{kind=link}

The End of an Era in Bitcoin Mining

For much of Bitcoin’s early life, mining still carried the aura of open participation. The protocol was permissionless, the hardware curve had not yet hardened into a capital race, and the story of the network could still be told through dispersed operators chasing asymmetric upside from a spare room, a garage, or a small hosting arrangement. That era has ended. After the April 2024 halving cut the block subsidy from 6.25 to 3.125 bitcoin, the economics of securing the network shifted even more decisively toward operators able to finance specialized fleets, negotiate industrial power terms, and tolerate thinner margins over longer periods. What disappeared was not access in a technical sense. It was access in an economic sense.

What that means is larger than a change in market structure. A network once sustained, at least in part, by distributed enthusiasts is now increasingly upheld by companies working within the disciplines of project finance, energy procurement, and asset utilization. In a 2025 industry survey covering firms representing 48% of global mining activity, 41% of participants were publicly listed, while the United States and Canada together accounted for more than four-fifths of reported mining activity. Those are the markers of an industrial sector, not a frontier hobby. Bitcoin may still be discussed as a decentralized monetary project, but the production of its security is now shaped by a much narrower circle of economically advantaged actors.

Seen through that lens, the disappearance of the grassroots miner is not incidental. It is the moment Bitcoin stops behaving like a fad secured by enthusiasm and starts behaving like a high-cost production economy. The change is subtle in code, but dramatic in practice. Risk and reward now resemble the logic of extraction industries, where capital intensity, operational scale, and resilience under pressure matter far more than ideology or early-mover romance.

| Bitcoin Mining Then and Now | ||

|---|---|---|

| Dimension | Earlier Era | Current Era |

| Who could participate | Individuals and small operators with modest equipment and tolerance for volatility | Large firms with financing capacity, industrial procurement, and infrastructure access |

| Core advantage | Early entry and informal experimentation | Scale, power contracts, machine efficiency, and balance-sheet resilience |

| Economic model | Speculative upside with lower capital barriers | Execution-driven industrial business with cost-curve pressure |

| Main constraint | Technical learning curve | Capital intensity, hardware refresh cycles, and energy sourcing |

| Meaning for Bitcoin | Network still felt frontier-like and participatory in practice | Security increasingly produced by industrial actors under real-world cost constraints |

| Sources: Cambridge Centre for Alternative Finance; Cambridge Digital Mining Industry Report; NBER; Decentralized Mining in Centralized Pools; |

||

Bitcoin as a Virtual Commodity with Real-World Constraints

If Bitcoin is becoming commodity-like, the reason lies not only in scarcity but in the conditions under which new supply is produced. Gold is constrained by geology. Bitcoin is constrained by protocol. Yet once production depends on scarce inputs, falls onto a cost curve, and rewards only those able to keep operating when returns deteriorate, the distinction between physical extraction and digital extraction starts to narrow. Bitcoin remains virtual, but the system that produces it now bears a striking resemblance to terrestrial commodity production.

At 138 terawatt-hours of annual electricity use in 2025, equivalent to roughly 0.5% of global electricity consumption, Bitcoin mining no longer sits outside the terrestrial economy. In the United States alone, federal estimates placed cryptocurrency mining at roughly 0.6% to 2.3% of national electricity demand in 2023. That scale matters because it ties Bitcoin directly to the realities that govern heavy users of power everywhere else: grid pricing, transmission constraints, political scrutiny, and the search for low-cost supply. Once production begins to compete for energy on those terms, Bitcoin stops looking like a detached digital curiosity and starts looking like a virtual commodity with physical dependencies.

The composition of mining’s energy mix reinforces the point. More than half of the sector’s power base in 2025 came from sustainable sources, including 42.6% renewables and 9.8% nuclear, while natural gas alone accounted for 38.2% and coal fell below 9%. Those figures are useful not because they settle a reputational debate, but because they show miners behaving like other industrial consumers, constantly arbitraging the relative cost, reliability, and availability of power. Mining has become a power-sourcing exercise, and that fact alone places it closer to the world of industrial production than to the mythology of early crypto participation.

This is where the commodity analogy becomes more exact. In physical mining, investors often look to standardized cost measures to judge who can keep producing through a difficult cycle. Bitcoin mining is moving toward a comparable discipline. Operators are increasingly judged by whether they can stay low on the cost curve after electricity, machine refresh, and overhead are accounted for. The protocol remains decentralized by design, but the production of network security is becoming more concentrated in economically advantaged hands. That distinction matters. Industrial concentration in production does not automatically eliminate protocol decentralization, but it does redefine who can participate meaningfully in securing the network.

