{kind=link}

The internet has become the central operating layer of the modern economy. Connectivity now determines practical participation in finance, health access, work, education, commerce, communication, and public services. Cloud infrastructure supplies the computing base behind that participation, while artificial intelligence is turning the network from an information system into an action system. IoT extends internet logic into physical environments, and the internet’s transaction, care, settlement, and automation layers now reach deeper into institutional life.

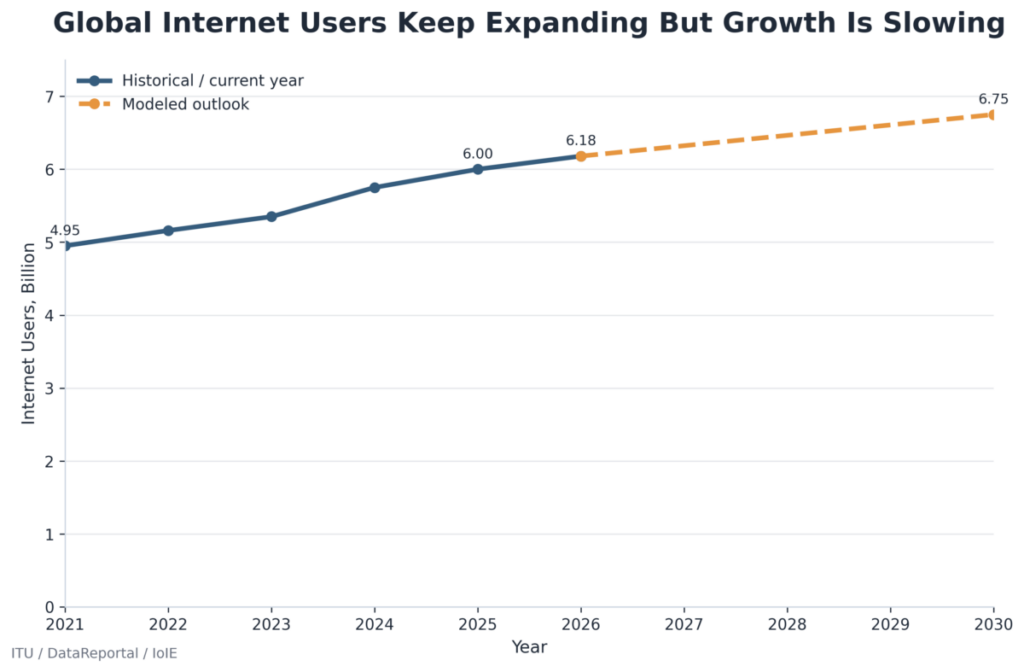

The mid-year picture is one of scale and strain. More than 6.1 billion people are online, and the full-year estimate is moving toward 6.18 billion, up from 6.00 billion in 2025. Nearly 5.9 billion people use mobile connections, and mobile technology is moving toward $8.2 trillion in economic value, up from $7.6 trillion in 2025. Yet roughly 2.1 billion people remain offline, making internet exclusion a widening economic and institutional divide rather than a narrow communications gap. The internet’s balance sheet has changed: user growth remains important, but the larger test is whether the systems already online can keep carrying the world that now depends on them.

The internet at mid-year 2026 is no longer defined by novelty or reach alone. It is being judged by capacity, reliability, inclusion, security, and the physical cost of keeping digital systems available at economic scale. The earlier internet story was expansion; the current story is the institutional stress created by dependence.

| Internet Statistics | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Global internet users | 6.00B | 6.18B | 3.0% | IoIE |

| Offline population | 2.20B | 2.10B | -4.5% | IoIE |

| Mobile technology economic value | $7.6T | $8.2T | 7.9% | IoIE |

| Worldwide AI spending | $1.75T | $2.52T | 44.0% | IoIE |

| Global IoT market | $864.32B | $1.055T | 22.1% | IoIE |

| Global retail e-commerce sales | $6.419T | $6.880T | 7.2% | IoIE |

* Estimate

Access Became Economic Participation

The first generation of internet measurement asked who was online. The sharper 2026 question is whether being online is strong enough to count as participation. A weak or unaffordable connection may still deliver messages, but it can leave households constrained when work, banking, healthcare, schooling, and government services depend on stable digital access.

