{kind=link}

Super-apps have long been described as powerful commercial tools – massive platforms capable of blending communication, payments, transport, commerce, and social services into a single interface. Yet this description understates their true significance. In many parts of the world, super-apps now operate as social infrastructure. They serve as digital bridges connecting individuals to opportunity, inclusion, health, mobility, and prosperity. More importantly, they form part of a new technological foundation that helps societies dismantle barriers which have historically divided people by culture, geography, income, and access.

In regions where institutions struggle to reach rural communities, where financial exclusion limits opportunity, where fragmented services create daily friction, the emergence of super-apps marks a pivotal shift. Integrated digital systems – woven directly into everyday routines – allow individuals to navigate life more confidently and more securely. The result is a reconfiguration of access itself. Super-apps simplify the complex, localize the unfamiliar, and democratize pathways that were once available only to the privileged.

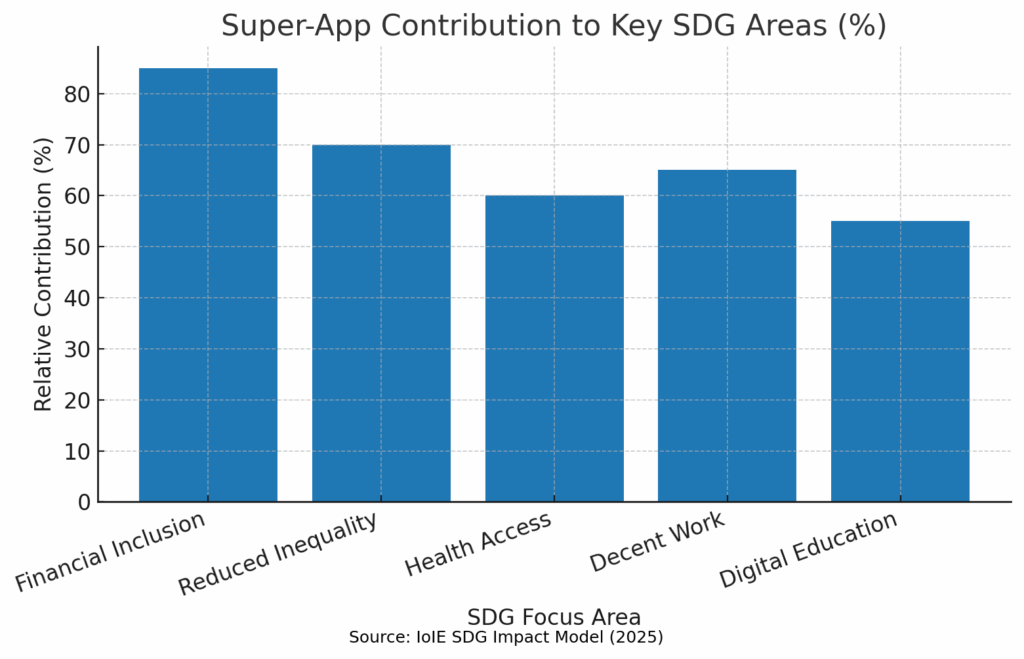

This shift corresponds directly with the ambitions of the United Nations Sustainable Development Goals. Financial inclusion, poverty reduction, improved health access, gender equality, and expanded economic participation are central themes in the SDGs, and they are precisely the domains where super-apps have demonstrated measurable impact. Their human benefit lies not in technological novelty, but in the convergence of systems – payments, mobility, identity, communication, care – into accessible digital ecosystems.

The promise of super-apps is not a digital utopia; it is a more humane, more connected, more navigable everyday life.

| Region | Company | Impact |

|---|---|---|

| Asia-Pacific | WeChat (Tencent) | Expanded digital participation for rural and urban populations; improved access to health services, e-commerce, and public services; major driver of financial inclusion through integrated payments. |

| South Asia | Paytm | Enabled large-scale UPI adoption; reduced barriers to financial access; expanded micro-loans, bill pay solutions, and digital identity services for underserved populations. |

| Southeast Asia | Gojek | Improved livelihoods through gig-economy opportunities; strengthened micro-entrepreneurship; expanded access to emergency transport, digital delivery networks, and local commerce. |

| Middle East & North Africa | Careem | Strengthened mobility and delivery infrastructure; improved safety and mobility options for women; supported early-stage digital wallets and financial access ecosystems. |

| Latin America | Rappi | Provided income opportunities in low-income urban regions; increased access to essential goods, pharmacy delivery, and digital wallet tools for underserved households. |

| Sub-Saharan Africa | Gozem | Expanded mobile-money and verification tools; enabled safer mobility; increased access to essential services and delivery support for rural communities. |

| North America | Uber | Improved mobility access for underserved populations; expanded gig-based income opportunities; early-stage integration of payments and essential delivery functions. |

| Europe | Revolut | Expanded cross-border financial access; reduced remittance friction; increased digital banking inclusion for migrants, low-income users, and mobile populations. |

Breaking Cultural and Structural Barriers Through Integrated Systems

Barriers – cultural, linguistic, geographic, economic – have always shaped the contours of opportunity. Whether one can access banking, speak the dominant language, navigate bureaucratic systems, or physically reach essential services often determines one’s life trajectory. Super-apps, intentionally or otherwise, erode these boundaries by redesigning access around intuitive, mobile-first ecosystems.

