{kind=link}

The global rise of the super-app marks a transformation far more economically significant than the evolution of mobile software. It represents the emergence of a new economic architecture—one in which payments, labour, consumption, mobility, and finance converge into highly integrated, data-rich digital environments. This transformation is not about the creation of virtual nations or digital sovereignties. Instead, it is about the expansion and deepening of national digital economies, where super-apps serve as the connective tissue linking citizens, firms, and institutions into the digital fabric of economic life.

This shift reflects a broader trend where nations are developing virtual nation economies, digital layers that extend the terrestrial economy into a structured, regulated and interoperable network of payment systems, identity frameworks, digital services and commercial platforms. Super-apps have become central elements within this emerging structure. They do not replace state authority, but they do reorganize the channels through which economic activity occurs, mediating daily interactions between citizens and the market in ways that conventional institutions never achieved.

The story of the super-app is therefore not one of technological novelty but of structural economic change. Understanding this shift requires examining how these platforms create digital economies, how they fold citizens more deeply into national commercial systems, how regulators respond to their expanding role, and how global economic forces shape their evolution.

The Digital Economy as an Integrated System

The digital economy should not be viewed simply as society’s migration online. It is the reorganization of economic fundamentals—production, consumption, labour, capital formation, and service delivery—into digital systems governed by algorithms, data flows and platform incentives. Super-apps accelerate this transition through integration. They serve as economic assemblers, pulling together previously fragmented commercial and financial activities into a single interface.

In traditional economies, citizens interact with markets through distinct channels: a bank for payments, physical shops for retail, taxis for mobility, government offices for services. In a super-app environment, these activities converge. Payment credentials, behavioural data, identity information and transaction histories coexist within one coordinated ecosystem. This convergence lowers transaction costs, increases efficiency, and formalizes previously informal markets.

Unlike sovereign entities, super-apps do not create their own economic borders. Instead, they expand the digital frontiers of the national economy, providing citizens with the infrastructure to participate more easily in commerce, access financial tools, and engage with labour markets. Their influence is not extraterritorial; it is integrative.

Economic Integration Through Payments and Identity

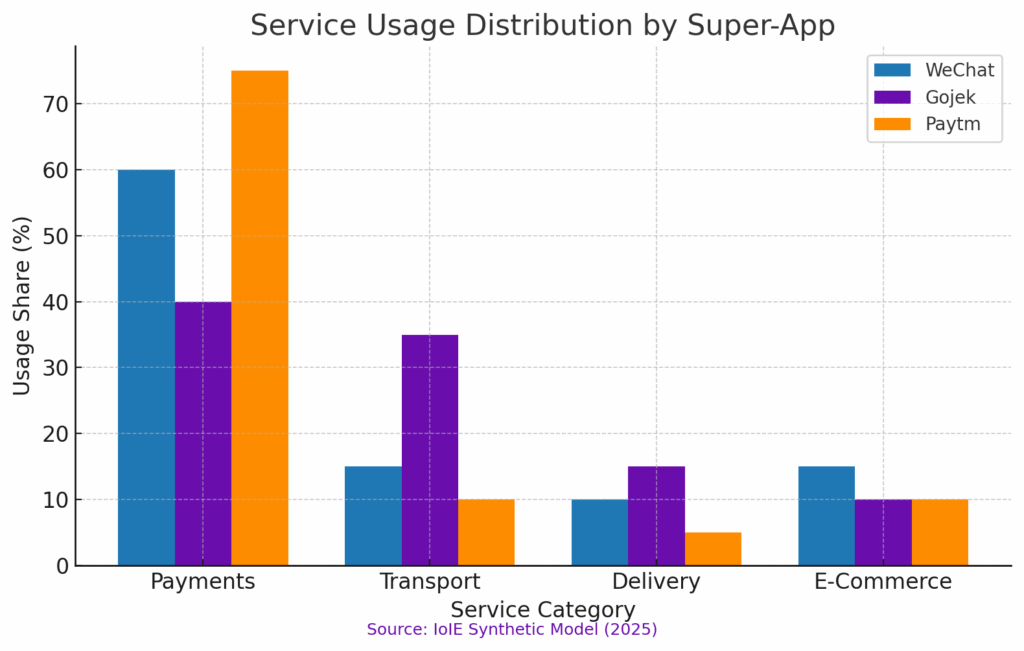

Most super-apps achieve scale by starting with payments. A digital wallet is the foundational tool of economic integration. Once users rely on the platform for everyday transactions—groceries, transportation, utility bills—the platform becomes economically indispensable.