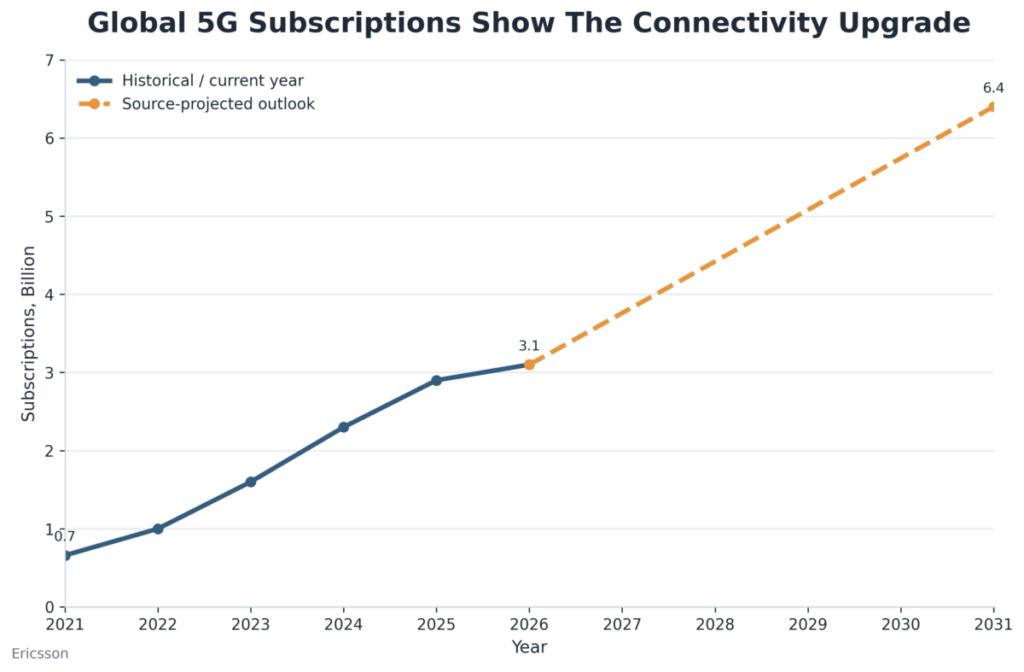

Mobile broadband reached 99 subscriptions per 100 inhabitants in 2025, showing that the basic mobile internet layer has become nearly universal in statistical terms. The more advanced layer is growing quickly as well. 5G subscriptions passed 3 billion in 2026, mobile data traffic rose 22% between the first quarters of 2025 and 2026, and 5G now carries about half of global mobile data traffic. Advanced mobile infrastructure is becoming one of the main carriers of internet growth.

The problem is distribution. 5G covered 55% of the world’s population in 2025, but coverage reached 84% in high-income countries and only 4% in low-income countries. The divide has moved from access to meaningful access, and that difference increasingly determines who can participate in the internet economy on equal terms. When connection quality is uneven, the economy’s digital front door does not open the same way for everyone.

The continuity question reaches beneath the consumer device. Satellite capacity, network routing, submarine cables, spectrum policy, and cloud interconnection define whether digital access can remain stable when daily economic activity assumes constant connection. Connectivity has become less like a communications amenity and more like the first condition of institutional participation.

| Connectivity Statistics | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Global internet users | 6.00B | 6.18B | 3.0% | IoIE |

| Offline population | 2.20B | 2.10B | -4.5% | IoIE |

| Mobile broadband subscriptions | 99 per 100 people | 101 per 100 people | 2.0% | IoIE |

| 5G subscriptions | 2.9B | 3.1B+ | 6.9% | Ericsson |

| 5G share of mobile data traffic | 48% | 50%+ | +2 pp | Ericsson |

* Estimate

Cloud Became The Processing Base

Once access becomes assumed, the next question is where the work of the internet happens. Increasingly, it happens in the cloud. Cloud infrastructure now holds institutional data, runs software, secures workloads, supports AI models, and mediates how organizations buy and deploy digital tools.

