{kind=link}

From Challenger to Digital Financial Ecosystem

By the end of 2025, fintech is no longer defined by disruption alone. What began as a challenge to legacy banking increasingly settles into structural permanence. Years of rapid growth give way to capital repricing, regulatory tightening, and sustained operational scrutiny, reshaping the sector into a more durable configuration. Fintech now consolidates into stable roles within the financial system rather than operating at its margins. This transition reflects maturation rather than retreat, marking fintech’s shift from challenger narrative to institutional relevance.

Fintech now occupies two interdependent structural roles. One operates as stand-alone platforms serving consumers and businesses directly across payments, lending, savings, credit, insurance, and financial tools. The other functions as embedded financial infrastructure integrated into traditional banks, merchants, platforms, and non-financial enterprises. Together, these roles signal fintech’s transition from external disruptor to foundational layer of the digital economy. Investment patterns reinforce this shift, with global fintech funding declining from its 2021 peak of roughly USD 240 billion to below USD 100 billion annually by 2023–2024, indicating capital discipline rather than declining importance.

As fintech matures, three operating models increasingly shape how digital finance is organized. The first consists of stand-alone fintech platforms offering financial services directly to end users, emphasizing usability, speed, and specialization. The second involves traditional banks integrating fintech services, retaining regulated balance sheets while embedding digital capabilities to modernize operations and reduce cost. The third is the emergence of SuperApps, a limited but influential evolution in which payments anchor a broader digital ecosystem combining financial and non-financial services in a single interface. These models coexist and overlap, yet they differ materially in economics, risk allocation, and strategic control.

Fintech’s independence does not originate in technology alone, but in structural failures exposed after the 2008 financial crisis. Trust deficits, high operating costs, and constrained access created space for alternatives to emerge. Early fintech firms focused on narrow pain points such as cross-border payments, peer-to-peer lending, and digital onboarding, exploiting gaps left by risk-averse banks. Over time, cloud computing, APIs, and mobile distribution enabled horizontal expansion across payments, savings, credit, insurance, and wealth.

By the end of 2025, this expansion translates into unprecedented scale. Leading digital-first platforms collectively serve well over one billion consumer and small-business accounts worldwide. Stripe processes transaction volumes measured in the trillions of US dollars annually. Nubank exceeds 90 million customers across Latin America, while Ant Group–enabled platforms reach more than one billion users through integrated commerce and payments ecosystems. These figures confirm fintech’s evolution into a stand-alone industry with its own scale economics and network effects.

Much of fintech’s most consequential growth now occurs beneath the surface. Embedded fintech integrates directly into banks, merchants, platforms, and public infrastructure, often without end-user visibility. In advanced economies, more than 70 percent of digitally active consumers rely on third-party fintech infrastructure for account aggregation, card authorization, fraud screening, or real-time payments without recognizing it. Large merchants route the majority of online transactions through fintech processors rather than bank-native gateways, while banks increasingly depend on fintech vendors for compliance automation, identity verification, and API connectivity. This invisible integration transforms fintech from optional innovation into operational necessity.

Where stand-alone platforms intersect with embedded infrastructure, fintech begins to shape behavior rather than merely facilitate transactions. Payments evolve from isolated financial actions into embedded components of commerce, mobility, media, and everyday services. Digital payments now account for more than 60 percent of all non-cash transactions globally, with real-time and wallet-based payments expanding at double-digit annual rates across major economies. Buy-now-pay-later products capture a growing share of online checkout flows in the United States, Europe, and Australia, influencing purchasing decisions at the moment of sale. When payment integrates into buying, lending into consumption, and identity into access, fintech platforms become economic environments coordinating data, attention, and money simultaneously.

As mobile-first and real-time financial behaviors normalize globally, fintech’s societal influence increasingly drives institutional adaptation. Expectations shaped by instant payments and app-based finance spill into regulated banking, forcing traditional institutions to modernize settlement systems, interfaces, and engagement models. Fintech’s role expands beyond infrastructure into a cultural force that reshapes how financial activity fits into daily life.

This shift alters traditional banking without displacing it. Banks retain balance sheets and regulatory licenses, but steadily lose control over customer interaction points as fintech platforms intermediate daily financial activity. Revenue pressure follows through compressed payment fees, faster settlement expectations, and intensified deposit competition driven by yield transparency. Lending disruption concentrates in unsecured consumer credit, small-business finance, and point-of-sale lending, where fintech-enabled credit channels grow several times faster than traditional bank lending in many markets. In response, banks reposition themselves as regulated anchors within broader fintech ecosystems rather than end-to-end service providers.

Fintech’s maturation also exposes structural vulnerabilities. Rising interest rates and tighter liquidity conditions reveal fragile unit economics among platforms dependent on interchange subsidies or growth-driven incentives. Expanding regulation across open banking, data rights, and operational resilience raises fixed costs and slows time-to-market. Infrastructure concentration around a small number of global cloud providers introduces systemic dependencies, increasingly separating fintech firms capable of operating as resilient infrastructure from those optimized primarily for rapid scale.

