{kind=link}

Internet connectivity is becoming embedded in society, daily life, and country-level economic interest. Mobile phones have helped connect a majority of the world’s population, turning basic access into a practical layer for finance, information, health access, work participation, and communication.

At the personal level, connectivity now creates a de facto standard for traditional banking and fintech access. It expands information access, supports entrepreneurial growth, improves public understanding of general health issues, extends digital health access, supports gig economy participation, and gives non-traditional banking a direct channel for moving money faster while reducing barriers to formal financial access.

Basic functions such as GPS now support property ownership because mobile phones can help locate, recognize, and document assets that were previously difficult to place inside formal systems. Digital communication has made constant contact a normal condition of personal and economic life. For businesses, the internet has been a de facto operating standard for nearly a decade, and improved services are unlocking artificial intelligence, stronger commerce, better supply-chain coordination, cloud-based analysis, and more transparent market participation.

At the country level, connectivity is becoming a baseline standard. Blackouts create economic losses, and the transmission of data has reached near-utility status. Beyond connectivity itself, government and business services now depend on digital access to improve lives and reduce structural barriers to a more stable humanitarian standard of existence.

ICT and mobile connectivity now form one of the largest operating layers of the internet economy. Global internet use reached about 6 billion people in 2025, while the offline population remained near 2.2 billion. Mobile broadband reached 99 subscriptions per 100 inhabitants and accounted for 89% of all mobile subscriptions. By April 2026, global internet use reached 6.12 billion people, while close to 2.2 billion people remained offline.

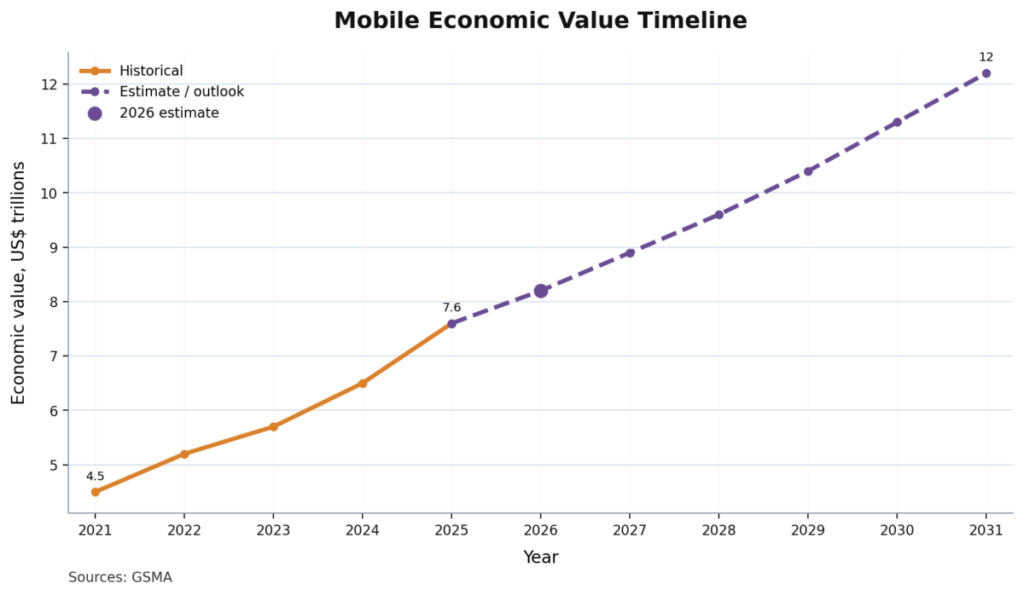

Mobile infrastructure also carries a large economic footprint. Mobile technologies and services generated about $7.6 trillion for the global economy in 2025, equal to 6.4% of global GDP. The industry supported 8.8 billion wireless connections and about 5.8 billion unique subscribers. By April 2026, unique mobile users reached 5.83 billion, equal to 70.4% of the global population, after adding 103 million users over the prior twelve months.

Connectivity has become less visible as it has become more essential. When networks fail, payment settlement slows, public services lose capacity, businesses pause activity, and digitally dependent households lose access to services that increasingly assume a working connection. The industry’s importance is therefore measured by continuity and practical usability, not only by coverage or subscription counts.

Key takeaway: Mobile broadband reached 99 subscriptions per 100 inhabitants in 2025.

