{kind=link}

The idea of a “super-app” has evolved from a niche technology concept to a defining structure in modern digital commerce. Unlike conventional mobile apps, a super-app combines previously independent functions—payments, messaging, shopping, transport, financial services—into a single, unified interface. In effect, the super-app becomes a digital environment where consumers manage most of their daily transactions without switching platforms.

Research increasingly treats super-apps as ecosystem anchors. They integrate third-party mini-apps, centralize identity and payments, and shape the flow of digital markets. As new entrants introduce the model into additional regions, the question is less about whether they will succeed technologically, and more about how this platform design will transform user behavior, market competition, and the broader consumer economy.

| Region | Country | Representative Super-App | Core Features |

|---|---|---|---|

| East Asia | China | WeChat (Tencent) | Messaging, payments, mini-programs, public services, mobility, e-commerce |

| Southeast Asia | Indonesia | Gojek | Ride-hailing, logistics, food delivery, payments, bill pay, merchant services |

| South Asia | India | Paytm | UPI payments, mobile wallet, banking, wealth, insurance, ticketing |

| Middle East | UAE | Careem | Ride-hailing, grocery, delivery, payments, service booking |

| Latin America | Colombia | Rappi | Delivery, grocery, pharmacy, travel booking, digital wallet |

| Africa | Togo | Gozem | Motorcycle taxis, delivery, e-commerce, mobile wallet, bill pay |

| North America | United States | Uber | Ride-hailing, food delivery, grocery, packages, integrated payments |

| Europe / Global Commerce | United States | Amazon | E-commerce, payments, grocery, pharmacy, entertainment, cloud services |