Their most profound impact is their cultural adaptability. In China, WeChat’s mini-app architecture allows rural farmers to sell produce, access subsidies, and join digital markets without requiring literacy in formal business practices. In Indonesia, Gojek’s interfaces support multiple languages and dialects, enabling service workers and customers from distinct cultural backgrounds to interact seamlessly. In West Africa, mobile-money super-apps anchored by the M-Pesa ecosystem bypass traditional banking altogether, replacing institutional hesitancy with trusted community-driven networks.

Recent UNCTAD research shows that integrated digital platforms significantly increase participation among marginalized populations by reducing the cognitive load of navigating formal systems. The Asian Development Bank also found that digital services delivered through super-apps increased engagement among low-income and rural users, who reported that integrated interfaces felt more familiar and less intimidating than standalone governmental or financial applications.

These platforms reshape cultural boundaries not by homogenizing them, but by localizing themselves – accepting that humanity’s diversity must be reflected in the tools that serve it.

Financial Inclusion as a Pathway to Human Prosperity

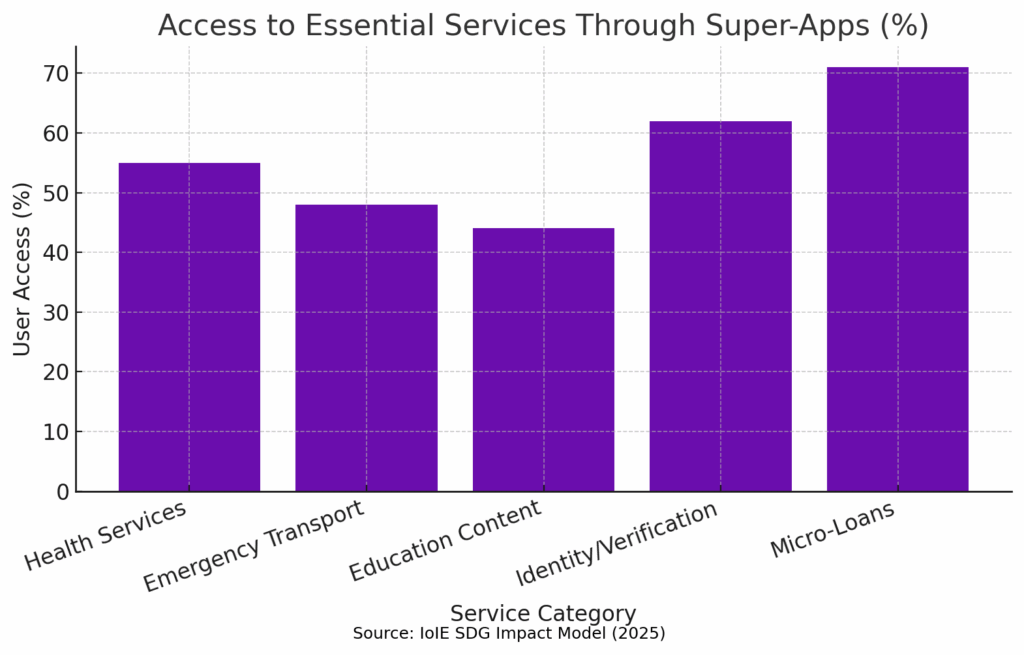

Financial inclusion is more than access to a bank account. It is access to life – credit for a business, savings for crisis resilience, remittances for family, insurance for health and recovery. Super-apps embed these tools directly into daily actions. Sending money, paying a bill, hailing a ride, buying medicine, or receiving wages requires no separate application and no complex onboarding process.

India provides one of the clearest examples. Platforms like Paytm and PhonePe leveraged the UPI payment infrastructure to create an inclusive financial landscape for hundreds of millions who previously lacked access to formal banking. These super-apps seamlessly introduced credit scoring based on behavioural data rather than collateral, enabling micro-loans to entrepreneurs, gig workers, and small merchants at a scale traditional banks could not match.

In China, Alipay’s Ant Forest linked payments to environmental action, enabling users to contribute to reforestation projects through micro-donations generated from everyday transactions. This initiative resulted in more than 200 million trees planted, blending financial inclusion with ecological participation and demonstrating how digital ecosystems can merge human well-being with environmental stewardship.

The World Bank’s latest financial inclusion report highlights a consistent pattern: regions with integrated digital ecosystems show measurable improvements in savings, credit access, and gender-inclusive economic participation. These improvements are cumulative, reinforcing prosperity for individuals and communities.

