concentrate dependency, making livelihoods and access vulnerable to opaque rules and system failures.

-

Different regions experience connected living differently, with smart living optimizing abundance, connected living amplifying volatility, and leapfrogging transforming survival outcomes.

-

Financial inclusion through digital payments and mobile money stands out as one of the most measurable successes of connectivity, especially in lower-income contexts.

-

Environmental and physical costs, including energy use and electronic waste, are structural consequences of connected living rather than secondary side effects.

-

Governance capacity increasingly determines whether connectivity stabilizes opportunity or compounds fragility.

-

The future of connected living depends less on technology itself than on how societies choose to govern digital infrastructure with the same seriousness as physical systems.

Sources

The Internet as the Place We Live

- International Telecommunication Union; Facts and Figures 2025; – Link

- DataReportal; Digital 2025 Global Overview Report; – Link

- World Bank; World Development Report – Digital Dividends; – Link

- OECD; Digital Economy Outlook; – Link

Pew Research Center; Internet and Technology Adoption; – Link - Asian Development Bank; Platform Economy and Digital Transformation; – Link

- Food and Agriculture Organization; Digital Agriculture and Innovation; – Link

- United Nations Development Programme; Digital Strategy and Human Development; – Link

What Connectivity Has Made Possible

- World Bank; World Development Report – Digital Dividends; – Link

- OECD; Digital Economy Outlook; – Link

- International Monetary Fund; Cross-Border Payments and Digital Finance; – Link

- World Bank; Global Findex Database; – Link

- GSMA; State of the Mobile Money Industry; – Link

- McKinsey Global Institute; The Future of Work; – Link

- World Economic Forum; Digital Labour and Skills Reports; – Link

- World Health Organization; Global Digital Health Strategy; – Link

- UNESCO; Education in a Digital World; – Link

- International Energy Agency; Digitalisation and Energy Efficiency; – Link

- World Bank; Digital Public Infrastructure; – Link

The Pressures Embedded in Connected Living

- OECD; Digital Economy Outlook; – Link

- Microsoft; Work Trend Index; – Link

- American Psychological Association; Stress and Technology Research; – Link

- Nature Human Behaviour; Digital Interruption and Cognitive Load; – Link

- International Labour Organization; World Employment and Social Outlook; – Link

- Federal Reserve; Household Finance Surveys; – Link

- UNESCO; Culture and Digital Transformation; – Link

- World Health Organization; Infodemic Management Reports; – Link

- International Energy Agency; Data Centres and Data Transmission Networks; – Link

- UNITAR / ITU; Global E-waste Monitor; – Link

Regions: How Connected Living Differs Across the World

- World Bank; Digital Economy Synthesis Reports; – Link

- OECD; Digital Transformation Studies; – Link

- U.S. Census Bureau; Internet Use and Digital Access; – Link

- European Commission; Digital Economy and Society Index (DESI); – Link

- BankID (Sweden); About BankID; – Link

- OECD; Platform Economy and Labour Markets; – Link

- Tencent; WeChat Ecosystem Overview; – Link

- Alibaba Group; Alipay Digital Payments; – Link

- National Payments Corporation of India; UPI Product Statistics; – Link

- GSMA; Mobile Economy Sub-Saharan Africa; – Link

- Saudi Ministry of Interior; Absher Platform; – Link

- UAE Digital Government; UAE PASS; – Link

- Banco Central do Brasil; Pix Instant Payments; – Link

Where Connected Living Is Headed

- International Telecommunication Union; Facts and Figures 2025; – Link

- McKinsey Global Institute; Artificial Intelligence and Economic Impact; – Link

- OECD; AI Policy Observatory; – Link

- Harvard Business Review; Artificial Intelligence in Business; – Link

- MIT Sloan; Algorithmic Decision-Making; – Link

- World Trade Organization; Digital Trade Reports; – Link

- International Energy Agency; Energy and Artificial Intelligence; – Link

- United Nations Environment Programme; E-waste and Digital Sustainability; – Link

- World Bank; Digital Public Infrastructure; – Link

- United Nations Development Programme; Digital Governance and Inclusion; – Link