{kind=link}

The Internet of Things (IoT) has moved beyond hype and experimentation. It now defines the foundation of digital competitiveness across industries, governments, and societies. In the coming five years, IoT will expand from isolated deployments to an integrated global infrastructure that connects production systems, cities, and everyday life. Its trajectory is accelerating—powered by cheaper sensors, faster networks, and the rising value of data as an economic asset.

What once seemed futuristic is now structural. Industrial equipment, energy grids, vehicles, and consumer devices are merging into continuous feedback systems, turning real-world processes into sources of intelligence. Between now and 2030, this integration will reshape cost structures, productivity, and the geography of growth. Regions capable of embedding IoT deeply into their economic fabric will capture new forms of advantage, while those lagging in connectivity and data governance risk being left behind.

Phase I: From Pilot to Platform (2024–2025)

The next twelve to eighteen months will mark a decisive shift as companies move from proof-of-concept to scaled rollout. IoT Analytics estimates that by the end of 2024, there will be approximately 18.8 billion connected devices worldwide, growing 13 percent annually. Firms are transitioning from pilot experiments toward full integration in logistics, retail, manufacturing, and asset management.

These early deployments focus on tangible efficiency—predictive maintenance, supply-chain monitoring, and remote equipment management. Industrial players report reduced downtime of 20–30 percent and measurable improvements in uptime and throughput. The immediate economic gains come from operational cost reduction and efficiency, but the broader transformation lies in how IoT establishes data feedback loops.

Regions with robust infrastructure—North America, Europe, and advanced Asian economies—are consolidating leadership during this phase. Connectivity upgrades through 5G and LPWAN networks allow firms to build real-time visibility into production and distribution. For emerging economies, low-cost sensors and cloud-based platforms are enabling “leapfrog” effects, where sectors like agriculture, urban infrastructure, and logistics can adopt connected systems without legacy constraints.

The first phase thus focuses on foundational layers: sensors, connectivity, and initial analytics. Economic benefits are incremental but cumulative—each connected process generates data that becomes an input for future optimization.

Phase II: Expansion and Monetization (2025–2027)

Between Years 2 and 3, IoT transitions from infrastructure deployment to business integration. Enterprises begin building hybrid edge–cloud architectures, processing data locally for speed while centralizing analytics for insight. According to Mordor Intelligence, the Industrial IoT (IIoT) market will grow at approximately 25 percent CAGR through 2030, reflecting how connected systems are becoming embedded in industrial operations.

The emphasis shifts from saving costs to creating value. Companies monetize data through predictive analytics, dynamic pricing, and real-time decision models. For instance, General Electric’s Predix platform helps manufacturers predict component failure, while Siemens’ MindSphere integrates machines and analytics to optimize production. These systems mark the transition from “connected devices” to “intelligent infrastructure.”

At the same time, consumer IoT accelerates. Affordable devices and improved network coverage bring smart homes, wearable health monitors, and connected vehicles into mainstream use. In markets like China, India, and South Korea, adoption rates outpace Western economies due to lower hardware costs and stronger state-led digital programs.

The economic effects of this second phase are structural. Data itself becomes a traded commodity. Firms begin to compete on who can derive the most actionable insights from connected systems. The ability to integrate data from operations, customers, and suppliers creates a new layer of strategic differentiation.

Phase III: Systemic Integration (2028–2030)

By Years 4 and 5, IoT becomes inseparable from the functioning of modern economies. According to Ericsson, total global IoT connections are forecast to rise from 18.8 billion in 2024 to around 43 billion by 2030. At this point, IoT infrastructure underpins nearly every major industry—manufacturing, healthcare, logistics, agriculture, and energy.

Economic systems evolve around continuous data exchange. Cities operate as interconnected organisms, industries optimize in real time, and services become predictive rather than reactive. Hospitals use IoT-enabled patient monitoring to reduce readmission rates; logistics networks use predictive routing to minimize fuel waste; utilities use smart grids to balance supply and demand autonomously.