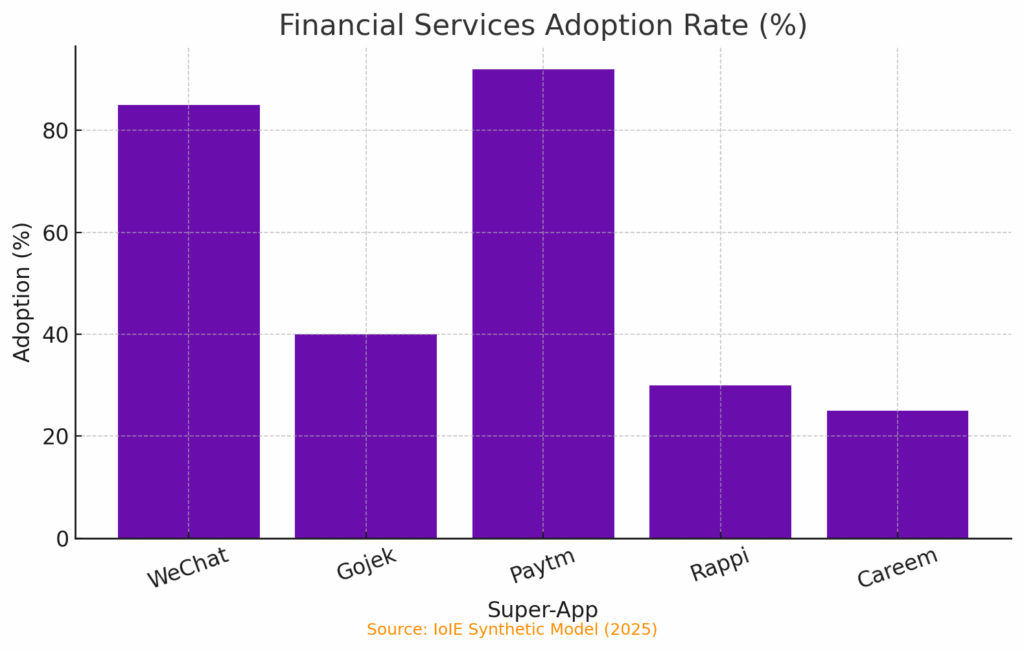

Because payments generate measurable, high-frequency metadata, they serve as the informational backbone of the digital economy. They enable platforms to understand consumption patterns, credit risk, labour supply, mobility routes and price sensitivity. When combined with identity systems—whether platform-specific or nationally integrated—the result is a powerful mechanism for coordinating economic activity. Consumers gain easier access to financial services; merchants gain digital visibility; and the state benefits through improved economic traceability and expanded participation in formal financial systems.

This dynamic is especially powerful in emerging markets, where super-apps often leapfrog traditional infrastructure. They provide micro-merchants with access to paying customers, enable new entrants to accept digital transactions, and create credit rails that reduce dependency on collateral-based lending.

The importance of payments lies not in the technology itself but in the way it binds the user to the digital economy. It is an economic tether, not a political one.

The Transformation of Merchant and Labour Markets

Super-apps bring a vast portion of micro-commerce into the formal digital economy. Street vendors, small shopkeepers, gig workers and informal service providers—traditionally excluded from digital ecosystems—gain new pathways into the national market. They can accept digital payments without expensive hardware, advertise services on equal footing with larger competitors, and access credit products that rely on behavioural data instead of collateral.

The result is a measurable shift in national economic composition. Informal markets shrink; digital transactions grow; and the structure of retail competition is reshaped around platform discoverability rather than location or scale. For labour, the effect is equally profound. National labour markets become digitally mediated, with algorithmic systems determining task allocation, pricing, incentives and visibility. The platform becomes an economic intermediary—a matchmaker, coordinator and regulator of work supply.

These developments do not create independent digital societies. They reinforce the terrestrial economy by formalising previously opaque economic activities. But they also introduce new challenges: worker protections, algorithmic fairness, platform-induced wage compression and potential overdependence on a single commercial interface.

| Region | Names | Services |

|---|---|---|

| Asia-Pacific | WeChat, Alipay, Gojek, Grab | Payments, mobile wallets, messaging, mini-apps, ride-hailing, delivery, e-commerce, financial services, public service access |

| South Asia | Paytm, PhonePe | UPI payments, digital wallets, bill pay, wealth management, insurance, ticketing, merchant services |

| Middle East & North Africa | Careem, STC Pay | Ride-hailing, food/grocery delivery, payments, mobile wallets, travel services, lifestyle bookings |

| Sub-Saharan Africa | Gozem, M-Pesa Super-App | Mobile money, merchant payments, micro-loans, bill pay, transport, delivery, e-commerce |

| Latin America | Rappi, MercadoPago | Delivery, courier services, grocery, pharmacy, travel booking, digital wallet, credit, rewards |

| North America | Uber, Cash App | Mobility, food delivery, parcel delivery, payments, P2P transfers, banking, investing |

| Europe | Revolut, Bolt | Digital banking, multi-currency payments, credit, investing, insurance, mobility, food delivery |

External Economic Forces: Global Power Structures and Market Pressures

Although super-apps anchor themselves within national economies, their development is influenced by global forces—capital, technology standards, cross-border competition and geopolitical tensions.

Global capital flows play a decisive role in super-app expansion. Venture capital, private equity and sovereign wealth funds often shape strategic priorities, encouraging aggressive growth, financialisation of services and rapid diversification. This external investment weaves national digital economies into global financial circuits, exposing them to shifts in investor sentiment and risk tolerance.