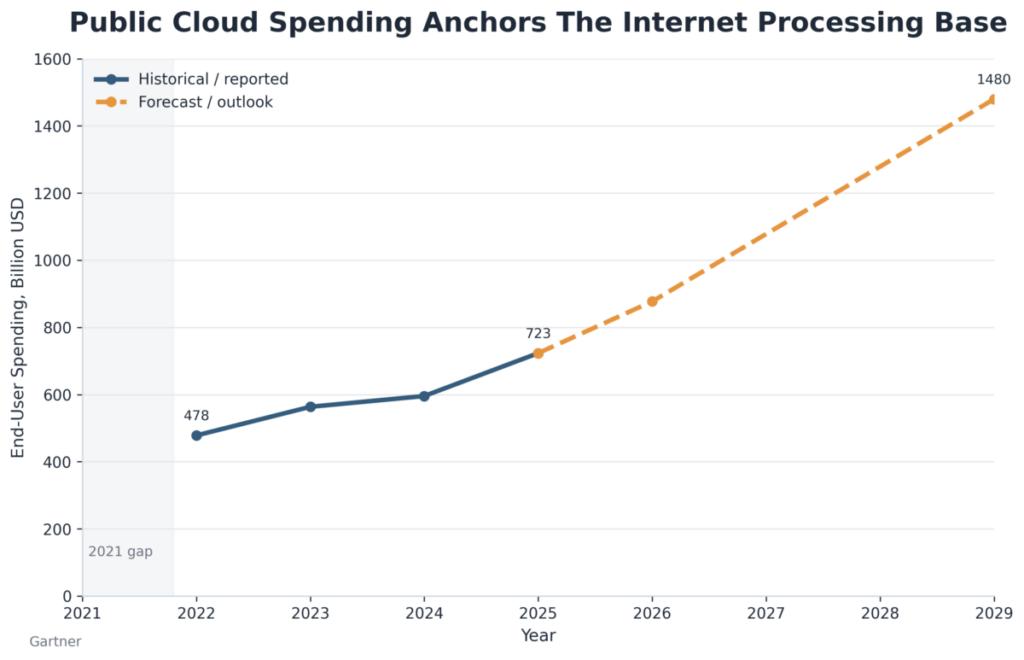

Cloud infrastructure services revenue reached about $419 billion in 2025, making cloud one of the internet economy’s main industrial bases. Broader public cloud end-user spending reached about $723.4 billion, while IaaS accounted for about $211.9 billion and PaaS accounted for about $208.6 billion. These figures place cloud beyond outsourced technology. It is now a market, a utility-like dependency, and a governance concern at the same time.

The concentration of the cloud market gives that dependency a strategic edge. Amazon, Microsoft, and Google together held about 63% of global enterprise cloud infrastructure spending. Google Cloud ended 2025 above a $70 billion annualized run rate with about $240 billion in backlog, while Oracle cloud infrastructure revenue grew 93% year over year in fiscal Q4 2026. The center of gravity is not only compute consumption; it is control over the channels through which enterprises purchase and operate digital capacity.

Hyperscaler marketplace sales reached about $30 billion in 2024 and are forecast to reach about $163 billion by 2030, turning cloud platforms into procurement channels as well as computing systems. Sovereign cloud IaaS spending is forecast at $80 billion in 2026, up 35.6% from 2025, as governments and regulated industries seek more control over where data and workloads reside. Cloud’s growth is therefore also a market-structure story, because the same platforms that supply capacity increasingly shape where software is bought and governed.