The structural outcome is a shift from ownership to service. Products become recurring service models—what analysts describe as everything-as-a-service (XaaS). Rolls-Royce’s Power by the Hour model exemplifies this transformation, charging customers for engine uptime rather than ownership. The same logic extends across sectors: mobility-as-a-service, energy-as-a-service, and factory-as-a-service.

Economically, this phase represents a redefinition of value creation. The core assets of a competitive firm are no longer physical but informational—the capacity to capture, interpret, and monetize data. For countries, competitiveness becomes a function of how well their digital infrastructure can support secure, interoperable, and scalable IoT systems.

Regional Divergence and Economic Implications

North America remains the largest IoT market by revenue, commanding around 36 percent of global share as of 2023, according to Grand View Research. With mature cloud ecosystems, advanced 5G deployment, and a deep base of enterprise users, the United States leads industrial and commercial IoT. Firms such as Amazon Web Services (AWS) and Microsoft Azure IoT provide standardized architectures for scalability, while manufacturers like Caterpillar use IoT for fleet monitoring and maintenance optimization.

However, as the North American market matures, growth slows. Expected CAGR through 2030 is approximately 7.6 percent, reflecting saturation rather than stagnation. The region’s challenge will be ensuring accessibility for smaller firms and maintaining competitiveness amid rising cybersecurity and regulatory costs.

Asia-Pacific will drive the fastest growth globally. The region’s IoT economy benefits from both scale and policy coordination. China’s “New Infrastructure Plan” and India’s Smart Cities Mission are embedding IoT directly into industrial and civic systems. Smart factories in Shenzhen already use connected robotics and AI-based visual inspection, while agricultural IoT systems in India and Indonesia enable precision irrigation and soil monitoring.

According to the Asian Development Bank, IoT-driven productivity gains could add 1.5 percent to regional GDP growth annually through 2030. Yet, disparities remain: high connectivity in South Korea and Japan contrasts with infrastructure bottlenecks in parts of Southeast Asia. Governance and standardization will determine whether the region achieves integrated growth or fragmented adoption.

Europe takes a measured but strategically significant path. The continent’s emphasis on sustainability and regulation aligns IoT integration with environmental objectives. The European Commission’s Digital Europe Programme and Germany’s Industry 4.0 initiative foster industrial modernization and resource efficiency. European firms are pioneering connected systems that align with decarbonization goals—smart grids, predictive maintenance, and real-time waste reduction.

However, Europe’s fragmented digital landscape slows regional coherence. Divergent national regulations, legacy infrastructure, and cost barriers hinder scale compared to Asia or the United States. Nevertheless, Europe’s leadership in ethical data governance may become a global model for responsible IoT integration.

Emerging markets—including Latin America, Africa, and the Middle East—represent IoT’s long-term frontier. While infrastructure and connectivity remain challenges, the economic potential is immense. Projects like Brazil’s agritech IoT systems have improved water efficiency by 25 percent, and Saudi Arabia’s NEOM is building a city designed entirely around IoT-enabled automation.

If effectively implemented, IoT could add up to 5 percent to GDP in these regions by 2030 through efficiency, new business models, and job creation, according to the World Bank. However, without policy investment and digital skills development, the benefits risk concentrating in limited sectors, widening the digital divide.