Technological dependencies create further constraints. Operating system policies, international cloud providers, data localisation regimes and cross-border payment regulations limit how super-apps can scale or which services they can legally host. These constraints embed super-apps within a global architecture of digital infrastructure, where national economic ambitions must negotiate with private global actors.

Cross-border platform competition introduces additional pressures. When platforms like WeChat, Grab or Gojek expand internationally, they carry with them not only technological models but economic behaviour patterns. Host nations must respond by shaping policy around digital sovereignty, competition frameworks and economic inclusion in order to protect their domestic digital economies.

Thus, while super-apps are nationally rooted, they operate within an international economic environment that influences their capacities, risks and strategies.

Regulation: The Architecture of a Super-App-Compatible Economy

Regulatory systems must evolve when economic participation migrates into digital platforms. Super-apps operate at the intersection of numerous regulatory categories: finance, competition, labour, transportation, data protection, cybersecurity and consumer rights. No traditional framework was designed for entities that span so many sectors simultaneously.

Regulators face the challenge of enabling innovation while preventing structural dependence or anti-competitive behaviour. Financial regulators must determine how embedded finance fits within banking systems. Competition authorities must assess how vertical integration affects market entry. Labour ministries must address rights for platform-mediated workers. Data regulators must ensure that consumer information—which becomes the raw material of digital economic coordination—is governed ethically and securely.

The goal is not to restrain super-app growth but to align it with national economic interests. This requires standards for interoperability, transparent algorithms, data portability, and fair platform access rules. Effective regulation positions the super-app as a contributor to the national virtual nation economy rather than a dominant gatekeeper.

Super-Apps Within National Virtual Nation Economies

National virtual nation economies, as framed by the Institute of Internet Economics, are not substitutes for the state but digital extensions of national institutions. They represent the integrated layer of identity, services, payments and data governance that overlays the physical economy. Super-apps are increasingly embedded within this layer.

They amplify economic participation by reducing friction. They strengthen financial inclusion by simplifying access to credit and savings tools. They expand the reach of national payment systems and accelerate the adoption of digital identity frameworks. They generate granular data that can inform better public policy. And they provide economic lifelines for merchants and workers participating in digital markets for the first time.

In this sense, super-apps help build and operate the economic infrastructure of national digital systems, reinforcing and expanding economic activity rather than supplanting state authority. Their influence is economic, not sovereign. Their growth strengthens the digital foundations of the terrestrial economy and extends the reach of national economic systems into everyday life.

Conclusion

Super-apps represent a critical evolution in economic infrastructure. They integrate daily economic activities into coordinated digital systems, transforming how citizens engage with markets, participate in labour economies, manage finances and access services. Far from constructing digital sovereignties, they reinforce and expand the national digital economy, serving as powerful intermediaries that accelerate formalization, efficiency and economic inclusion.

The broader national virtual nation economy provides the regulatory and institutional context that ensures super-apps operate in alignment with national priorities. This digital layer—formed by identity frameworks, payment systems, data governance and platform regulation—supports the integration of citizens and firms into a coherent, modern economic structure.

As super-apps grow, nations must design regulatory and economic strategies that harness their integrative power while safeguarding competition, labour fairness and data rights. The future of national digital economies will not be built by platforms alone, but by the interplay of platform innovation, state regulation and citizen participation. The challenge ahead is ensuring that super-apps strengthen democratic economic outcomes rather than concentrating economic power in ways that limit choice, transparency and opportunity.

Key Takeaways

- Super-apps function as economic infrastructure that integrates payments, labour, retail and financial services within national digital economies.

- They reinforce, rather than replace, terrestrial economic systems by formalising transactions and broadening economic participation.

- Their expansion is shaped by global capital flows, technology standards and international platform competition.

- Regulations governing finance, competition, labour and data must evolve to align super-app growth with national economic interests.

- Super-apps operate as central components of national virtual nation economies, strengthening economic inclusion and digital market access.

Sources

Sources

- ScienceDirect; Digital Platforms’ Growth Strategies and the Rise of Super Apps – Link

- INSEAD Knowledge; Super-Apps: How to Create a Mass Market of One – Link

- Wiley; The Future of Digital Payments Market Infrastructures – Link

- IIASA; Digitalization Will Transform the Global Economy – Link

- Institute of Internet Economics; Virtual Nations & Digital Economies – Link

- New Media & Society; Super-appification: Conglomeration in the Global Digital Economy – Link

- Heliyon; Consumer Preferences for Super App Services – Link

- arXiv; SoK: Decoding the Super App Enigma: Security Mechanisms, Threats, and Trade-offs – Link

- arXiv; Super Apps and the Digital Markets Act – Link

- Business & Social Trends Journal; The SuperApp Implementation in Business – Link

- Visa Consulting & Analytics; Succeeding With Super Apps – Link

- MDPI Sustainability; The Rise of Superapps in Emerging Countries – Link

- Journal of Money, Credit and Banking; The Rise of E-Wallet Super-Apps and Buy-Now-Pay-Later – Link