Reducing Poverty by Expanding Digital Opportunity

Poverty persists not only due to lack of resources, but due to lack of opportunity. Super-apps expand opportunity by simplifying economic entry points. Micro-entrepreneurs gain storefronts without rent. Gig workers gain access to customers without needing traditional employment. Merchants gain payment rails without requiring bank accounts or expensive POS systems.

Gojek offers one of the most studied examples. Its drivers, delivery workers, and merchants form a vast ecosystem supporting millions of livelihoods across Indonesia. Research from the Centre for Strategic and International Studies (CSIS) found that Gojek contributes over USD 7 billion annually to the Indonesian economy, much of it through income gained by individuals who previously existed on the margins of economic life.

In Latin America, Rappi serves a similar role by providing flexible work and supporting micro-commerce through digital storefronts and integrated logistics. Even imperfect gig economies can serve as transitional lifelines in regions where formal labour markets are inaccessible or scarce.

What emerges is a layered form of empowerment: super-apps do not eliminate poverty, but they meaningfully reduce vulnerability by providing economic footholds where none existed before.

Improving Health Access and Reducing Mortality Through Digital Health Ecosystems

Access to healthcare is one of humanity’s starkest divides. Super-apps increasingly bridge this gap by integrating health services into their digital ecosystems.

During the COVID-19 pandemic, these platforms became essential public-health infrastructure. WeChat consolidated vaccination records, test results, and medical appointment bookings. Grab and Gojek managed essential goods delivery and supported health-related transport. Paytm in India integrated telemedicine connections, allowing users in remote villages to consult doctors digitally.

These interventions had lasting effects. According to The Lancet Digital Health, the use of integrated digital health platforms reduces diagnostic delays, improves compliance with treatment appointments, and increases access to medical expertise in rural and remote communities. In West Africa, partnerships with Gozem enabled emergency transport that lowered response times in regions without traditional ambulance systems.

By embedding health into everyday digital life, super-apps reduce the structural causes of preventable mortality: delayed care, inadequate information, and lack of access.

Prosperity Through Connectivity and Digital Participation

Prosperity is more than financial gain. It is the capacity to navigate life with stability, security, and possibility. Super-apps contribute to this through connectivity – social, economic, and informational.

When communities gain access to payments, identity verification, logistics, digital communication, savings products, and essential services through a unified interface, daily life becomes more navigable and resilient. The OECD’s work on digital transformation shows that small and medium-sized enterprises dramatically increase productivity when integrated into digital ecosystems offering low-cost payments and logistics.

In regions with limited infrastructure, super-apps often become the infrastructure. They serve as the railways of the digital age, carrying information, goods, and opportunity across distances that physical systems cannot bridge.

What super-apps ultimately offer is a redistribution of capability – tools that enable individuals to support themselves, families to stabilize their futures, and communities to thrive.

Difference Makers

Super-apps are not simply technological marvels or commercial engines. They are human systems – digital environments built to expand access, reduce barriers, and connect individuals to the essential structures of modern life. They align closely with the core ambitions of the UN Sustainable Development Goals by lowering obstacles to financial inclusion, reducing poverty through digital participation, improving health outcomes, and offering new pathways towards prosperity.

They do not replace traditional institutions. Instead, they strengthen them by extending their reach into everyday life. They do not erase inequality, but they diminish the forces that reinforce it. And they do not create separate digital nations; they amplify the digital capacities of existing societies, helping humanity move toward a more just, more connected, and more sustainable future.

Super-apps help humanity not only through innovation, but through compassion embedded in code – systems designed to lift, to link, and to empower.

Key Takeaways

- Super-apps reduce cultural, economic, and geographic barriers by integrating key services into accessible digital systems.

- They significantly advance financial inclusion, enabling underserved populations to access payments, credit, savings, and essential services.

- Case studies from Asia, Africa, and Latin America show measurable gains in poverty reduction, micro-enterprise growth, and labour mobility.

- Integrated digital health features improve access to treatment, reduce delays, and support public health infrastructure.

- Super-apps contribute directly to progress on multiple UN Sustainable Development Goals, particularly inclusion, health, and economic opportunity.

Sources

- ScienceDirect; Digital Platforms’ Growth Strategies and the Rise of Super Apps – Link

- INSEAD Knowledge; Super-Apps: How to Create a Mass Market of One – Link

- Wiley; The Future of Digital Payments Market Infrastructures – Link

- IIASA; Digitalization Will Transform the Global Economy – Link

- Institute of Internet Economics; Virtual Nations & Digital Economies – Link

- New Media & Society; Super-appification: Conglomeration in the Global Digital Economy – Link

- Heliyon; Consumer Preferences for Super App Services – Link

- Lancet Digital Health; Improving Access Through Digital Health Platforms – Link

- World Bank; Global Financial Inclusion Report – Link

- Asian Development Bank; Digital Platforms for Inclusive Growth – Link

- CSIS Indonesia; Gojek’s Economic Impact Assessment – Link

- OECD; Digital Transformation and SME Productivity – Link