Cloud’s next limit is not demand. It is the physical capacity to keep adding compute. Data centers captured more than one fifth of global greenfield investment in 2025, with announced foreign direct investment in the sector exceeding an estimated $270 billion. The cloud still feels weightless from the user’s screen, but its operating reality is capital-heavy and increasingly energy-bound. Data centers are becoming the internet’s new industrial geography.

| Cloud and IaaS Statistics | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Public cloud end-user spending | $723.4B | $877.5B | 21.3% | Gartner |

| Cloud infrastructure services revenue | $419B | $509B | 21.5% | IoIE |

| IaaS spending | $211.9B | $256.2B | 20.9% | IoIE |

| PaaS spending | $208.6B | $253.0B | 21.3% | IoIE |

| Sovereign cloud IaaS spending | $59.0B | $80.0B | 35.6% | Gartner |

* Estimate

AI Changed The Function Of The Web

Cloud supplied the processing base; AI is changing what that base is asked to do. The web once waited for users to search, click, read, compare, and decide. The AI web tries to infer intent and convert information access into task direction.

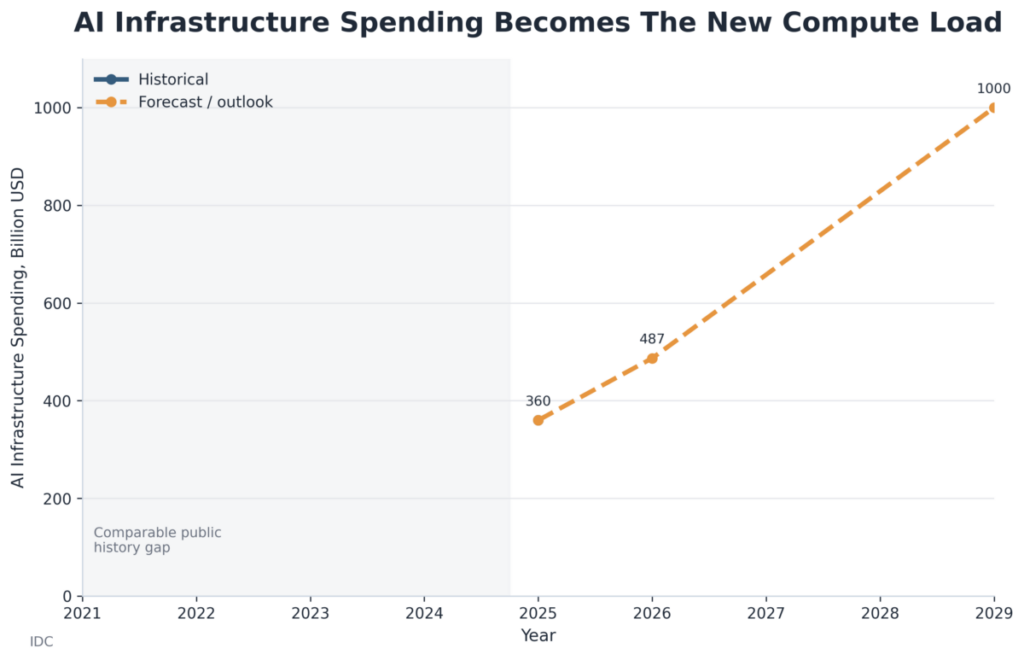

Worldwide AI spending is forecast at $2.52 trillion in 2026, up from $1.75 trillion in 2025. Global corporate AI investment reached $581.7 billion in 2025, confirming that AI is no longer a speculative software segment. It is becoming a capital-intensive interface across the internet economy.

User adoption has moved at platform speed. Standalone generative AI users rose from about 1.0 billion in 2025 to 2.42 billion by April 2026, while the broader active AI user base reached about 4 billion. Enterprise adoption is also broad, with 88% of organizations using AI in at least one business function in 2025. AI now stands between users and the web more often, turning open-ended browsing into mediated answers and task completion.