Key takeaway: ICT and mobile connectivity have moved from access infrastructure into operating infrastructure for economic activity, public systems, and daily participation.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Global internet users | 6.00B | 6.18B | 3.0% | ITU; DataReportal |

| Offline population | 2.20B | 2.10B | -4.5% | ITU; DataReportal |

| Unique mobile users | 5.78B | 5.88B | 1.7% | DataReportal |

| Mobile economic value | $7.6T | $8.2T | 7.9% | GSMA |

* Estimate

New Trends

The most important 2026 trend is the expansion of mobile networks beyond communications into programmable infrastructure. 5G and early 5G-Advanced systems are increasingly tied to edge computing, network APIs, distributed cloud nodes, and on-device artificial intelligence. The mobile network is becoming a performance layer for local processing, industrial monitoring, and device-level intelligence.

Demand is also shifting from consumer mobile usage toward industrial and institutional load. Connected production and machine communication are adding pressure to mobile capacity as public infrastructure becomes more dependent on real-time network performance. These uses require predictable latency, strong uplink capacity, dense backhaul, and sufficient mid-band spectrum.

Satellite connectivity has become a more visible part of the connectivity stack. Its near-term importance lies in stabilizing access where terrestrial deployment economics remain weak. Satellite-supported backhaul and direct-to-device services can create a basic connectivity floor for areas that remain difficult to serve with conventional networks.

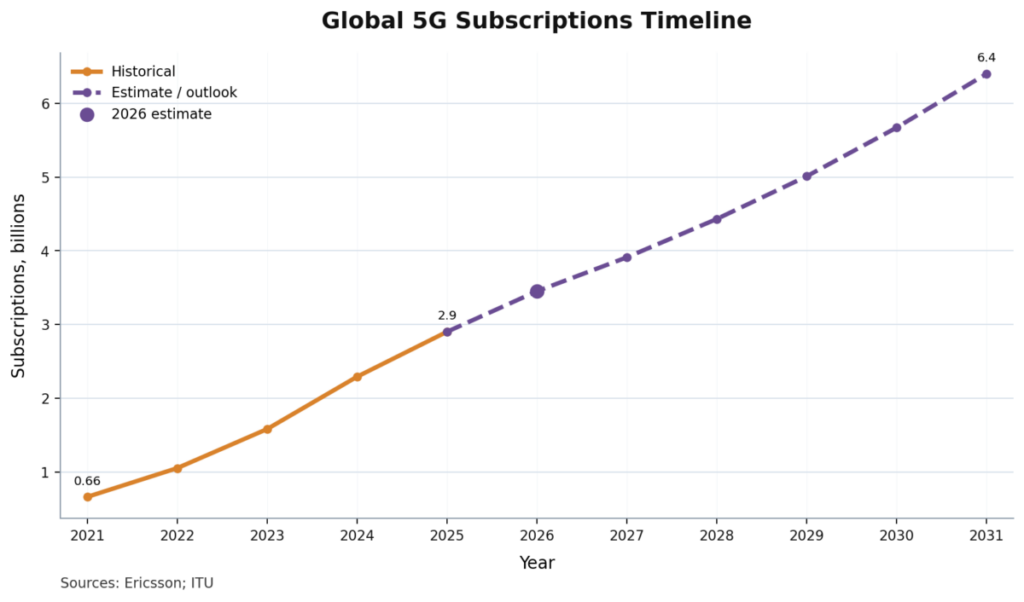

Global 5G subscriptions passed 3 billion in 2026, and 5G carried about half of the world’s mobile data traffic. Mobile network data traffic grew 22% between Q1 2025 and Q1 2026. Fixed wireless access also became more important, with around 70% of FWA service providers offering the service over 5G.

Key takeaway: 5G passed 3 billion subscriptions in 2026 and now carries about half of global mobile data traffic.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| 5G subscriptions | 3.00B | 3.45B | 15.0% | ITU; Ericsson |

| 5G mobile data share | 48% | 52% | 8.3% | Ericsson |

| Monthly mobile data traffic | 172 EB | 210 EB | 22.1% | Ericsson |

| 5G FWA provider share | 65% | 71% | 9.2% | Ericsson |

* Estimate

Major Milestones

The industry has reached the point where connectivity is treated as a utility-like condition rather than a discretionary service. Internet and mobile access now support financial transfers, business operations, digital public services, employment platforms, education systems, and healthcare interfaces. The cost of failure has moved beyond the telecom sector and into the wider economy.