Human and societal considerations increasingly define fintech’s legitimacy within the digital economy. Mobile-first platforms materially expand access to payments, savings, and credit, particularly in regions where physical banking infrastructure remains limited. More than 75 percent of adults globally now hold some form of transaction account, with digital financial services driving recent gains. At the same time, behavioral design embedded in fintech interfaces shapes spending, borrowing, and saving patterns, raising concerns around consumer protection, over-indebtedness, and algorithmic accountability. Uneven digital literacy and connectivity risk creating new forms of exclusion even as formal access expands.

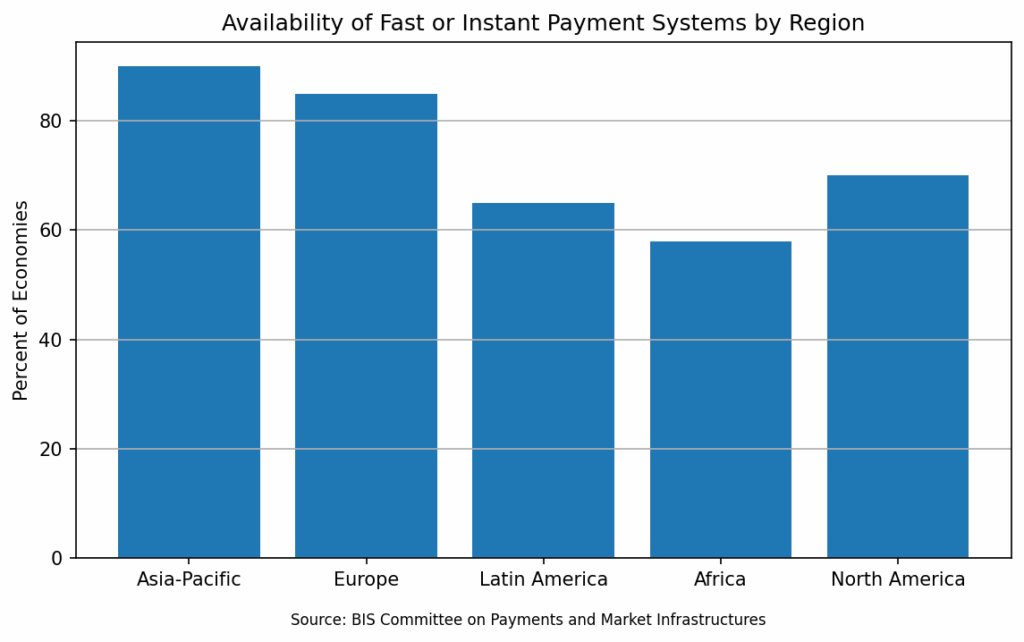

Regional expression reinforces fintech’s plural identity. North America emphasizes infrastructure fintech, embedded finance, and intensified deposit competition. Europe advances regulated integration through open finance and harmonized payment frameworks. Asia-Pacific demonstrates ecosystem dominance through SuperApps and state-backed real-time rails processing billions of transactions annually. Latin America showcases fintech-led banking alternatives responding to high spreads and low trust, while Africa positions mobile money as foundational economic infrastructure.

By the end of 2025, fintech occupies a structurally plural position. It exists as an independent platform-based industry, as embedded infrastructure within traditional banking, and, in limited markets, as SuperApp-driven digital ecosystems. Its most profound impact lies not in replacing banks, but in redefining how financial activity integrates into everyday economic life. This shift from disruption to orchestration sets the foundation for examining fintech economics at the firm level, where margins, funding costs, operating leverage, and strategic trade-offs increasingly shape executive decision-making.

Platforms, Pressure, and Executive Trade-Offs

At the firm level, fintech economics increasingly diverge from traditional banking logic. Stand-alone fintech platforms operate without deposit funding or balance-sheet intermediation, generating value through transaction volume, platform usage, and product expansion rather than net interest margins. Traditional banks, by contrast, remain anchored to regulatory capital, liquidity requirements, and funding costs. This structural distinction shapes strategy, cost discipline, and growth pathways across the sector. Within stand-alone fintech, a smaller subset of firms evolves toward SuperApp models, using payments as an anchor to layer multiple financial and non-financial services into a single user environment. These models are not representative of fintech as a whole, but they illustrate how scale and customer control reshape platform economics under specific market conditions.

Capital allocation trends reinforce this divergence. Global fintech investment totals USD 95.6 billion across 4,639 deals in 2024, marking the lowest annual level in seven years, followed by USD 44.7 billion across 2,216 deals in the first half of 2025. Capital does not exit the sector; it concentrates. Investors increasingly favor firms with proven revenue engines, regulatory clarity, and operational leverage. For fintech executives, this environment rewards disciplined growth, diversified monetization, and defensible unit economics. For sales and service teams, it reshapes buyer behavior as enterprise clients reduce vendor sprawl and demand measurable returns on integration spend.