The mid-year shift is from assistance toward execution. Agentic AI was already being scaled by 23% of organizations in 2025, while another 39% were experimenting with it. AI has also moved into ordinary information discovery, with 60% of U.S. adults having read AI summaries in search results in 2026 and 42% using chatbots to search for information. The internet’s distribution layer is being reorganized around machine-generated answers, not only human navigation.

A contrast now defines the web’s next phase: the old internet organized human browsing; the new one increasingly organizes machine-mediated action. Every answered prompt, generated image, code suggestion, product comparison, customer-service exchange, and automated workflow draws on a compute stack. AI infrastructure alone is expected to add $401 billion in spending in 2026, while global data-center electricity demand could exceed 1,700 TWh by 2035 in a high-adoption AI case. AI turns demand for answers into demand for power, chips, land, cooling, and institutional governance.

| Artificial Intelligence: Annual Statistics and 2026 Estimates | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Worldwide AI spending | $1.75T | $2.52T | 44.0% | IoIE |

| Corporate AI investment | $581.7B | $720.0B | 23.8% | IoIE |

| Standalone generative AI users | 1.0B | 2.42B | 142.0% | IoIE |

| Active AI user base | 3.0B | 4.0B | 33.3% | IoIE |

| Enterprise AI adoption | 78% | 88% | +10 pp | IoIE |

* Estimate

The Physical Economy Moved Online

As AI makes the internet more interpretive, IoT extends that interpretive capacity into physical environments. The Internet of Things gives the physical world a digital nervous system. Its importance is not simply that there are more connected devices; its importance is that more physical activity can be observed by software, translated into data, and coordinated across systems.

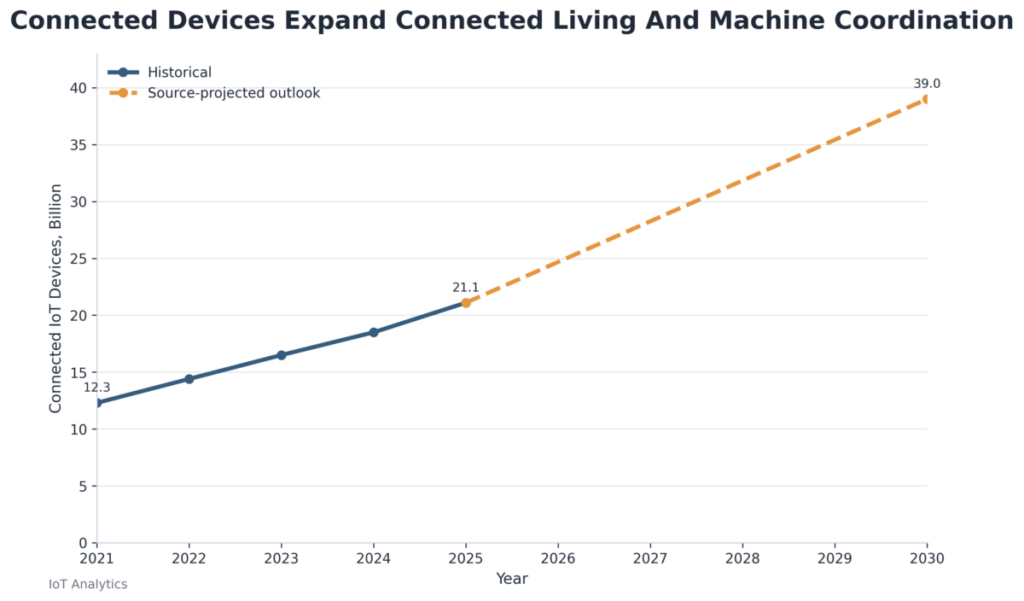

The global IoT market is estimated at $1.055 trillion in 2026, up from $864.32 billion in 2025, a 22.1% increase. Connected IoT devices are expected to reach 24.1 billion in 2026, up from 21.1 billion in 2025, and could approach 39 billion by 2030. The smart-home market is moving from $162.8 billion to $207.0 billion, while enterprise IoT is rising from $324.0 billion to $369.4 billion. IoT has moved beyond consumer novelty and into the infrastructure of households, firms, and physical systems.

