{kind=link}

For more than a decade, blockchain’s public identity has been shaped by volatility. Bitcoin rallies, ETF inflows, and abrupt reversals continue to dominate coverage, reinforcing the perception of crypto as a macro-sensitive risk asset rather than structural financial infrastructure. In early 2026, U.S. spot Bitcoin exchange-traded funds recorded approximately $3.8 billion in cumulative outflows over five weeks, illustrating how quickly institutional capital repositions when liquidity tightens.

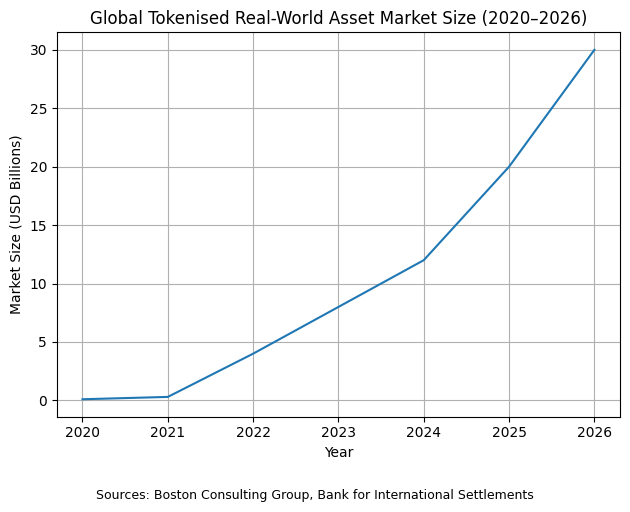

Beneath that price layer, however, a structural migration is underway. Distributed ledger systems are moving from speculative trading venues toward the operational core of regulated markets. The Institute of Internet Economics identifies 2025 as an inflection point marked by infrastructure consolidation, regulatory sorting, and a narrowing of crypto’s perimeter toward governable financial rails. The Bank for International Settlements, in turn, frames tokenisation as a modernization pathway capable of improving legacy settlement processes while enabling programmable capabilities across payments and securities markets.

In finance, a technology becomes standard not through narrative dominance but through workflow integration. Settlement friction declines, capital efficiency improves, compliance remains intact, and risk becomes more transparent. By these measures, blockchain’s trajectory is increasingly operational. Rather than constructing parallel ecosystems, banks and market infrastructures are embedding distributed ledger components into clearing, collateral management, fund administration, and trade documentation – areas still shaped by batch processing and reconciliation cycles designed for fragmented markets.

Tokenisation makes the shift tangible. When government bonds, money market fund shares, and private credit instruments are converted into programmable tokens, their economic substance remains unchanged; what evolves is the settlement logic. Ownership records synchronize automatically. Corporate actions execute through predefined code. IOSCO’s analysis underscores how these adjustments reshape post-trade mechanics and supervisory oversight without redefining the assets themselves.

Becoming standard therefore implies normalization within regulated architecture, not displacement of incumbent institutions. Retail trading cycles may continue to fluctuate with macro conditions. Infrastructure, by contrast, compounds through compliance alignment and measured systems integration. The speculative layer reacts to liquidity; the infrastructural layer reorganizes it.

Tokenisation Use Cases and Constraints

| Asset | Purpose | Operational gain | Constraint |

|---|---|---|---|

| Government bonds | Enable programmable settlement without changing credit risk. | Faster collateral reuse and ownership synchronization. | Clear settlement finality and custody rules. |

| Money market funds | Embed cash instruments into programmable workflows. | Improved intraday liquidity management. | Transfer-agent and valuation integration. |

| Private credit | Digitize servicing and ownership records. | Automated corporate actions and transparency. | Disclosure and cross-border enforceability. |

| Trade documents | Synchronize documentation across counterparties. | Reduced verification delays and faster payment. | Legal recognition and standards adoption. |

| Sources: IOSCO, World Trade Organization | |||

How the Infrastructure Stack Is Taking Shape

If blockchain is to function as infrastructure, it must change how financial state is recorded and transferred inside systems that already move capital at scale. A distributed ledger is a synchronized record in which each validated transaction is cryptographically linked to the previous one, forming an interlocking chain of state changes shared across authorized participants. Every entry preserves a traceable history of ownership and disposition, creating an auditable lineage of asset movement. Rather than maintaining separate books and reconciling discrepancies after execution, institutions reference a common ledger that updates simultaneously under defined validation rules. AI-driven monitoring increasingly oversees this environment, automating reconciliation, flagging anomalies, and compressing exception cycles. Efficiency follows from structure: fewer duplicative records, faster visibility into settlement status, and security reinforced by distributed validation that makes unilateral alteration operationally prohibitive.