Global Fintech Structural Indicators (Selected Points)

| Indicator | 2015 | 2021 | 2023–2024 (latest in article) | Why it matters |

|---|---|---|---|---|

| Global fintech investment (USD) | $19.1B | ≈$240B peak year (context) | $119.8B (2023); $95.6B (2024) | Signals capital repricing and shift from growth-first to discipline. |

| Global fintech deals (count) | 1,162 | — | 5,382 (2023); 4,639 (2024) | Shows consolidation and tighter funding standards. |

| Adults with a transaction account (global) | — | — | >75% (global adults) | Inclusion becomes baseline; value shifts to quality/usage of access. |

| Digital payments share of non-cash (global) | — | — | >60% of non-cash transactions | Payments become embedded in everyday platforms and commerce. |

Payments remain the primary economic backbone for most stand-alone fintech platforms and the most common entry point for broader expansion. Globally, the payments industry processes roughly 3.4 trillion transactions annually, representing approximately USD 1.8 quadrillion in value and generating a revenue pool near USD 2.4 trillion. Growth persists but moderates, with 2024 revenue expanding around 4 percent as interest income rises to nearly half of total payments revenues. For independent platforms, these dynamics underscore a central strategic reality: control over payment flows enables cross-selling into lending, subscriptions, data, and advertising, while pricing power increasingly depends on reliability and performance rather than volume alone.

At scale, payments economics reward operational excellence more than narrative positioning. Adyen’s 2024 performance provides a clear benchmark. The company processes EUR 1,285.9 billion in payment volume, reports approximately EUR 2.0 billion in net revenue, and sustains EBITDA margins in the low-to-mid-50 percent range. Growth in point-of-sale volumes reflects the convergence of physical and digital commerce under unified platforms. For executives, these figures illustrate how routing intelligence, fraud optimization, and uptime protection preserve margins more effectively than price competition.

Behavioral adoption of mobile-first and real-time transactions increasingly forces banks to operate like fintech platforms, reshaping cost structures and regulatory exposure. Consumers normalize instant peer-to-peer payments, wallet balances, and app-based transfers, while banks remain subject to prudential rules governing capital, liquidity, and settlement risk. Many fintech and digital investment platforms, by contrast, operate primarily under conduct or securities regulation, relying on internal ledgers and partner banks rather than holding customer funds directly on balance sheet. This asymmetry drives banks toward bank-backed fintech models, including proprietary P2P systems, wallet-like interfaces, and ledger-based digital balances. The motivation is not regulatory avoidance, but competitive survival as transaction behavior migrates toward fintech-style rails.

SuperApp economics extend this logic by layering multiple revenue streams onto a single user base. Revolut reports GBP 3.1 billion in revenue and GBP 1.1 billion in pretax profit for 2024, serving 52.5 million customers across payments, subscriptions, wealth, and digital assets. Nubank reports USD 1.97 billion in net income for FY 2024, nearly doubling year over year, alongside an annualized return on equity of roughly 29 percent. These results illustrate how stand-alone fintechs evolve into multi-product financial environments where customer lifetime value, funding efficiency, and cross-sell depth outweigh raw user growth.

Credit-led expansion introduces both opportunity and fragility. Buy-now-pay-later grows rapidly as a conversion tool, reaching an estimated 86.5 million users in the United States during 2024. Yet unit economics remain highly sensitive to funding costs and loss rates. Affirm reports USD 2.3 billion in fiscal 2024 revenue against USD 1.3 billion in transaction costs, leaving just under USD 1.0 billion in revenue after transaction expenses. For CFOs, these figures highlight a persistent tension: scale accelerates revenue, but sustainable profitability depends on disciplined underwriting, capital structure, and loss management.

Cost discipline increasingly separates durable platforms from weaker competitors. Fraud economics provide one of the clearest illustrations. Merchants spend an average of USD 4.60 for every dollar lost to fraud, while financial services firms spend approximately USD 4.41 per dollar once investigation, remediation, and operational overhead are included. These ratios explain why spending on identity verification, fraud prevention, and chargeback management remains resilient even as budgets tighten. For fintech platforms, operational failures translate directly into revenue leakage and customer churn, elevating reliability from a support function to a core economic driver.

Regulatory developments further shape fintech strategy. In the United Kingdom, open banking exceeds 16.5 million active users, while open-banking-enabled payments reach nearly 33 million in a single month by late 2025. In the United States, the CFPB’s personal financial data rights rule, finalized in October 2024 and effective January 2025, establishes mandatory data access and consent frameworks. For independent platforms, these rules expand addressable markets while increasing compliance costs, reinforcing the competitive advantage of scale, legal maturity, and governance readiness.

Technology investment reflects fintech’s maturation. Platforms increasingly prioritize resilience, automation, and governance over novelty. Financial Stability Board analysis highlights third-party dependencies and AI model concentration as emerging systemic risks, even as automation delivers measurable savings in fraud detection, underwriting, and customer service. Commercially, fintech offerings now bundle functionality with assurance, documentation, and uptime commitments, as enterprise buyers increasingly purchase operational confidence alongside technical capability.

For executives, fintech economics at the end of 2025 reward orchestration over disruption. Growth remains achievable, but it flows to platforms that convert transaction control into multi-product economics, manage costs with discipline, and operate comfortably under regulatory scrutiny. Sales and service teams sit at the front line of this shift, translating reliability, compliance readiness, and performance into commercial trust. As fintech becomes core financial infrastructure, economic success depends less on narrative ambition and more on execution quality and strategic focus.