The category is moving from sensing toward coordination. A connected device once meant a remote reading or a notification. Increasingly, it means a local decision, an automated adjustment, a maintenance signal, an energy response, or a health alert. Matter is becoming a current-year marker for connected-living maturity, and cybersecurity labeling is now part of the consumer IoT market through the FCC’s U.S. Cyber Trust Mark. Standardization and visible security frameworks matter because the connected world is becoming too large for isolated device ecosystems to carry the next phase of growth.

IoT also shows the internet’s environmental double edge. Sensors can reduce hidden waste by detecting leaks, lowering energy use, improving irrigation, and identifying equipment strain before failure. Sensor-led precision agriculture has reduced water use by 20% to 30% in documented cases. Connected-device growth also increases demand for chips, batteries, replacements, patching, and disposal. The physical world is becoming more readable, but readability has material cost.

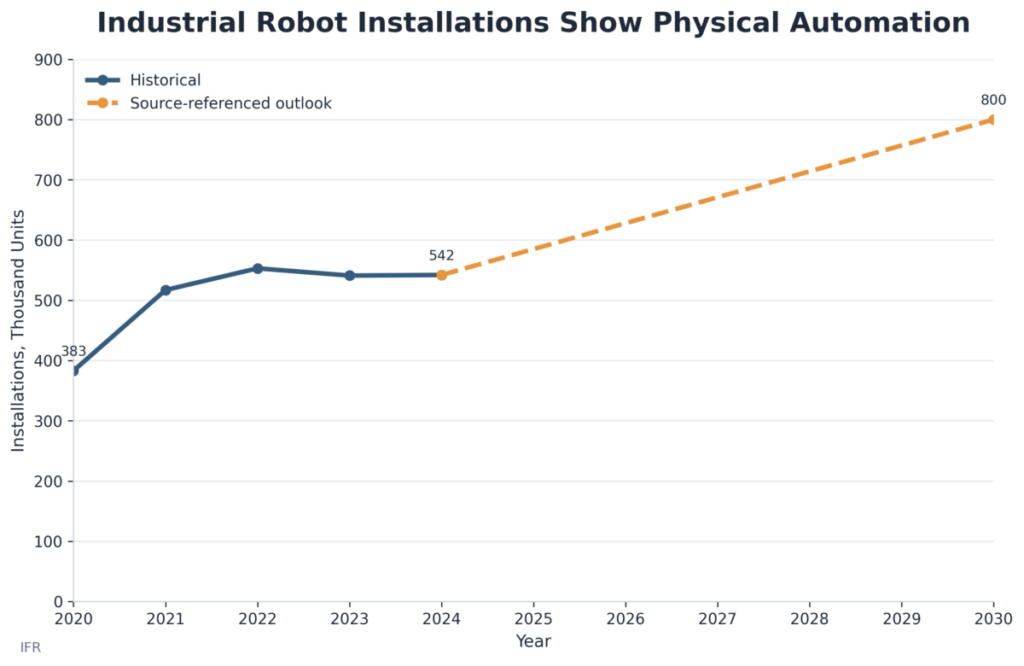

The same movement appears in robotics. Industrial robot installations are rising from 575,000 to 615,000, while the operational robot stock is moving from 5.08 million to 5.53 million. Professional logistics robots are rising from 117,300 to 133,700, showing that physical automation is spreading through the systems that move goods and organize labor.