Blockchain Infrastructure in Regulated Finance

| Layer | Core function | Example | Governance focus |

|---|---|---|---|

| Post-trade utilities | Shared ledger reduces reconciliation and settlement timing gaps. | DTCC Project Ion | Settlement finality and operational resilience |

| Tokenised bank liabilities | On-chain bank money coordinates delivery versus payment. | J.P. Morgan Kinexys and JPM Coin | Prudential treatment and liquidity oversight |

| Supervised pilot layer | Regulated environments test tokenised bonds and funds. | MAS Project Guardian | Licensing, custody, and reporting controls |

| Interoperability layer | Messaging connects tokenised platforms to existing networks. | SWIFT digital asset trials | Standards and cross-border compliance alignment |

| Sources: DTCC, SWIFT, Monetary Authority of Singapore, J.P. Morgan | |||

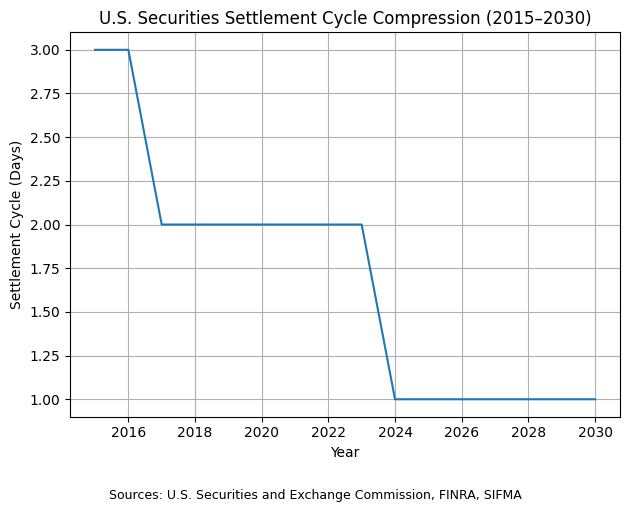

These mechanics are being tested within core market utilities. DTCC, which processes transactions valued at more than $2 quadrillion annually, advanced Project Ion after demonstrating that distributed ledger settlement models could operate alongside legacy systems. The U.S. transition to T+1 settlement in 2024, shortening the cycle from two business days to one, intensified the need for synchronized confirmation and asset availability. Shared ledger architecture reduces timing mismatches, supporting further compression toward near real-time execution without dismantling existing clearing frameworks.

The money layer addresses delivery-versus-payment risk. J.P. Morgan’s Kinexys platform, including JPM Coin, has processed more than $300 billion in cumulative transaction volume and supports billions in daily institutional flows. By moving digital representations of bank liabilities on-chain, tokenised assets and programmable deposits settle as coordinated ledger updates. Narrowing the temporal gap between asset transfer and payment execution reduces counterparty exposure and accelerates collateral redeployment.

Regulatory pilots clarify operational feasibility. The Monetary Authority of Singapore’s Project Guardian convenes global institutions to test tokenised bonds, funds, and foreign exchange within supervised parameters in a financial center overseeing assets exceeding S$4 trillion. Permissioned participation and embedded reporting logic align tokenised transactions with licensing and custody requirements from inception.

Trade finance illustrates the applied dimension. With global trade volumes exceeding $25 trillion annually, documentation latency constrains liquidity across supply chains. Platforms such as WaveBL, implemented with Lloyds, digitize and synchronize document state across counterparties, reducing manual verification steps and accelerating payment release. Across multi-trillion-dollar trade flows, incremental cycle reductions translate into measurable working capital gains.

Interoperability determines scalability. SWIFT connects more than 11,000 institutions across over 200 countries and territories, transmitting tens of millions of financial messages daily. Its digital asset trials seek to integrate tokenised platforms into existing global messaging rails, preventing liquidity fragmentation while embedding distributed ledger components within established networks.

Across layers, the gains are structural: synchronized records reduce reconciliation, programmable execution compresses settlement windows, embedded AI oversight strengthens compliance, and distributed validation enhances resilience. Blockchain’s relevance lies not in token issuance but in re-engineering how financial state moves across systems measured in trillions – and in post-trade utilities, quadrillions – of dollars annually.

Future Market Structure and Governance Requirements

As distributed ledger systems shift from pilot corridors into regulated production, the focus moves from proof of concept to systemic calibration. When infrastructure measured in trillions accelerates, governance becomes an economic variable.

The additive benefits to traditional banking and investment systems are measurable. Global outstanding debt securities exceed $140 trillion, and cross-border portfolio investments account for tens of trillions more. Even marginal reductions in settlement latency and reconciliation overhead release significant capital. The U.S. move from T+2 to T+1 in 2024 shortened exposure windows and reduced margin requirements. Synchronizing asset and cash states through distributed ledgers extends that compression, potentially lowering collateral buffers tied to settlement risk and improving balance sheet flexibility under Basel III liquidity and capital standards.

Time compression, however, alters market dynamics. Settlement buffers historically allowed liquidity sourcing and supervisory oversight. As programmable execution narrows those intervals, capital can reposition across interconnected networks with greater velocity. In stable conditions, exposure declines. Under stress, repricing and liquidity migration may accelerate.

