{kind=link}

Connectivity has quietly shifted from a purchased service to a background condition of modern life. More than 4.6 billion people use mobile internet globally, and smartphone users exceed 4.3 billion, making mobile the dominant interface to digital life according to GSMA data. At national scale, operators such as Verizon, China Mobile, and Vodafone manage traffic volumes that increasingly resemble utility throughput rather than consumer media demand.

The coverage footprint now looks like a baseline layer of economic participation. ITU reporting confirms that 4G networks cover more than 95 percent of the population in advanced economies, while 5G reaches over half the global population. The engineering is complex, but the user experience is blunt: when the signal is there, people move money, coordinate work, and reach services without thinking; when it disappears, the economy briefly loses its operating system.

The economic scale explains why expectations are hardening. Mobile technologies generated approximately $5.7 trillion in global economic value in 2023, equivalent to 5.4 percent of global GDP. Telecommunications capital expenditure reached roughly $295 billion that year, with projected cumulative investment of $1.5 trillion between 2023 and 2030. Operators such as AT&T and Deutsche Telekom are investing heavily in network virtualization and core redundancy because demand is no longer about faster browsing. It is about continuous access to cloud platforms, payment processors, and customer-facing systems that assume the network is always on.

| Global Connectivity Dependence Across Critical Functions | |||

| Sector | Connectivity Role | Failure Impact | Policy Relevance |

|---|---|---|---|

| Digital Payments | Real-time authorization and transaction routing | Retail and enterprise revenue disruption | Systemic risk oversight and outage reporting mandates |

| Emergency Services | Dispatch coordination and public alerts | Public safety exposure | Critical infrastructure classification |

| Cloud Enterprise Systems | Continuous SaaS and ERP access | Operational downtime and productivity loss | Resilience compliance requirements |

| Sources: GSMA Intelligence; OECD; World Bank | |||

That assumption is now embedded in productivity and growth logic. World Bank research indicates that a 10 percent increase in broadband penetration can increase GDP growth by up to 1.38 percentage points in developing economies. OECD digital economy analysis consistently frames connectivity as a multiplier because it expands participation, accelerates transactions, and reduces coordination costs. Global digital payment transaction value exceeds $14 trillion annually, much of it routed through mobile-connected systems such as Visa, Mastercard, and Alipay networks. For a small retailer running payments through a point-of-sale terminal, connectivity is not a nice-to-have line item. It is operational oxygen.

Outages make the utility reality visible by showing how widely the costs spread. In July 2022, a nationwide Rogers outage affected approximately 12 million subscribers, halting Interac debit transactions and disrupting emergency services across Canada; public-sector estimates placed economic losses at roughly CAD $142 million for the day. Australia’s Optus outage affected nearly 10 million users and prompted federal review due to its impact on hospitals, banking access, and transport systems. The losses do not respect customer boundaries, because payments, authentication, logistics, and communications chains run across providers and sectors.

For years, the policy stance matched an earlier internet era. Competition and spectrum policy were the primary governance tools, with switching and market pressure expected to discipline service quality. Regulators focused on allocation and interconnection while resilience was treated as engineering practice, not a public requirement. That posture made sense when disruption was local and the economic blast radius was limited.

Dependency now behaves like shared national exposure. Financial clearing, enterprise workflows, emergency dispatch coordination, and public administration platforms assume continuous connectivity, and switching providers does little during systemic failure. Market incentives still matter, but they struggle to internalize national GDP exposure when harm is distributed across firms, consumers, and public services. As telecommunications integrates with power grids and hyperscale cloud providers, cascades become more plausible. The core shift is not that connectivity became popular. It is that it became foundational.

Market Incentives, Governance, and the Emerging Regulatory Moment

Regulation is tightening around connectivity for a simple reason: the failure mode now looks like infrastructure failure. When networks go down, people lose banking access, telehealth appointments, workplace systems, and emergency communications in the same hour. In the United States, more than 85 percent of adults rely on smartphones for daily online access, and during major outages, 911 services and digital government portals have experienced disruption. Network reliability has moved from a carrier promise to a public expectation.

The economics behind intervention are not abstract. During the Rogers outage, approximately one-quarter of Canadian connectivity was impaired, disrupting Interac payments nationwide. Enterprises that were not direct customers still experienced transaction failure, revealing why firm-level accountability does not map cleanly onto economy-wide harm. When digital payment flows measure in the trillions annually, the outage cost is not limited to churn, refunds, or reputation damage. It becomes a friction shock to commerce, payroll, and basic household purchasing.

| Major Telecom Outages and Regulatory Response | |||

| Country | Operator | Primary Disruption | Policy Outcome |

|---|---|---|---|

| Canada | Rogers | National payment and emergency disruption | Federal resilience review |

| Australia | Optus | Hospital, banking, and transport disruption | Government investigation and compliance review |

| Sources: Reuters; ABC News Australia; Toronto City Council | |||

Policy is responding by shifting from general oversight to enforceable resilience behavior. In the United States, the FCC’s Disaster Information Reporting System integrates telecommunications outage data into federal emergency management processes, effectively treating outages as national coordination events rather than private service incidents. In Europe, the NIS2 Directive requires initial incident notification within 24 hours and follow-up assessment within 72 hours, with penalties reaching €10 million or 2 percent of global turnover. Resilience is moving from operational preference into statutory compliance, with obligations that can be audited and penalized.