How Fintech Reshapes Norms, Culture, and Human Behavior

Money increasingly disappears from view. By the end of 2025, it moves quietly, continuously, and almost invisibly through daily life. Fintech’s most enduring impact is no longer novelty or speed, but normalization. Payments, savings, and credit reside inside phones, platforms, and routines, reshaping how people experience time, trust, and economic participation. Banking fades as a destination and reappears as background infrastructure, while money becomes something people expect to move instantly, clearly, and with minimal effort.

This normalization reflects a broader social transition. Financial access approaches saturation in many regions, shifting the central challenge from formal inclusion to usable inclusion. Globally, 79 percent of adults now hold an account, up from 74 percent in 2021, while low- and middle-income economies reach 75 percent. In developing economies, 40 percent of adults save using a financial account, a marked departure from cash-dominant behavior. These figures matter not simply as milestones, but because they signal that financial interaction becomes routine, embedded in decisions about work, family, healthcare, and mobility rather than treated as a separate institutional act.

Mobile-enabled financial systems illustrate how this shift reshapes everyday life. With more than two billion registered mobile money accounts and over half a billion monthly active users, these systems process roughly USD 1.68 trillion in transaction value each year. Their importance lies less in scale than in immediacy. Wages, remittances, and payments move when they are needed, not when institutions permit them. In many developing contexts, this immediacy carries outsized human significance, allowing households to respond to illness, income gaps, or opportunity without relying on informal lenders or costly coping strategies.

As transactions become ever-present, financial decision-making integrates into daily life rather than remaining episodic. Behavioral economics explains why speed matters. Instant payments shrink the psychological distance between intention and action, making spending, saving, and sharing money feel as natural as messaging or navigation. Research shows that 58 percent of children aged eight to 17 engage in digital spending environments designed to encourage rapid decisions. Beyond gaming, these dynamics extend across food delivery, ride-hailing, subscriptions, and creator platforms, shaping financial habits early and embedding money into social interaction.

Speed also reshapes dignity and agency. Digital payments reduce time spent traveling, waiting, or negotiating access to funds. For young workers, migrants, informal earners, and low-income households, immediate settlement of income and faster remittances reduce uncertainty in daily planning. Adoption of fast payment systems accelerates when they support everyday use cases and allow non-bank participation, expanding economic engagement where people already live and work rather than forcing lives to adapt to institutional constraints.

These behavioral shifts increasingly reshape institutions themselves. As mobile-first transaction norms spread, expectations formed outside legacy banking models spill back into regulated finance. Many payment experiences feel detached from banks even when they remain bank-backed, conditioning users to expect speed without visibility into regulatory structure. Banks respond by redesigning themselves to behave more like fintech platforms, deploying app-native interfaces, internal ledger systems, and digital balances that mirror fintech usability while operating within prudential oversight. Cultural expectation, rather than technology alone, becomes a driver of institutional change.

Fintech Usage and Behavioral Adoption

| User behavior | Earlier point | Latest point |

|---|---|---|

| Adults making digital payments (LMICs) | 34% (2014) | 62% (2024) |

| Adults making digital merchant payments (global) | 35% (2021) | 42% (2024) |

| Mobile money monthly active users | 250M (2019) | 514M (2024) |

| Sources: World Bank Global Findex; GSMA State of Mobile Money | ||

Social outcomes vary across fintech’s operating models. Stand-alone fintech platforms shape behavior most directly through interface design and default settings. Bank-integrated fintech embeds change more gradually, balancing usability with protection. SuperApp-style ecosystems concentrate transactions, attention, and services within a single environment, amplifying convenience while increasing behavioral influence. Across all models, lower barriers to entry and instant transactions quietly reshape poverty dynamics by normalizing financial participation for populations long excluded from traditional banking.

Within this broader transformation, poverty reduction emerges as a cascading human outcome rather than an explicit design objective. Lower minimum balances, reduced documentation requirements, micro-savings capability, and widely accepted digital payments remove structural frictions that historically trap households in cash-based survival cycles. Evidence shows these capabilities improve resilience, reduce volatility, and allow individuals to act on information and opportunity more quickly. Poverty is not eliminated, but its daily severity softens in ways that compound over time.

Risks remain integral to this picture. Faster access can amplify impulsive spending, over-borrowing, and exposure to fraud, particularly among youth and first-time users. Research consistently shows that education alone is insufficient without design safeguards, age-appropriate interfaces, and transparent dispute mechanisms. Inclusion expands opportunity when speed is balanced with protection, but it can reproduce vulnerability when engagement incentives outpace governance.

From a UN-aligned perspective, governance functions as social infrastructure rather than restraint. Cooling-off periods, default alerts, clear consent architectures, and interoperability standards shape whether systems scale safely. Shifting success metrics from account ownership toward usable access, measured through frequency, reliability, and purpose of use, more accurately reflects fintech’s real social impact. Protection, in this framing, enables trust and longevity rather than limiting innovation.

