{kind=link}

Industrial robotics is moving out of a startup-driven expansion phase and into a period defined by industrial discipline and financial accountability. Throughout the 2010s, robotics development was shaped by venture-backed experimentation, with firms prioritizing proof of concept and speed to deployment over lifecycle durability or capital efficiency. That model produced genuine technical progress, but it also generated systems that often struggled when exposed to continuous industrial operation.

The scale of adoption illustrates both the success and the limits of this approach. Global industrial robot installations exceeded 553,000 units in 2022, with automotive manufacturing accounting for roughly 40 percent of demand, according to industry data. Logistics and warehousing followed as fast-growing segments, driven by e-commerce expansion and persistent labor shortages. As robotics moved from pilots into core operations, however, buyers increasingly evaluated systems using the same capital standards applied to conventional industrial equipment.

This transition marks a structural shift. Robotics is no longer treated as experimental infrastructure but as depreciating industrial assets expected to meet defined payback periods, utilization targets, and serviceability requirements. The industry’s current reset reflects the growing separation between technologies that can scale economically and those that remain viable only under subsidized or experimental conditions.

When Robotics Technology Outpaces Economic Reality

Modern industrial robotics encompasses articulated arms for welding and assembly, collaborative robots designed to work alongside humans, and autonomous mobile robots responsible for material movement and order fulfillment. Advances in machine vision, sensor fusion, and AI-based control have expanded automation into tasks once considered too variable for machines.

In tightly controlled environments, these technologies deliver clear value. In automotive manufacturing, robotic welding and painting systems continue to achieve strong returns due to standardized processes and predictable operating conditions. Economic challenges emerge when similar technologies are extended into less structured environments, such as mixed-model assembly or final-fit operations. Here, vision systems must adapt continuously to design variation and tolerance changes, increasing calibration requirements and reducing uptime.

Logistics operations highlight these limitations even more sharply. Autonomous mobile robots depend on simultaneous localization and mapping, fleet orchestration software, and real-time path planning to move goods efficiently. While effective in low-density, static layouts, performance degrades as traffic increases, layouts change, or human workers interact unpredictably. Minor navigation errors or congestion can cascade across fleets, reducing throughput and increasing exception handling.

Integration further undermines economic performance. In large fulfillment centers, robotics platforms must interface with warehouse management systems, order orchestration software, and legacy conveyor infrastructure. Integration and commissioning frequently account for 30 to 50 percent of total automation project costs in complex logistics environments. These costs are rarely visible in early demonstrations, but they materially distort ROI assumptions once systems are deployed at scale.

Hardware design decisions made during the startup phase compound these challenges. Many platforms emphasize tightly integrated architectures and custom components to accelerate time to market. In industrial environments, this increases mean time to repair, inflates spare-parts inventories, and limits redeployability. Once robotics systems are capitalized over multi-year lifecycles, these characteristics become incompatible with standard asset management expectations.

Why ROI and Cost Structures Now Dictate Robotics Design

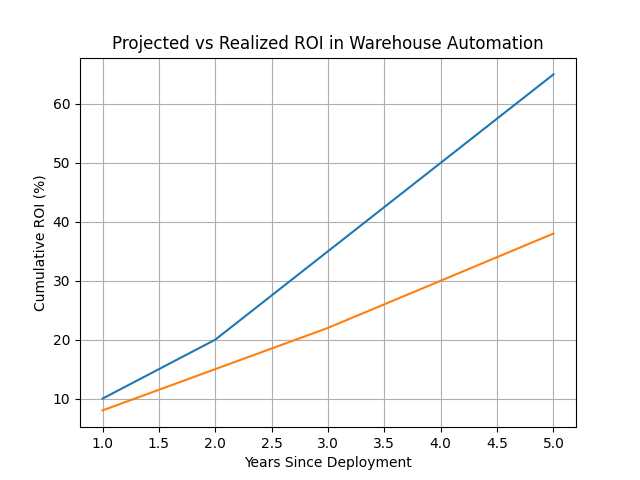

As robotics investments fall under tighter financial scrutiny, ROI and cost structures increasingly dictate technology choices. Most manufacturers and logistics operators target payback periods of three to five years, with predictable operating costs and stable utilization. Systems that require prolonged commissioning or deliver volatile performance struggle to meet these thresholds.