How Super-Apps Redefine the Consumer Experience

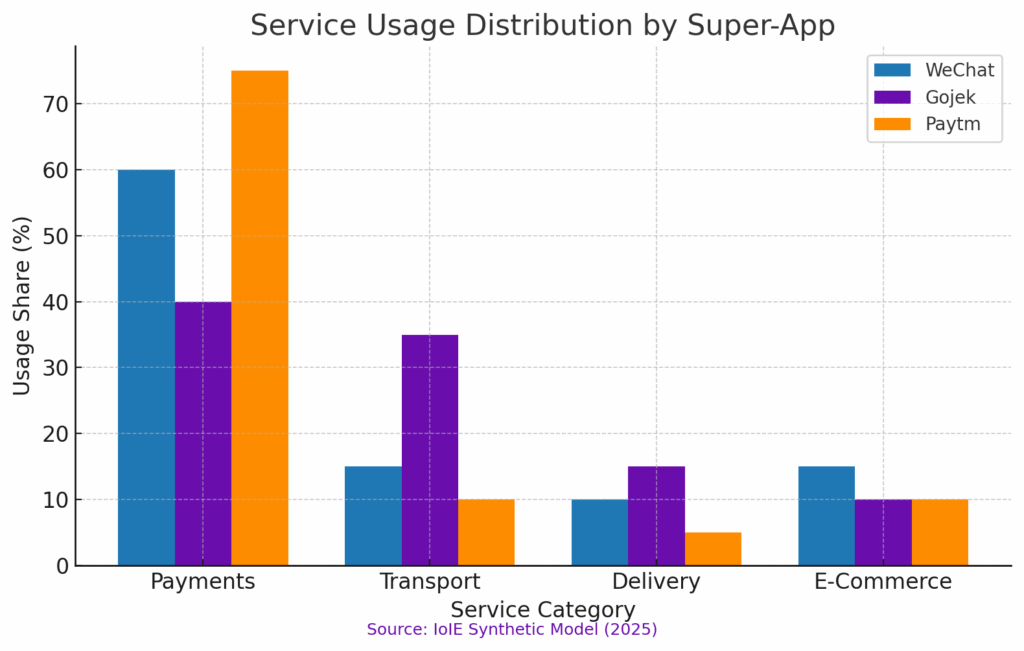

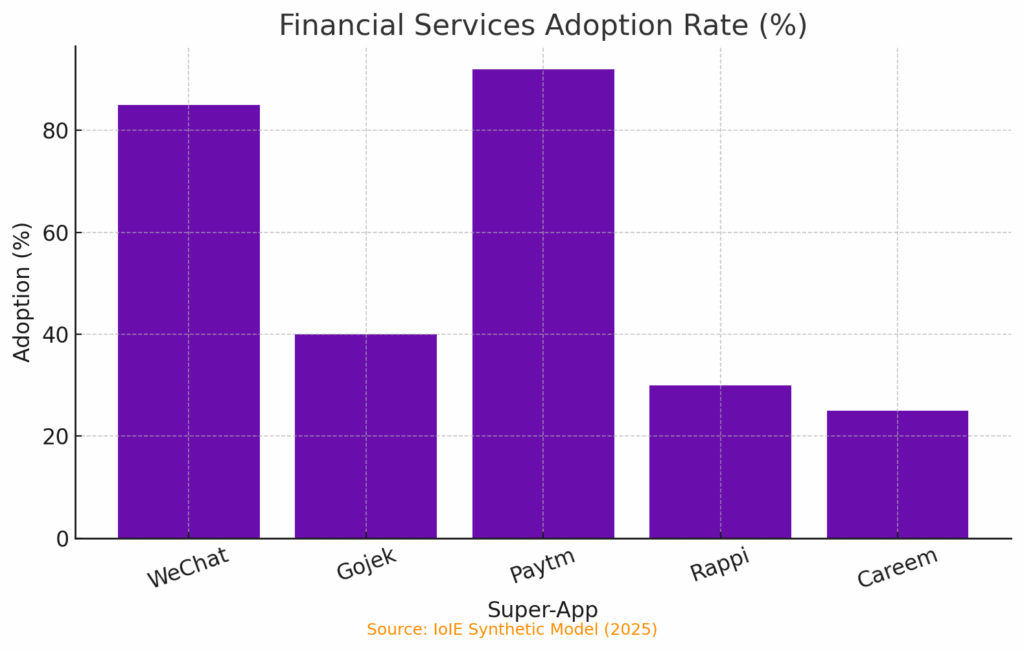

China’s WeChat remains the definitive example of the super-app model. Launched in 2011 as a simple messaging tool, it evolved into a multi-layer digital ecosystem integrating payments, mini-programs, e-commerce, mobility, and public services. For hundreds of millions of people, everyday tasks—paying bills, booking medical appointments, coordinating work, or accessing government documentation—occur entirely inside WeChat. Studies indicate that over 80 percent of users rely on super-apps primarily for payments and service booking, making these the true engines of engagement.

Southeast Asia demonstrates a different trajectory. Grab began as a ride-hailing service but expanded through direct engagement with hyper-local consumer needs: motorcycle transport, cash-based payments, and merchant-friendly financial products. Over time, it built an integrated environment combining delivery, mobility, financial services, insurance, and mapping. Analysis of Grab’s ecosystem shows that integrating services increases retention by lowering the friction of switching across apps. Consumers who start with rides or delivery often adopt payments and credit products because the platform already understands their behavior through cross-service data.

India provides a third model through Paytm, which grew by leveraging the country’s public digital infrastructure. Built initially for mobile recharges, it now offers UPI-based payments, wealth management, ticketing, and a full payments bank. Its adoption of UPI—combined with Aadhaar for identity verification—positions Paytm as part of a hybrid private–public digital ecosystem. The recent extension of UPI support to international mobile numbers pushes India’s fintech architecture into global markets, allowing the Indian diaspora to integrate directly into domestic payment systems.

Across these regions, the pattern is consistent: once a platform becomes the primary channel for payments and mobility, it transitions from being an application to becoming consumer infrastructure.

What a New Super-App Changes for Individuals

For consumers, the most immediate change is consolidation. Typical mobile usage involves app-switching across payments, messaging, shopping, and transport. A super-app collapses these into a single identity and wallet, drastically reducing friction. Research on platform operations shows that this consolidation increases transaction volume by lowering search costs and centralizing trust signals such as ratings and payment verification.

Artificial intelligence now intensifies this effect. Emerging studies describe “AI-embedded super-apps” that proactively orchestrate user journeys. Rather than waiting for user input, the platform can recommend credit products based on transaction data, plan multimodal travel routes, or surface mini-apps dynamically depending on time of day or location. While this can streamline consumer workflows, it also raises questions about data concentration and the degree to which algorithmic optimization shapes user decisions.