By the end of 2025, fintech’s societal meaning is defined less by disruption and more by habit. Money flows through daily life with increasing speed and invisibility, reshaping norms around trust, autonomy, and participation. Culture remains the lens of analysis, but the human consequences run deeper. As barriers to money management fall, poverty’s grip weakens at the margins, and financial access becomes a quiet yet powerful force shaping dignity, resilience, and opportunity across societies.

How Regional Context Shapes Adoption, Impact, and Risk

Fintech’s social and economic effects are not uniform. While digital finance relies on broadly similar technologies, its outcomes diverge sharply based on regulatory structures, income levels, institutional trust, and cultural norms. By the end of 2025, regions increasingly reflect distinct fintech identities shaped less by innovation itself and more by how societies absorb speed, access, and governance into daily life.

These differences matter because they determine whether fintech reinforces existing financial systems, substitutes for missing infrastructure, or evolves into platform-driven ecosystems that blur boundaries between commerce, media, and finance. Viewed regionally, fintech reveals how money, trust, and participation reorganize themselves across very different social and economic contexts.

United States: The United States presents a paradox of fintech maturity. Despite a deeply banked population, consumer behavior increasingly centers on fintech-led payments, wallets, and investment platforms. Peer-to-peer payment systems process well over one trillion dollars annually, with platforms such as Zelle and Venmo becoming default tools for everyday transfers. Fintechs dominate growth in unsecured consumer credit and retail investing, while banks respond by deploying bank-backed real-time payment rails and wallet-like interfaces. The result is a market in which fintech reshapes daily financial behavior, while banks retain balance-sheet primacy but steadily lose control over customer interaction.

Europe: Europe approaches fintech through integration rather than confrontation. Open banking and harmonized regulation enable fintech adoption within established financial institutions rather than outside them. More than 16 million users actively engage with open-banking-enabled services, supporting account aggregation, alternative payments, and cross-border credit assessment. Digital banks achieve scale, but typically coexist with incumbents rather than replacing them. Europe’s model emphasizes competition through interoperability, prioritizing systemic stability and consumer protection over rapid platform dominance.

China: In China, fintech evolves into a deeply embedded digital ecosystem. SuperApp platforms integrate payments, commerce, savings, credit, and public services into a single daily interface. Mobile payments process transaction volumes measured in the tens of trillions of dollars annually, while cash usage declines sharply across both urban and rural areas. QR-based payments become the default for everything from transit to street vendors. Strong state oversight shapes platform behavior, allowing scale while constraining systemic risk.

Asia (excluding China): Across Asia, fintech adoption reflects sharp contrasts between advanced digital economies and emerging markets. In India, the Unified Payments Interface processes over ten billion transactions monthly, enabling instant, low-cost transfers for households and small businesses. Southeast Asia experiences rapid wallet adoption driven by e-commerce and ride-hailing platforms, where payments, mobility, and commerce converge. The region’s defining feature is state-led payment infrastructure paired with private-sector innovation, enabling rapid scaling while remaining anchored to public rails.

Africa: In Africa, fintech functions as foundational economic infrastructure rather than an enhancement to banking. Mobile money platforms reach a majority of adults in several countries, processing transaction values equivalent to more than half of national GDP in some markets. These systems enable wages, remittances, merchant payments, and government transfers in environments where bank branches remain limited. For millions, the mobile phone serves as the primary financial interface. Africa demonstrates fintech’s capacity to substitute for missing institutions and stabilize daily economic life.

Latin America: Latin America showcases fintech as a response to high fees, low trust, and limited competition in traditional banking. Digital banks attract tens of millions of users by offering low-cost accounts, instant payments, and simplified onboarding. Real-time payment systems gain rapid merchant acceptance, reshaping peer transfers and retail commerce. Fintech success reflects pent-up demand for accessible financial services rather than pure technological leapfrogging. Over time, digital-first models pressure incumbents to lower costs and modernize distribution.

Low-, Middle-, and High-Income Economies: Across income groups, fintech plays different structural roles. In high-income economies, it optimizes convenience, speed, and interface experience within already banked populations. In middle-income economies, fintech expands competition and becomes a primary channel for payments and savings. In low-income economies, it substitutes for absent banking infrastructure, enabling basic money management with minimal documentation or minimum balances. The unifying factor is how rapidly digital finance reduces friction in everyday economic participation.

Taken together, these regional patterns demonstrate that fintech’s effects are shaped less by technology itself than by the social, regulatory, and economic environments into which it is introduced. Fintech does not follow a single global trajectory. Its impact reflects regional choices around regulation, infrastructure, and institutional trust.

Before mobile-enabled finance, poverty is shaped primarily by physical distance, documentation barriers, and the inability to safely store or move money. After mobile finance becomes ubiquitous, the constraint shifts toward income stability, digital literacy, and governance of speed rather than access itself. This distinction underscores fintech’s deeper role as social infrastructure rather than financial novelty.

Understanding these regional differences is essential for policymakers, financial institutions, and platform operators alike. Fintech’s future influence will depend less on innovation cycles and more on how societies choose to balance speed, access, and protection as digital finance becomes an everyday human utility.