The New Rules of Bitcoin Mining Profitability

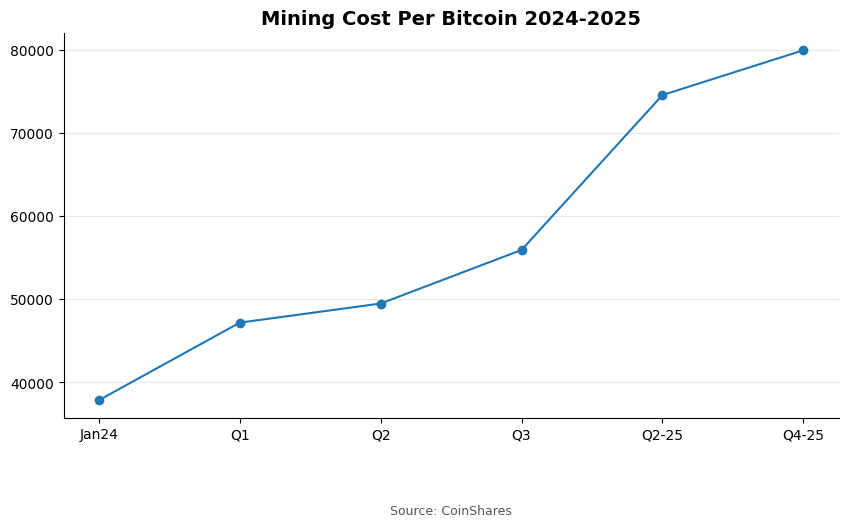

Since the halving, profitability has become less about directional optimism and more about execution. Reporting in mid-2024 showed listed miners already wrestling with lower rewards, rising network difficulty, and softer investor enthusiasm for mining equities even after the sector raised more than $3 billion in the first quarter of that year. By late 2025 the pressure was showing up more clearly in production economics. The weighted average cash cost to produce one bitcoin among listed miners reached about $74,600 in Q2 2025, while later analysis placed the Q4 2025 figure near $80,000, with all-in costs materially higher once depreciation and stock-based compensation were included. The old assumption that a rising bitcoin price would lift the whole sector has become harder to defend.

| What Now Determines Mining Profitability | ||

|---|---|---|

| Profitability Driver | Why It Matters More Now | Implication for Smaller Operators |

| Electricity sourcing | Energy has become the dominant variable in staying low on the cost curve | Less leverage in negotiating long-term contracts or accessing surplus generation |

| Hardware generation | New ASIC cycles compress margins for operators using older fleets | Higher reinvestment burden just to remain competitive |

| Financing access | Public markets and larger balance sheets support expansion and machine refresh | More exposed to tightening capital conditions and distress sales |

| Operational uptime | Downtime now carries a higher penalty after subsidy compression | Lower redundancy and fewer optimization resources magnify disruption risk |

| Strategic optionality | Sites with AI or HPC conversion potential command additional value | Limited ability to pivot infrastructure toward higher-value compute uses |

| Sources: CoinShares; Bitcoin Mining Report Q4 2025; Reuters; AI’s race for U.S. energy butts up against bitcoin mining; | ||

Beneath those averages sits a narrower and harsher equation. Electricity remains the decisive input, but machine efficiency, fleet age, uptime, cooling design, and financing costs now shape the difference between survival and forced restructuring. New ASIC generations can improve economics meaningfully, yet they also raise the cost of staying relevant. Operators no longer reinvest simply to expand. They reinvest to avoid falling behind. That is the mechanism by which the small miner keeps disappearing: the business no longer rewards persistence at low scale. It rewards privileged access to capital, power, and equipment turnover.

What emerges is a global cost curve that looks familiar to commodity producers. Those operating near the bottom can withstand difficult stretches and even consolidate when others falter. Those higher up move toward asset sales, mergers, shutdowns, or strategic pivots. Profitability, then, is no longer chiefly a story about catching the next bitcoin rally. It is a story about who can run an energy-intensive production business better than everyone else.

Scale, Diversification, and the Pull of Larger Infrastructure Markets

While thinner mining margins have intensified cost discipline, they have also changed how the market values mining assets themselves. Analysts expected as much as 20% of bitcoin miner power capacity to pivot toward AI by the end of 2027, largely because power-connected sites, cooling systems, and land with grid access had become more valuable in a broader compute buildout. That shift is revealing. A mining site is no longer just a place where bitcoin is produced. It is increasingly a scarce infrastructure asset that can be repurposed for more lucrative workloads if the economics justify it.