Industry data reinforces this shift. Surveys across warehousing and manufacturing consistently show that fewer than half of large-scale automation projects achieve their initially projected ROI within three years. Even modest deviations in uptime can materially alter payback timelines, particularly when automation replaces flexible human labor rather than fixed machinery.

Labor economics further constrain adoption. In U.S. fulfillment operations, fully loaded warehouse labor costs typically range from $45,000 to $60,000 per worker annually. Robotics systems that require frequent maintenance, specialized supervision, or extensive exception handling often fail to deliver sustained cost advantages once depreciation, service contracts, and downtime are fully accounted for.

Depreciation dynamics also shape design priorities. Traditional industrial equipment depreciates predictably over seven to ten years, enabling structured capital planning. Robotics systems that require major hardware replacement or become obsolete due to software incompatibility disrupt this model. Buyers increasingly favor modular designs and software-defined upgrades that extend asset life and preserve residual value.

These financial realities are constraining the scope of acceptable innovation. Advanced autonomy remains attractive, but only when paired with predictable economics, transparent lifecycle costs, and demonstrable operating histories.

Industrial Robotics Technologies by Use Case and Economic Reliability

| Technology Type | Primary Use Case | Core Strength | Economic Failure Point | ROI Reliability |

|---|---|---|---|---|

| Articulated Robotic Arms | Welding, painting, fixed assembly | High precision and repeatability | Low adaptability to product variation | High |

| Collaborative Robots (Cobots) | Human-assisted assembly, inspection | Lower safety enclosure costs | Limited speed and payload | Medium |

| Autonomous Mobile Robots (AMRs) | Warehouse transport, fulfillment | Layout flexibility and scalability | Traffic congestion, uptime variability | Medium–Low |

| Vision-Guided Picking Systems | Piece picking, sorting | High task flexibility | Model drift and retraining costs | Low–Medium |

| Automated Storage and Retrieval Systems | High-density warehousing | Throughput and space efficiency | High capital intensity, low flexibility | Medium |

Source: International Federation of Robotics; McKinsey & Company; Industry analyses

The New Centers of Gravity in Industrial Robotics Technology

The convergence of technical and financial pressures is reshaping the industry’s technological center of gravity. Emphasis is shifting away from bespoke, vertically integrated systems toward modular, interoperable architectures aligned with industrial economics.

Modularity enables incremental deployment and redeployment, reducing capital risk and improving utilization. Industry surveys indicate that a growing majority of logistics operators now prioritize interoperability and open interfaces when evaluating automation vendors. This shift favors platforms that integrate with heterogeneous infrastructure rather than replace it.

Software has become equally decisive. Digital twins and simulation tools are increasingly used to model robotic workflows before physical deployment. In automotive manufacturing, simulated commissioning allows robotic cells to be optimized for cycle time and collision risk prior to installation. Simulation-led approaches have been shown to reduce commissioning time by as much as 30 percent, improving forecast accuracy and reducing downside risk.

Safety, cybersecurity, and regulatory compliance are now embedded design requirements rather than secondary considerations. Fire risks associated with lithium-ion batteries have increased insurance scrutiny, while connected robotics systems face expanding cybersecurity obligations. European regulatory frameworks governing AI and industrial safety are accelerating demand for auditability and lifecycle controls, influencing product design globally.

These requirements favor vendors with scale, mature service networks, and regulatory expertise, reinforcing consolidation across the sector.

What the Shift Means for Buyers and Capital Allocation

For buyers, robotics adoption has become a capital allocation decision rather than a technology bet. Automation investments are evaluated alongside conventional machinery, facility upgrades, and labor strategies, with increasing emphasis on balance-sheet impact and cash-flow stability.

Large fulfillment operators illustrate this shift. Rather than relying on generic robotics platforms, leading firms have moved toward tightly controlled, internally optimized systems designed around specific workflows. This reflects a recognition that generalized robotics solutions often struggle to deliver consistent ROI at scale.