Power, Rights, and Control in a Post-Disruption Fintech System

As fintech approaches maturity, governance replaces disruption as the decisive force shaping its trajectory. By the end of 2025, the central question is no longer whether fintech belongs in the financial system, but how authority, responsibility, and rights are allocated across increasingly complex digital arrangements. Regulation now responds to behaviors already normalized at scale. Real-time payments, digital wallets, platform-based finance, and embedded financial services are no longer experimental. They function as daily infrastructure for households, businesses, and governments, requiring governance frameworks to evolve from permissive experimentation toward durable oversight.

This transition reveals a deeper reality. Fintech governance is no longer defined by product categories, but by power – power over data, transaction flows, and the rules governing participation. These pressures manifest differently across fintech’s three dominant paths, each producing distinct strengths, vulnerabilities, and regulatory challenges. Understanding governance today requires examining how control operates within each model rather than seeking a single, uniform regulatory response.

Stand-Alone Fintech Platforms: Stand-alone fintech platforms represent the most familiar governance challenge. These firms deliver discrete financial services directly to users, often moving faster than institutional frameworks designed for traditional intermediaries. Their appeal rests on speed, clarity, and the ability to meet consumer demand without the structural overhead of banks. Platforms such as Robinhood lower barriers to retail investing, while payment and infrastructure providers accelerate digital commerce by abstracting complexity away from users.

Governance in this path centers on conduct and consumer protection rather than systemic stability. Data portability enables competition, but also introduces consent fatigue and uneven understanding of how personal financial data is used. Cross-border exposure emerges quickly as platforms scale beyond national licensing regimes, raising questions around disclosures, dispute resolution, and enforcement. Failures typically arise not from insolvency, but from mis-selling, opaque incentives, or accountability gaps when systems fail.

Effective governance strengthens this model rather than constraining it. Clear conduct rules, standardized disclosures, and operational resilience requirements reduce ambiguity and build trust. For many stand-alone fintechs, regulatory compliance becomes a competitive advantage, signaling reliability in markets where trust remains uneven. The regulatory challenge lies in preserving speed and accessibility while preventing erosion of consumer rights as platforms scale.

SuperApp: SuperApps present a fundamentally different governance challenge. In these systems, financial services are not discrete products but embedded functions within broader digital ecosystems. Payments, credit, identity, commerce, and communication converge within a single interface, transforming platforms into economic environments rather than service providers. Money movement becomes inseparable from daily digital life.

Governance tensions intensify because data sovereignty and jurisdiction blur. When financial identity, transaction history, and behavioral data concentrate inside a single platform, questions of ownership and control become geopolitical as well as regulatory. Cross-border transactions flow through private rails that do not align cleanly with correspondent banking systems, complicating sanctions enforcement, AML oversight, and consumer recourse. User relationships are governed as much by platform terms of service as by national law.

Fintech Operating Models and Control Points

| Model | Primary interface owner | Primary economic driver | Risk concentration | Example references |

|---|---|---|---|---|

| Stand-alone fintech platform | Fintech | Payments + cross-sell (subscriptions, lending, data) | Conduct risk; reliability/fraud | Stripe; Nubank; Ant Group-enabled platforms |

| Bank-integrated fintech | Bank or bank-fronted channel | Cost efficiency + retention; modernized rails | Third-party risk; outsourcing/cloud | Zelle-type networks; bank-led digital channels |

| SuperApp ecosystem | Platform (non-bank) | Multi-product monetization + ecosystem lock-in | Concentration of data + market power | Large SuperApps in parts of Asia-Pacific |

This concentration gives rise to what can be described as virtual nations. Users participate in platform-based economies where access, identity, and value exchange are defined by platform rules rather than citizenship. These arrangements offer real advantages, including frictionless participation and rapid inclusion. Yet they also expose systemic risks. Power concentration, opaque rule-making, and limited exit options raise concerns around accountability and consumer protection when financial life becomes deeply embedded within a single ecosystem.

Governance responses vary widely. Some jurisdictions impose functional separation, data localization, or activity-based licensing. Others rely more heavily on behavioral oversight and competition policy. The result is regulatory divergence rather than convergence, reinforcing the reality that SuperApps remain viable primarily where regulatory tolerance aligns with platform concentration.

Traditional Banking Integration: Traditional banks occupy a distinct governance position. Unlike fintech platforms, banks operate under prudential regulation designed to protect systemic stability, requiring capital buffers, liquidity management, and supervisory oversight. Yet consumer expectations shaped by fintech force banks to deliver similar speed and convenience. This tension drives banks to adopt fintech-like operating models while remaining within regulatory boundaries.

Governance in this context functions as both constraint and anchor. Banks increasingly serve as regulated foundations for identity, custody, and settlement, even as interfaces migrate toward digital platforms. Open finance rules compel data sharing, redistributing control over customer relationships. Bank-backed systems such as Zelle condition users to expect instant transfers, illustrating how banks adopt fintech behaviors to remain relevant.