A second milestone is the rise of resilience as a core industry measure. Connectivity policy is increasingly tied to national economic continuity because the internet depends on cross-border physical, digital, and energy infrastructure. Advanced digital economies must manage continuity risk, while developing economies must manage the risk that weak access slows modernization before digital gains can compound.

A third milestone is the elevation of device ownership into an economic access issue. Mobile phones now function as identity gateways, payment instruments, public-service access points, learning devices, and work interfaces. By April 2026, smartphones represented about 89.1% of mobile phone handsets in use and 85.5% of total cellular mobile connections, supporting the shift from basic connection counts toward device-enabled participation.

The industry also reached two major scale markers between 2025 and mid-2026. Internet adoption crossed the 6 billion-user threshold in 2025, and unique mobile users reached 5.83 billion by April 2026.

Key takeaway: Connectivity has become a utility-like condition because economic and public systems increasingly assume that digital access is continuous.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Internet adoption threshold | 6.00B users | 6.18B users | 3.0% | ITU; DataReportal |

| Unique mobile user threshold | 5.78B users | 5.88B users | 1.7% | DataReportal |

| Smartphone handset share | 87.5% | 89.5% | 2.3% | DataReportal |

| Mobile broadband intensity | 99 per 100 people | 101 per 100 people | 2.0% | ITU |

* Estimate

Industry Outlook

The near-term outlook is shaped by the movement from coverage expansion to capacity, reliability, and service quality. Mobile broadband and 5G adoption will continue to rise, but the industry’s next phase depends on how well networks handle heavier traffic, higher institutional dependence, and more demanding industrial use.

The long-term outlook points toward a more integrated ICT infrastructure stack in which mobile networks, cloud platforms, edge computing, satellite systems, devices, and AI-capable endpoints operate as one connected environment. Markets that expand coverage without solving affordability, device access, or resilience will continue to show a gap between statistical availability and practical use.

Mobile’s economic contribution is projected to rise from $7.6 trillion in 2025 to $11.3 trillion by 2030. 5G now carries about half of mobile data traffic, and mobile network data traffic grew 22% between Q1 2025 and Q1 2026. The long-range outlook is therefore centered on capacity, differentiated service, and network quality rather than simple user-count growth.

The outlook remains uneven. 5G covered 55% of the world’s population in 2025, but coverage reached 84% in high-income countries and only 4% in low-income countries. The next stage of industry expansion depends on converting coverage into usage and extending higher-capacity networks beyond advanced urban markets.

Key takeaway: The industry outlook is no longer defined only by more users coming online; it is defined by whether networks can support continuous, affordable, high-capacity use.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Mobile economic value | $7.6T | $8.2T | 7.9% | GSMA |

| 5G subscriptions | 3.00B | 3.45B | 15.0% | ITU; Ericsson |

| 5G population coverage | 55% | 60% | 9.1% | ITU |

| 5G mobile data share | 48% | 52% | 8.3% | Ericsson |

| 2030 mobile value forecast | $7.6T | $11.3T by 2030 | 48.7% | GSMA |

* Estimate

Supplemental Information

Ecological / Environment

ICT’s environmental position is tied to the infrastructure required to sustain data growth. Higher mobile traffic, cloud dependence, edge computing, satellite expansion, and AI-capable networks require more energy, equipment, land use, cooling, and hardware renewal. The available connectivity statistics show rising dependence on digital infrastructure, but they do not by themselves prove a net environmental gain or loss.

The main environmental issue is capacity discipline. As networks carry more traffic and support more economic functions, energy efficiency, equipment lifecycle management, network sharing, spectrum efficiency, and data-center power sourcing become more important to the industry’s physical footprint. Environmental claims should remain limited unless the research packet includes direct evidence on electricity use, emissions, e-waste, cooling demand, or equipment replacement cycles.

Key Global Stats

Global Internet Adoption

Global internet use reached about 6 billion people in 2025, equal to roughly three-quarters of the world’s population. The offline population remained about 2.2 billion. The 2025 internet-user baseline rose from a revised 5.8 billion users in 2024, creating a year-over-year increase of about 200 million users.