The strategic implications are already visible. Core Scientific’s relationship with CoreWeave became an early signal that miners with the right power profile could be revalued through the lens of high-performance computing, and CoreWeave later agreed to acquire Core Scientific in a deal valued at about $9 billion to secure contracted and future power capacity for AI workloads. In Brazil, meanwhile, surplus renewable generation drew crypto miners precisely because underused energy had become an arbitrage opportunity. These developments point in the same direction. Mining is no longer an isolated crypto activity. It sits inside a wider contest over power, land, and compute capacity, where electricity itself increasingly functions as the prize asset.

That broader context matters because electricity demand from data centers, AI, and crypto mining is rising together. The International Energy Agency warned that consumption from those sectors could double by 2026, turning grid access into a strategic constraint rather than a background assumption. In that setting, Bitcoin mining begins to resemble a digital extractive industry folded into a larger infrastructure economy, one in which success depends not only on hashing efficiency but on control over scarce industrial inputs.

Regulation, Geography, and the Reality of Terrestrial Constraint

As soon as Bitcoin mining became a meaningful industrial load, terrestrial regulation became inevitable. Efforts by U.S. authorities to measure mining electricity use in 2024, even though the emergency survey was later halted, made the point clearly enough: policymakers no longer see mining simply as software or finance. They see it as an infrastructure issue touching grids, emissions, peak demand, and local power prices. By March 2026, officials were advancing pilot surveys for data centers after the mining-specific effort had been challenged, suggesting that the regulatory lens is widening from crypto alone to all large digital loads competing for electricity.

| Why Regulation and Geography Now Matter More | ||

|---|---|---|

| Policy or Location Factor | Why It Has Become Material | What It Means for the Industry |

| Electricity-use scrutiny | Mining is now large enough to affect grid planning and local demand debates | Policy attention shifts from crypto as finance toward crypto as industrial load |

| Emissions and power mix | Energy sourcing determines both operating cost and public-policy exposure | Location choices increasingly reflect energy-policy tradeoffs |

| Transmission bottlenecks | Some jurisdictions have surplus generation but insufficient transmission | Mining can monetize stranded or underused power in select regions |

| Cross-border mobility | Mining capacity can relocate relatively quickly compared with many heavy industries | Hash rate distribution increasingly follows cost and policy rather than ideology |

| Data-center policy spillover | Governments are broadening oversight to large digital loads beyond crypto alone | Mining is being normalized into wider infrastructure regulation |

| Sources: U.S. Energy Information Administration; Reuters; | ||

Geography follows the same industrial logic. After China’s 2021 crackdown, mining gravitated toward jurisdictions offering a combination of legal tolerance, abundant power, and manageable operating costs. The United States became the dominant center, but the pull of other energy-rich jurisdictions has grown as miners search for cheaper or underused supply. Brazil’s recent appeal rested not on ideology but on surplus renewable generation that could be monetized without worsening peak grid stress. That is how commodity production moves. It follows cost, access, and regulatory conditions.

For all the language about digital assets and decentralized finance, Bitcoin now sits squarely inside the same physical and political systems that shape terrestrial industries. Its network still runs on code, but the economics of securing it are governed by electricity markets, capital budgets, infrastructure bottlenecks, and public oversight. The result is not merely that Bitcoin is traded like a commodity. It is increasingly produced like one, and that shift marks the clearest end yet to the era that first made it feel culturally distinct from the rest of the economy.

Key Takeaways

- Grassroots mining has been displaced less by formal exclusion than by capital intensity, hardware turnover, and tighter return requirements.

- Bitcoin increasingly behaves like a virtual commodity because its production now depends on energy access, cost position, and industrial scale.

- Post-halving mining economics reward execution in power sourcing, fleet efficiency, and capital management more than simple price exposure.

- Power-connected mining sites are being revalued as broader infrastructure assets as AI and high-performance computing compete for the same inputs.

- Regulation and geography now shape Bitcoin mining in ways that resemble terrestrial commodity industries more than early crypto culture.

Sources

- Cambridge Centre for Alternative Finance; Cambridge Digital Mining Industry Report 2025; – Link

- Cambridge Centre for Alternative Finance; Cambridge Bitcoin Electricity Consumption Index; – Link

- CoinShares; Bitcoin Mining Report Q4 2025; – Link

- CoinShares; Bitcoin Mining Report Q1 2026; – Link

- International Energy Agency; Electricity 2024; – Link

- International Energy Agency; Energy and AI; – Link

- Reuters; AI’s Race for U.S. Energy Butts Up Against Bitcoin Mining; – Link

- Reuters; CoreWeave to Acquire Core Scientific in $9 Billion Deal; – Link

- Reuters; Clean Energy Glut Draws Cryptocurrency Miners to Brazil; – Link

- U.S. Energy Information Administration; Tracking Electricity Consumption from Cryptocurrency Mining; – Link

- World Gold Council; All-in Sustaining Costs and All-in Costs; – Link