Operators are adapting because resilience is turning into a measurable governance outcome. Carriers such as BT, Telefónica, and T-Mobile are expanding network automation, geo-diverse routing, and rollback controls to reduce systemic exposure. In parallel, hyperscale cloud providers hosting 5G core functions are embedding compliance and audit capabilities directly into network architecture. Reliability is increasingly expressed through controls, logging, and repeatable recovery playbooks that regulators and enterprise customers can scrutinize, rather than through marketing claims about coverage.

Supply chain governance is now inseparable from resilience because the network is an ecosystem of vendors, software layers, and remote management pathways. The European Commission’s ICT Supply Chain Security Toolbox formalizes risk mitigation across supplier networks, and debates over 5G equipment participation and high-risk vendor designations show how infrastructure sourcing intersects with foreign policy. As networks virtualize, questions about remote management access, firmware integrity, and update provenance become operational resilience issues with direct business implications. Telecommunications regulation now touches semiconductor constraints, hyperscale dependencies, and cross-border technology policy.

The same pressures land differently across income tiers. High-income economies can finance redundancy mandates and auditing frameworks while maintaining rollout momentum. Middle-income markets face sharper trade-offs between rapid 5G expansion and compliance burden. In Sub-Saharan Africa, mobile money platforms such as M-Pesa serve millions as a primary banking interface; outages carry immediate social consequence even where measured GDP share is smaller. Oversight is becoming institutionalized economic governance, but sequencing is not uniform, and the inclusion agenda does not pause while resilience standards rise.

Connectivity, Digital Sovereignty, and the Rise of Virtual Nations

Connectivity governance is now colliding with sovereignty governance because the network carries the operational core of modern economies. Telecommunications networks underpin economic output, industrial strategy, and national security at the same time, and that convergence is reshaping what regulation is meant to do. Vendor trust regimes, localization requirements, and cybersecurity standards increasingly define digitally bounded ecosystems where participation depends on compliance with technical and governance constraints. Virtual nationhood is emerging through infrastructure regulation that sets the rules for trusted connectivity.

| Digital Sovereignty Levers in Telecom Governance | |||

| Policy Lever | Objective | Implementation | Economic Effect |

|---|---|---|---|

| Vendor Risk Controls | Limit strategic exposure | Procurement restrictions | Supplier substitution and capex shifts |

| Localization Mandates | Jurisdictional control | Domestic hosting requirements | Cloud architecture redesign |

| Sources: European Commission; ENISA; Ofcom | |||

Data is increasingly treated as national economic capital, yet data does not move or compute without the network layer that carries it. Governments are investing heavily in domestic data center expansion and semiconductor capacity to secure processing autonomy, and telecommunications networks form the backbone of that capacity. The global semiconductor market exceeds $500 billion annually, and AI compute infrastructure investment measures in the tens of billions across major economies. As 5G cores virtualize and workloads shift into cloud environments, the economic value tied to connectivity sits inside an ecosystem of compute, storage, and silicon that governments are increasingly motivated to secure.

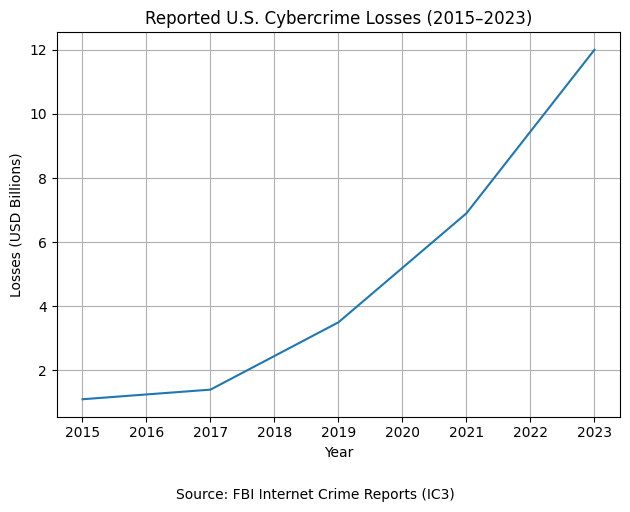

Cybersecurity adds urgency and turns dependence into a measurable risk profile. U.S. cybercrime losses exceeded $12 billion in 2023 alone. Ransomware attacks on hospitals and municipalities have forced service diversion and shutdowns, turning digital disruption into physical-world consequence. Under those conditions, resilience is not only about uptime. It is also about reducing the attack surface of systems that rely on continuous connectivity for payment, dispatch, and public administration.