By April 2026, global internet use reached 6.12 billion people, equal to 73.8% of the world population. Reported internet users increased by 59 million over the prior year in the DataReportal series, while close to 2.2 billion people remained offline. The 2026 figure should be treated as latest available rather than final year-end data.

Key takeaway: Internet use reached about 6 billion people in 2025 and 6.12 billion by April 2026, while about 2.2 billion people remained offline.

Mobile Broadband Subscriptions

Mobile broadband reached 99 subscriptions per 100 inhabitants in 2025 and represented 89% of all mobile subscriptions. Mobile broadband coverage is now nearly universal, but the next divide sits inside quality, affordability, and practical service conditions.

The mobile market reached 5.78 billion unique mobile users in October 2025 and 5.83 billion by April 2026. The April 2026 reading represented 70.4% of the global population and added 103 million users over twelve months, giving unique mobile use annual growth of 1.8%.

Key takeaway: Mobile broadband now accounts for 89% of all mobile subscriptions, making data access the core mobile service.

5G Coverage and Adoption

5G reached 55% global population coverage in 2025 and accounted for about one-third of mobile broadband subscriptions. The adoption base crossed 3 billion subscriptions by 2026, with 3.1 billion subscriptions recorded after 162 million additions in Q1 2026.

The coverage divide remains substantial. High-income countries reached 84% 5G coverage, while low-income countries reached 4%. This gap places 5G in two different stages at once: a mainstream network layer in advanced markets and a limited-access technology in the lowest-income markets.

Key takeaway: 5G covered 55% of the global population in 2025, but low-income country coverage remained only 4%.

Mobile Data Traffic

Mobile network data traffic grew 22% between Q1 2025 and Q1 2026. 5G now carries about half of global mobile data traffic, and total monthly global mobile network data traffic reached 210 exabytes in Q1 2026.

5G carried 48% of mobile data traffic at the end of 2025 and about half in the latest 2026 reading. The traffic share is forecast to rise to 85% by 2031, placing 5G capacity at the center of long-term mobile network planning.

Key takeaway: Mobile data traffic grew 22% year over year through Q1 2026, with 5G carrying about half of global mobile traffic.

Mobile Economic Footprint

Mobile technologies and services generated $7.6 trillion in economic value in 2025, equal to 6.4% of global GDP. The figure is projected to reach $11.3 trillion by 2030 as 5G, AI, and related digital technologies expand across consumer and enterprise use cases.

The 2025 figure follows a 2024 baseline of $6.5 trillion, giving the mobile industry a one-year increase of about $1.1 trillion in measured economic contribution. The economic footprint reflects mobile’s role as a general-purpose infrastructure layer, with value extending beyond operator revenue.

Key takeaway: Mobile generated $7.6 trillion in economic value in 2025 and is projected to reach $11.3 trillion by 2030.

Notable Country / Region Stats

China remains the largest mobile connection market by scale. A total of 1.83 billion cellular mobile connections were active in China in late 2025, equal to 129% of the national population. China’s connection base is large enough to shape global subscription, device, traffic, and infrastructure totals.

India remains one of the largest mobile and internet adoption markets. National digital participation is shaped by mobile-first access and rapid 5G expansion, and current mobile network traffic growth has been driven strongly by India and North America. Together, China and India define the scale side of global mobile adoption.

The United States remains a high-penetration mobile and internet market. The country had 417 million cellular mobile connections at the end of 2025, and mobile connectivity is deeply embedded in household access, enterprise systems, cloud-linked services, and digital commerce.

Nigeria illustrates the scale of the remaining adoption gap in large emerging markets. Internet use continues to expand, but affordability, device access, service quality, and rural coverage remain central constraints. This pattern reflects the broader global distinction between statistical coverage and meaningful connectivity.

Regional differences are most visible in 5G coverage. High-income markets have moved into broad 5G availability, while low-income markets remain near the beginning of 5G deployment. Global averages can conceal large gaps in network generation, service quality, and practical affordability.

Key takeaway: China and India define mobile scale, high-income regions define mature 5G availability, and low-income markets define the remaining coverage challenge.

Keywords: Internet Connection Technology, ICT, Mobile Broadband, 5G, Digital Connectivity, Internet Adoption.