Consumer preference research identifies three core services—messaging, payments, and mobility—as the backbone of super-app adoption. Any emerging super-app that captures these will be well positioned to become the dominant channel through which consumers access a broad suite of digital services.

Cultural and Social Implications

Super-apps do not exist independently of cultural and social contexts. Their design tends to shape local behaviors. In China, the integration of personal messaging, workplace coordination, public services, and payments into a single interface has restructured how people interact. Many social and civic activities—community groups, religious donations, nightlife access—occur through WeChat mini-programs, merging previously separate spheres of life.

In Southeast Asia, platforms like Grab and Gojek have digitized portions of the informal economy. Street vendors, riders, and micro-retailers who previously operated outside formal systems now participate in digital marketplaces with standardized ratings, payment histories, and access to credit or insurance. This expands economic opportunity but also introduces new dependencies on platform algorithms, which determine rankings, pricing incentives, and customer visibility.

India’s super-app model ties directly into national conversations about digital sovereignty and public infrastructure. Paytm’s integration with UPI and Aadhaar links consumer services to state systems. The international expansion of UPI impacts diaspora financial habits, enabling real-time payments across borders and exporting Indian payment standards into foreign markets.

Privacy remains a central tension. Technical studies of WeChat’s mini-program protocols highlight extensive first-party tracking. As super-apps expand into new regions, data governance—how data is collected, stored, shared, and audited—will determine both public trust and regulatory intervention.

Regional Trajectories and Regulatory Variance

Super-apps rose fastest in Asia because of favorable conditions: high mobile penetration, underdeveloped card networks, and initially lighter regulatory frameworks. But this model is not universally transferable.

In the European Union, the Digital Markets Act and GDPR impose strict interoperability and self-preferencing rules. The European super-app, if it emerges, is likely to be federation-based: an interconnected environment using open banking APIs, mobility-as-a-service frameworks, and public identity systems rather than a single closed platform.

In North America, entrenched credit card networks, dominant app-store gatekeepers, and active antitrust enforcement challenge the formation of a WeChat-style super-app. Instead, the region will likely see sector-specific clusters—payments absorbing shopping and rewards, or e-commerce integrating financial services—rather than all-in-one platforms.

Parts of Africa, Latin America, and the Middle East are adopting super-apps as substitutes for fragmented physical infrastructure. In these markets, ride-hailing, mobile money, food delivery, and public health tools often converge through a single platform. Because these services serve unmet infrastructure needs, platform decisions can have disproportionate social impact.

What the New Super-App Means in Practice

The arrival of a new super-app represents a shift in how consumers access digital services. If it begins with payments, it may quickly become the default channel for everyday commerce. If it begins with messaging, it may redefine identity, communication, and social interaction. In either scenario, convenience often evolves into reliance.

The new super-app represents a reconfiguration of consumer infrastructure—an integration of services that simplifies daily life while concentrating power into a singular digital environment. How individuals, regulators, and local markets respond will determine whether super-apps become engines of innovation or sources of dependency.

Key Takeaways

- Super-apps integrate payments, mobility, messaging, retail, and financial services into a single platform, fundamentally reshaping digital consumer behavior.

- Case studies from China, Southeast Asia, and India show that super-apps become infrastructure once embedded in core routines like payments and transport.

- AI-driven personalization strengthens convenience but increases data concentration and the influence of platform algorithms.

- Cultural and regulatory contexts shape the role of super-apps, influencing labor markets, privacy norms, and public-sector integration.

- The impact of a new super-app depends on governance of data rights, interoperability, competition, and consumer exit options.

Sources

- ScienceDirect; Digital Platforms’ Growth Strategies and the Rise of Super Apps – Link

- ResearchGate; Defining a Super App and Analyzing It from an Ecosystemic Perspective – Link

- SSRN; One App for Everything: A Multidisciplinary Review of Super Apps – Link

- Wiley Online Library; Dynamic AI-Embedded Super App: A Design-Based Perspective – Link

- ScienceDirect; Consumer Preferences for Super App Services – Link

- PETS Symposium; Pervasive First-Party Tracking in a Billion-User Super-App Ecosystem – Link

- Grab; Scaling a Superapp: Grab’s Formula for Growth and Innovation – Link

- Paytm; Paytm – India’s Most Trusted Platform for BHIM UPI Payments – Link