Economic and Policy Outlook

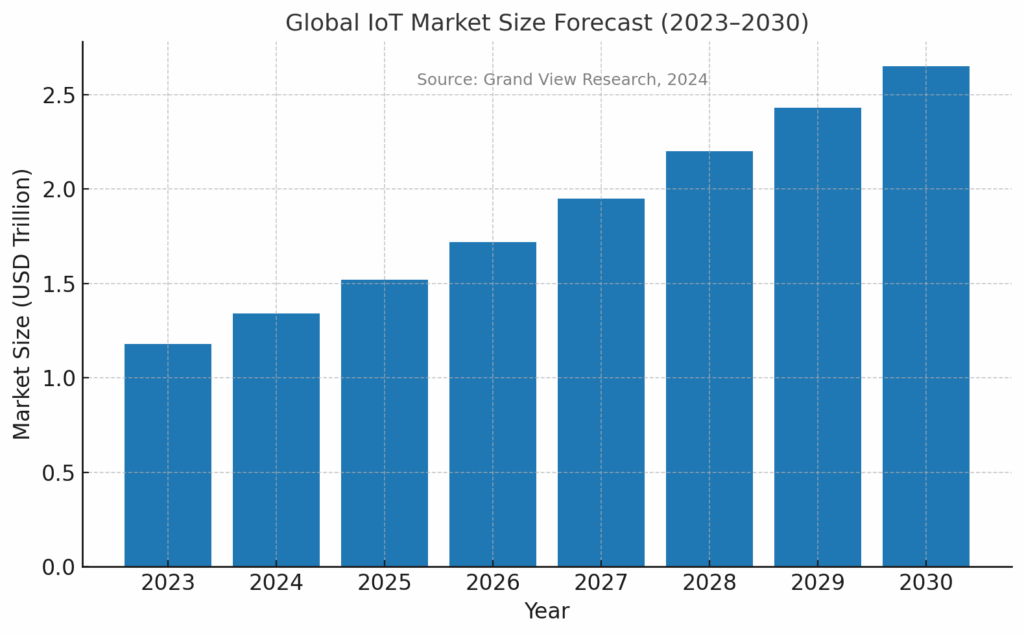

The global IoT market, valued at USD 1.18 trillion in 2023, is projected to reach USD 2.65 trillion by 2030, according to Grand View Research. This expansion represents more than technological diffusion—it signals a systemic shift in how economies allocate capital and labor.

The key macroeconomic levers are:

- Efficiency: Predictive maintenance and automation reduce operating costs and capital waste.

- Monetization: Data transforms into new revenue streams, particularly in analytics and AI-enhanced services.

- Transformation: Business models pivot toward service-based structures, creating new competitive hierarchies.

Policy will define the global distribution of IoT’s economic benefits. Countries adopting coherent strategies for data sovereignty, privacy, and interoperability will attract investment and innovation. The OECD notes that nations with clear IoT governance frameworks experience faster private-sector deployment and lower compliance risk.

By contrast, fragmented regulations risk producing “data islands,” where incompatible standards and protectionist laws limit the scalability of IoT ecosystems. Already, the number of countries implementing cross-border data restrictions has grown from 10 in 2010 to more than 65 by 2025, highlighting the emergence of competing digital blocs.

Labor markets will evolve in parallel. The World Economic Forum projects that IoT, AI, and automation will together create 97 million new digital jobs by 2030, offsetting most displacement from routine work. Economies investing in digital literacy and cloud infrastructure will capture the multiplier effects; those that delay will face structural unemployment in legacy sectors.

The Decade of Connected Economies

By the early 2030s, IoT will be the connective tissue of the global economy. Industrial competitiveness will depend on how efficiently data circulates between systems, sectors, and borders. The economic logic of connectivity will replace the old logic of scale: advantage will derive not from size, but from integration.

In manufacturing, connected supply chains will coordinate production dynamically. In cities, infrastructure will balance resource flows autonomously. In services, predictive analytics will enable constant adaptation to demand. For nations, the measure of success will be not GDP alone but digital capacity—the ability to sustain continuous, data-informed productivity.

The five-year trajectory of IoT integration thus defines more than a technological shift—it marks the emergence of a new phase of globalization. As connectivity deepens, economies will compete not only in output but in the intelligence of their networks. The future of competitiveness will belong to those who understand that the real economy is now a connected one.

Sources

IoT Analytics — Number of Connected IoT Devices Growing 13% to 18.8 Billion Globally — Link

Mordor Intelligence — Industrial Internet of Things (IIoT) Market Size and Forecast 2030 — Link

Ericsson — IoT Connections Outlook – Mobility Report 2024 — Link

Grand View Research — Internet of Things (IoT) Market Size, Share & Trends Report, 2030 — Link

World Bank — Digital Development Report 2024 — Link

Asian Development Bank — Industry Transformation and IoT in Asia 2025 — Link

World Economic Forum — Future of Jobs and IoT Integration Report 2025 — Link

European Commission — Digital Europe Programme and Cyber Resilience Act — Link

Harvard Business Review — How IoT Redefines Productivity — Link