Regional dynamics intensify these considerations. Asia, particularly China, Japan, and South Korea, accounts for more than 70 percent of global industrial robot installations. Many manufacturers in these markets adopted automation aggressively during periods of rapid growth, scaling early-generation systems. As margins tighten, underperforming assets are being reassessed, exposing long-term cost and upgrade limitations.

The United States faces a different constraint profile. Robotics adoption has been more selective, but integration costs are higher due to heterogeneous facilities and legacy IT systems. When systems underperform, remediation costs are often higher than in greenfield Asian environments. Cybersecurity and regulatory exposure further increase total cost of ownership.

Europe’s stricter regulatory environment raises upfront compliance costs but reduces long-term operational risk, accelerating the rejection of immature systems and encouraging earlier convergence toward standardized designs.

Across regions, buyers increasingly favor phased deployments tied to proven performance, limiting exposure to ROI shortfalls and stranded assets.

Regional Industrial Robotics Deployment Profiles and Risk Factors

| Region | Deployment Intensity | Typical Facility Profile | Primary Financial Risk | Regulatory / Structural Pressure |

|---|---|---|---|---|

| Asia | Very High | Large-scale manufacturing, export-oriented | Asset saturation and margin compression | Lower regulation, higher capital exposure |

| United States | Medium | Mixed-age facilities, heterogeneous IT | High integration and retrofit costs | Cybersecurity and labor regulation |

| Europe | Medium–High | High-value manufacturing | Upfront compliance and certification cost | Strict safety and AI governance |

Source: International Federation of Robotics; OECD; World Bank

Outlook for Industrial Robotics in a Capital Disciplined Era

Automation remains a structural necessity driven by labor shortages, demographic pressures, and productivity demands. The constraint is not technological potential, but economic survivability.

The next phase of industrial robotics will favor technologies that deliver consistent uptime, predictable costs, and long asset lives. Incremental improvements in perception, control, and simulation will matter more than headline breakthroughs if they improve utilization and reduce maintenance.

Likely winners include modular robotics platforms, software-driven orchestration systems, and vendors capable of supporting global service and compliance requirements. Losers will be highly customized, capital-intensive systems that depend on optimistic utilization assumptions or fragile operating models.

Industrial robotics is not slowing down. It is converging toward durable, economically viable automation, marking its transition from experimentation to industrial infrastructure.

Future Uses and Emerging Technologies in Industrial Robotics

| Future Use Case | Enabling Technology | Timeline |

|---|---|---|

| Flexible final assembly | Advanced vision, force sensing, AI motion planning | Medium term |

| Autonomous intra-factory logistics | Fleet-level orchestration, edge AI | Short–Medium term |

| Mixed human–robot work cells | Safety-rated AI, real-time perception | Medium term |

| Simulation-first deployment | Digital twins, virtual commissioning | Short term |

| Self-optimizing production lines | Reinforcement learning, real-time analytics | Medium–Long term |

| Distributed micro-factories | Modular robotics, cloud coordination | Long term |

| Predictive maintenance automation | Sensor fusion, anomaly detection | Short term |

| Compliance-by-design robotics | Audit logging, explainable AI | Medium term |

| AI-driven quality inspection | Computer vision, edge inference | Short–Medium term |

| Energy-aware automation | Power-optimized hardware, AI scheduling | Medium term |

Source: International Federation of Robotics; OECD; McKinsey & Company; Industry analyses

Key Takeaways

- Industrial robotics is transitioning from startup-led experimentation to capital-disciplined maturity.

- Core technologies function as intended, but economic fragility emerges at scale.

- ROI, depreciation, and serviceability now shape robotics design and deployment.

- Regional differences amplify financial and operational constraints.

- The industry’s future lies in robust, modular, financially viable systems.

Sources

- International Federation of Robotics; World Robotics 2023 – Industrial Robots; – Link

- McKinsey & Company; Automation in Logistics and Manufacturing: The Economic Reality; – Link

- Boston Consulting Group; How Robots Will Transform Manufacturing and Logistics; – Link

- Siemens; Digital Twins in Industrial Automation; – Link

- Organisation for Economic Co-operation and Development; The Impact of Industrial Robots on Productivity and Jobs; – Link

- U.S. Bureau of Labor Statistics; Employer Costs for Employee Compensation; – Link

- PitchBook; Robotics & Automation Industry Report; – Link