Failures in this model often stem from complexity rather than intent. Outsourcing, cloud concentration, and partnerships with fintech vendors introduce third-party risk and blur accountability when incidents occur. At the same time, banks retain advantages in dispute resolution, consumer protection, and cross-border resilience. Governance frameworks increasingly position banks as stabilizing infrastructure within broader fintech ecosystems rather than obsolete intermediaries.

The Near Horizon: Fintech Under Governance Pressure

Fintech enters the near term as infrastructure rather than experiment. This shift is already measurable. Real-time payment systems now process tens of billions of transactions annually, with year-over-year growth still in the double digits across major economies. Digital wallets account for more than half of non-cash transactions globally, and in several markets they have become the default method for everyday payments. The industry is no longer expanding by invention, but by absorption into daily economic behavior.

Growth in this period comes from usage depth, not category expansion. Transaction volumes continue to rise even as new-user growth slows, a classic maturity signal. In payments, margins compress as scale increases, pushing firms to focus on reliability, uptime, and fraud control rather than acquisition. Outages and delays now carry reputational and regulatory consequences, reflecting fintech’s transition from optional service to critical utility.

Governance pressure accelerates this stabilization. Over the next phase, regulators shift from defining fintech to supervising function. Data governance, operational resilience, and third-party risk dominate supervisory agendas. In parallel, compliance costs rise. Industry estimates show that regulatory and risk-management spending now consumes a materially larger share of fintech operating budgets than it did five years ago, narrowing the cost gap with traditional banks.

The three paths respond differently, but all feel the same constraints.

Stand-alone fintech platforms focus on unit economics and compliance readiness. Venture capital patterns confirm this shift. Global fintech funding remains less than half of its 2021 peak, yet capital continues flowing to payments infrastructure, fraud prevention, and regulatory technology. Startups are increasingly built to be acquired or integrated rather than to replace incumbents.

SuperApps deepen rather than expand. In regions where they operate, a small number of platforms process the majority of retail digital payments, embedding finance into commerce, mobility, and services. However, cross-border replication slows. Data-localization rules, competition scrutiny, and consumer-protection requirements limit global scaling, reinforcing regional dominance rather than global reach.

Banks accelerate integration. In the United States alone, bank-backed instant payment systems handle hundreds of millions of transactions each month, conditioning consumers to expect immediacy even from regulated institutions. Banks invest heavily in real-time settlement, digital identity, and internal ledger modernization, while maintaining capital and liquidity buffers that fintechs do not carry. Their strategic role shifts toward trust, custody, and recourse.

Technology investment reflects these realities. Artificial intelligence spending concentrates on fraud detection, AML monitoring, and customer service automation, where cost savings and compliance benefits are immediate. At the same time, regulators highlight cloud concentration and third-party dependencies as systemic risks, pushing firms to diversify infrastructure and strengthen resilience. Scale without governance readiness is no longer viable.

Consumer behavior reinforces the trend. Users expect instant access, transparent balances, and continuous availability, but tolerance for failure declines sharply. Trust becomes a competitive differentiator. Platforms that balance speed with protection gain share; those optimized solely for growth experience higher churn and regulatory friction.

The near horizon is therefore not a new disruption cycle. It is a stress test. The firms that succeed are those that execute reliably under governance constraints. Fintech is close to maturity, but not fully settled. What happens next is not about invention, but about whether implementation holds.

Long-Term Outlook: Where Fintech Is Settling

Sending money increasingly feels less like a financial act and more like a message. Rent clears instantly. Wages arrive the same day. Funds cross borders in minutes rather than days. These behaviors are no longer exceptional. They are becoming routine, and they reveal fintech’s long-term trajectory more clearly than any forecast. Digital payments already represent more than half of all non-cash transactions globally, while real-time payment systems process tens of billions of transfers each year, more than double their early-2020s volume. Fintech’s future begins from this lived reality rather than from speculation.

As these habits normalize, the definition of success changes. Firms that endure are those that handle volume reliably rather than those that grow fastest. Payments processors, fraud-detection systems, and compliance platforms increasingly resemble utilities, valued for uptime, accuracy, and resilience rather than brand differentiation. Venture capital behavior reflects this shift. Global fintech investment remains less than half of its 2021 peak, yet capital continues to flow toward infrastructure categories that reduce operational risk. The market signals refinement rather than reinvention.

Platform dynamics reinforce this pattern. In markets where SuperApps operate, they are no longer novelties but defaults. In parts of Asia and Latin America, a single application now handles a majority of retail digital payments while also supporting lending, bill payment, and merchant services. Small businesses accept payments, manage cash flow, and pay suppliers without switching systems. At the same time, these models remain geographically bounded. Competition policy, data-localization rules, and strong banking incumbents prevent similar concentration elsewhere. Th

e long-term outcome is not global dominance, but regional entrenchment.

Banks adapt in quieter but consequential ways. In the United States alone, bank-backed peer-to-peer and instant payment networks process hundreds of millions of transactions each month, conditioning consumers to expect immediacy even from regulated institutions. Banks increasingly operate behind the scenes, providing settlement, custody, and dispute resolution while fintech interfaces manage user experience. Their value proposition shifts away from speed and toward trust, particularly when transactions fail, are disputed, or cross borders.