The regulatory direction points toward more formal resilience discipline. Standardized outage classifications, structured stress testing, and executive accountability provisions are plausible next steps, especially where outages are already treated as national incidents. Compliance metrics may influence licensing, spectrum allocation, and merger approvals, making resilience readiness a form of market access currency. The tighter the dependency, the tighter the link between performance and permission.

Supply chain scrutiny is likely to intensify because sovereignty is enforced through controllable components. Firmware verification, remote management transparency, and localization of critical control functions are emerging as standard risk levers. Cross-border hosting of virtualized cores may face national security review where lawful access regimes and vendor obligations diverge. Infrastructure certification may become a prerequisite for participation in national digital markets, extending compliance beyond operators to cloud hosts and equipment suppliers.

Capital allocation is already bending toward sovereignty priorities. Governments may deploy funding mechanisms to support redundant backbone infrastructure and domestic semiconductor manufacturing, and telecommunications resilience will intersect more directly with AI strategy and industrial competitiveness initiatives. Geopolitical segmentation is sharpening as export controls on advanced networking hardware and AI accelerators influence infrastructure design decisions, and digital trust blocs may consolidate around aligned vendor ecosystems.

Connectivity regulation is evolving into the legal architecture of digital state capacity. As data becomes economic capital and processing capacity becomes strategic strength, control over the infrastructure that carries and secures digital activity becomes a sovereignty function. Virtual nations emerge through enforceable regulatory design that defines trust boundaries, vendor eligibility, and infrastructure control.

Connectivity now operates as regulated continuity. The first driver is economic: when payments, enterprise workflows, and public administration assume always-on access, outages produce spillover losses that competition and switching cannot contain. The second driver is operational: regulators are translating resilience into enforceable obligations through reporting timelines, auditability, and continuity discipline that push networks toward utility-grade reliability expectations. The third driver is strategic: supply-chain assurance and hosting constraints increasingly determine which architectures and vendors are trusted, turning compliance into a condition of market participation. The result is a governance layer that not only supervises telecom markets, but increasingly defines the boundaries of digital economic membership.

Key Takeaways

- Connectivity has transitioned from competitive service to utility-grade infrastructure underpinning trillions in global economic value and daily economic coordination.

- Market competition cannot fully internalize systemic risk when outages affect millions and create measurable spillover losses across payments and services.

- Regulatory frameworks are converging around transparency, operational resilience mandates, and enforceable incident reporting timelines rather than content regulation.

- Reliability is becoming auditable governance performance as networks virtualize and recovery discipline is embedded into architecture and operations.

- Supply chain assurance is now central to resilience, linking telecom oversight to vendor ecosystems, firmware integrity, and cross-border dependencies.

- Economic tier shapes regulatory sequencing, with inclusion and affordability pressures constraining how quickly resilience mandates can be absorbed.

- Telecommunications oversight increasingly intersects with semiconductor constraints, AI compute strategy, and foreign policy alignment through vendor trust regimes.

- Virtual nations are emerging through regulatory design that defines digital trust boundaries and infrastructure control as a condition of participation.

- Near-term regulation is likely to tighten outage classification, stress testing expectations, and executive accountability tied to licensing and spectrum policy.

- Connectivity oversight is becoming institutional economic governance as network continuity translates into productivity, public safety, and national capacity.

Sources

- GSMA Intelligence; The Mobile Economy 2024; – Link

- GSMA Intelligence; The State of Mobile Internet Connectivity 2024; – Link

- International Telecommunication Union; Global Connectivity Report 2025; – Link

- World Bank; Broadband and Economic Growth Research; – Link

- OECD; Digital Economy Outlook; – Link

- Reuters; Rogers Communications Services Down for Thousands of Users; – Link

- Toronto City Council; Rogers Outage Economic Impact Estimate; – Link

- ABC News Australia; Optus Network Outage Report; – Link

- Federal Communications Commission; Disaster Information Reporting System; – Link

- Federal Communications Commission; Outage Information Sharing; – Link

- European Union; Directive (EU) 2022/2555 (NIS2 Directive) Article 23; – Link

- European Union Agency for Cybersecurity; Mapping NIS2 Obligations with ECSF Role Profiles; – Link

- European Commission; EU Launches New Toolbox to Strengthen ICT Supply Chain Security; – Link

- European Commission; Toolbox to Improve ICT Supply Chain Security; – Link

- Ofcom; Network and Service Resilience Guidance; – Link

- Ofcom; Network and Service Resilience Guidance for Communication Providers (PDF); – Link

- Federal Bureau of Investigation; Internet Crime Report 2023; – Link