Stable-value instruments heighten the tension. Tokenised representations of bank deposits and short-term sovereign-backed assets are increasingly embedded in settlement flows, while global stablecoin market capitalization has fluctuated in the hundreds of billions of dollars range. As these instruments intersect with regulated tokenised securities markets, confidence becomes infrastructural. A reserve impairment or operational outage could transmit liquidity effects rapidly across synchronized systems. Research from the Cambridge Centre for Alternative Finance emphasizes that interoperability standards and regulatory clarity are critical to preventing fragmentation and contagion in tokenised money environments.

Regulatory architecture will determine adoption velocity. The European Union’s Markets in Crypto-Assets framework imposes authorization, reserve, and disclosure requirements on issuers and service providers, aligning digital asset activity with financial stability principles. Similar supervisory tightening is unfolding across major jurisdictions, particularly where tokenised funds, deposits, and wholesale payment systems converge. Divergence in custody law and settlement finality definitions nonetheless creates cross-border friction.

Over the next 18 to 24 months, implementation is likely to concentrate in wholesale domains – interbank payments, tokenised money market funds, collateral mobility platforms, and regulated bond issuance. Governance priorities will focus on interoperability standards, clear legal definitions of digital asset ownership and segregation, institutional-grade smart-contract audits, and supervisory tools capable of near real-time monitoring. AI-assisted compliance systems are positioned to expand toward predictive anomaly detection as transaction volumes scale.

Blockchain’s integration is therefore additive rather than revolutionary. Synchronized ledgers reduce reconciliation costs and compress settlement exposure across markets valued in the tens of trillions. Yet accelerated capital mobility can magnify imbalances if oversight does not calibrate to structural speed. Whether distributed ledger infrastructure strengthens systemic resilience will depend less on technological capability than on the discipline of its governance.

Governance Snapshot for Tokenised Markets

| Jurisdiction | Framework | Scope | Implication |

|---|---|---|---|

| European Union | MiCA | Authorization and reserve requirements. | Clearer compliance perimeter for issuers. |

| Singapore | Project Guardian | Supervised tokenisation pilots. | Regulated corridor for production testing. |

| United States | T+1 settlement reform | Shortened securities settlement cycle. | Operational pressure for synchronized systems. |

| Sources: European Securities and Markets Authority, Monetary Authority of Singapore, U.S. Securities and Exchange Commission, FINRA | |||

Key Takeaways

• Blockchain adoption is shifting from speculative trading cycles toward regulated infrastructure integration across clearing, settlement, custody, and collateral management.

• A distributed ledger improves efficiency by synchronizing transaction records, reducing reconciliation, and compressing exposure windows through programmable settlement.

• Institutional deployment is occurring at systemic scale, within markets that process over $2 quadrillion annually and encompass more than $140 trillion in outstanding global debt.

• Tokenised bank liabilities and synchronized settlement models reduce delivery-versus-payment risk and improve capital efficiency under existing liquidity and capital standards.

• Efficiency gains are accompanied by structural tradeoffs, including accelerated capital mobility that may amplify liquidity stress if not properly governed.

• Interoperability standards, custody clarity, smart-contract audit controls, and near real-time supervisory monitoring will determine the ceiling of adoption.

• Over the next 18 to 24 months, blockchain implementation is likely to expand additively within wholesale financial corridors rather than displace traditional banking institutions.

Sources

• Institute of Internet Economics; The State of Crypto & Blockchain 2025 YE Review; – Link

• Institute of Internet Economics; How Blockchain Is Rewiring Trade, Collateral and Settlement; – Link

• Institute of Internet Economics; AI Becomes the Compliance Engine of Crypto; – Link

• Bank for International Settlements; Annual Economic Report 2025 – Tokenisation Chapter; – Link

• International Organization of Securities Commissions; Tokenisation and Market Implications; – Link

• International Monetary Fund; Tokenised Reserves and Monetary Implications; – Link

• Cambridge Centre for Alternative Finance; Tokenised Money Use Cases Interoperability and Regulation; – Link

• DTCC; Project Ion Development Phase Announcement; – Link

• J.P. Morgan; Kinexys / JPM Coin Digital Payments Overview; – Link

• Monetary Authority of Singapore; Project Guardian; – Link

• SWIFT; Live Digital Asset Transaction Trials; – Link

• World Trade Organization; World Trade Statistical Review; – Link

• Securities Industry and Financial Markets Association; US Transition to T+1 Settlement; – Link

• U.S. Securities and Exchange Commission; SEC Adopts T+1 Settlement Cycle Rules; – Link

• FINRA; Understanding Settlement Cycles; – Link

• CoinDesk; Bitcoin ETFs Record $3.8 Billion Five-Week Outflow; – Link

• European Securities and Markets Authority; Markets in Crypto-Assets Regulation (MiCA); – Link