Governance increasingly determines what scales. Financial data has become one of the most valuable digital assets, and governments respond accordingly. Open-finance frameworks expand portability, but within clearer limits around consent, security, and accountability. Over time, data sovereignty moves from policy abstraction to design constraint, shaping system architecture, partnerships, and market selection. Firms unable to adapt find growth constrained not by demand, but by jurisdiction.

Cross-border finance highlights both fintech’s promise and its limits. Digital rails reduce remittance costs, which have fallen from over seven percent a decade ago to under six percent globally, with some corridors significantly cheaper. For migrant workers and small exporters, this difference is material. At the same time, instant settlement magnifies weaknesses in fraud prevention and dispute resolution. Regional payment corridors and interoperability agreements emerge as partial solutions, but a fully harmonized global framework remains elusive. The future is faster and cheaper, but uneven.

At the human level, fintech’s long-term impact appears through cumulative change rather than disruption. More than three-quarters of adults worldwide now hold some form of account, up from just over half a decade earlier. Mobile phone penetration exceeds 80 percent globally, enabling basic money management in regions where bank branches never existed. Poverty does not disappear, but one of its most persistent constraints – the inability to store, move, and manage money safely – continues to erode. The challenge shifts from access to stability, literacy, and protection.

As digital finance deepens, economic participation becomes less tied to geography. Digital wallets and platform identities allow users to earn, store, and spend value across multiple ecosystems governed by private rules. These virtual economic spaces offer efficiency and inclusion, but they also raise questions around accountability, exit, and recourse. When rules change or access is restricted, remedies are often unclear. Governance increasingly confronts these realities as fintech settles into everyday life.

The long arc of fintech does not point toward another wave of disruption. It points toward settlement. The systems that endure balance speed with protection, scale with accountability, and innovation with restraint. Technology remains essential, but it no longer leads the story.

Fintech’s future is not defined by what comes next. It is defined by what stays.

Key Takeaways

- Fintech’s disruptive phase is largely complete; the industry is now defined by implementation, integration, and stabilization rather than invention.

- Three durable models coexist globally: stand-alone fintech platforms, bank-integrated fintech systems, and regionally bounded SuperApps.

- Governance, not technology, has become the primary determinant of how far and how safely fintech can scale.

- Real-time payments and mobile wallets have shifted consumer expectations toward instant, always-on financial access as a baseline.

- Data sovereignty and control over financial identity increasingly shape platform design, market access, and competitive advantage.

- Cross-border finance has become faster and cheaper, but remains uneven due to jurisdictional fragmentation and enforcement gaps.

- Banks are evolving into regulated infrastructure providers, anchoring trust, custody, and recourse beneath digital interfaces.

- SuperApps demonstrate the power of platform-based finance, but their expansion is constrained by regulation, competition policy, and cultural context.

- Fintech’s most profound long-term impact is human: reducing everyday financial friction and weakening access-related poverty constraints.

Sources

Fintech’s Structural Moment: From Challenger Narrative to Digital Financial Ecosystem

- Bank for International Settlements; Annual Economic Report 2024; – Link

- McKinsey & Company; Global Payments Report 2025; – Link

- World Bank; Global Findex Database 2025; – Link

- Reuters; Finance and Fintech Coverage; – Link

Platforms, Pressure, and Executive Trade-Offs

- KPMG; Pulse of Fintech 2024–2025; – Link

- McKinsey & Company; Global Banking Annual Review 2024; – Link

- Financial Stability Board; Financial Innovation and Structural Change; – Link

- Reuters; Fintech Investment and Banking Strategy Coverage; – Link

How Fintech Reshapes Norms, Culture, and Human Behavior

- World Bank; Global Findex Database 2025; – Link

- GSMA; State of Mobile Internet Connectivity 2024; – Link

- OECD; Digital Economy Outlook; – Link

United Nations Development Programme; Digital Finance and Financial Inclusion; – Link

How Regional Context Shapes Adoption, Impact, and Risk

- Federal Reserve; Payment Systems and FedNow Service; – Link

- European Commission; Open Finance Framework; – Link

- People’s Bank of China; Payment Systems Overview; – Link

- Reserve Bank of India; Payment and Settlement Systems; – Link

- World Bank; Financial Inclusion and Digital Payments in Africa; – Link

- Reuters; Latin America Finance and Fintech Coverage; – Link

Power, Rights, and Control in a Post-Disruption Fintech System

- Bank for International Settlements; Annual Economic Report 2024; – Link

- Financial Stability Board; BigTech in Finance and Platform Regulation; – Link

- OECD; Data Governance and the Digital Economy; – Link

- International Monetary Fund; Global Financial Stability Report; – Link

World Economic Forum; Digital Sovereignty and Platform Power; – Link

The Near Horizon: Fintech Under Governance Pressure

- Bank for International Settlements; Fast Payments and Financial Stability; – Link

- KPMG; Pulse of Fintech 2024–2025; – Link

- OECD; Artificial Intelligence in Financial Services; – Link

- Financial Stability Board; Third-Party and Cloud Risk in Financial Services; – Link

Long-Term Outlook: Where Fintech Is Settling