Autonomous mobility gives the robotics story a public-facing edge. Robotaxi ride scale is moving from more than 14 million trips to more than 26 million. The economic value is also shifting from individual machines toward managed robot fleets, with Amazon operating more than 1 million robots across its logistics system and DeepFleet reducing robot travel time by 10%. Robotics depends on the internet stack because modern machines need sensing, mapping, fleet software, model-driven perception, and networked coordination. The internet is no longer confined to screens. It increasingly appears as monitoring, fulfillment, navigation, care, and movement.

| Connected Living and Physical Automation Statistics | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Global IoT market | $864.32B | $1.055T | 22.1% | IoIE |

| Connected IoT devices | 21.1B | 24.1B | 14.2% | IoIE |

| Smart-home market | $162.8B | $207.0B | 27.1% | IoIE |

| Enterprise IoT market | $324.0B | $369.4B | 14.0% | IoIE |

| Industrial robot installations | 575,000 | 615,000 | 7.0% | IoIE |

| Operational robot stock | 5.08M | 5.53M | 8.9% | IoIE |

| Professional logistics robots | 117,300 | 133,700 | 14.0% | IoIE |

| Robotaxi ride scale | 14M+ | 26M+ | 85.7% | IoIE |

* Estimate

Transactions Became Faster And More Embedded

Once the internet can interpret intent, commercial systems can move closer to the moment of decision. The internet no longer only creates demand. It settles demand. E-commerce is the visible storefront, while fintech is the timing change beneath it.

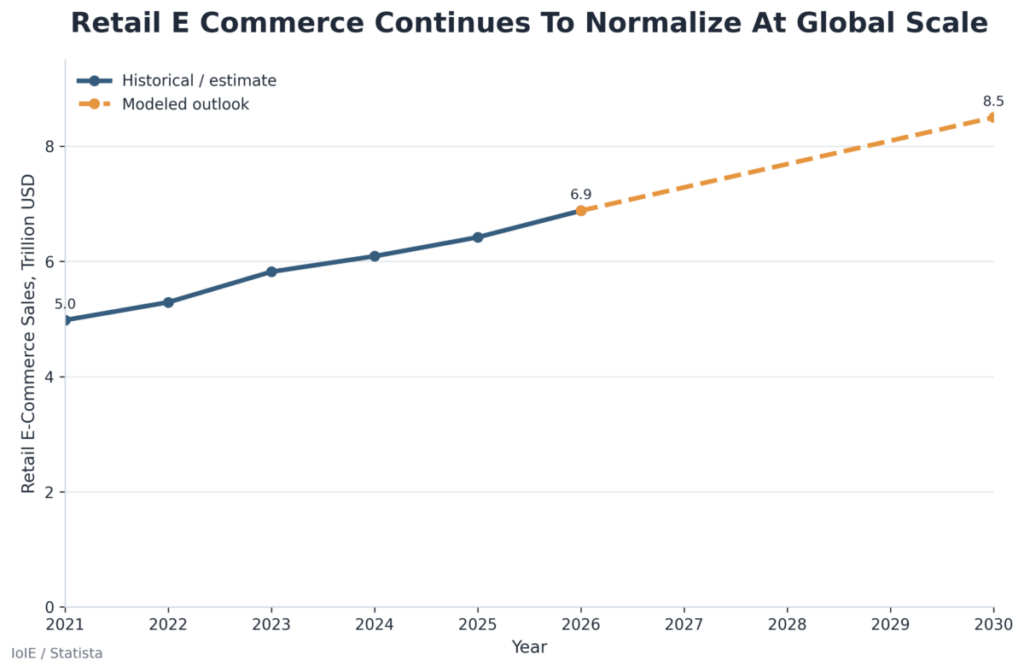

Global retail e-commerce is estimated at $6.880 trillion in 2026, up from $6.419 trillion in 2025. U.S. retail e-commerce is estimated at $1.307 trillion in 2026 after $1.234 trillion in 2025. In the first quarter of 2026, U.S. retail e-commerce reached $326.7 billion and accounted for 16.9% of total U.S. retail sales. The lead story is not only continued growth; it is the normalization of online commerce as a standing share of retail activity.

The commercial internet is larger than retail. Business e-commerce is rising from $35.9 trillion to $39.5 trillion under the available estimate, while online shoppers rise from 2.77 billion to 2.95 billion. The shopping experience is also becoming less like browsing and more like guided conversion. Traffic from generative AI sources to U.S. retail sites rose 693.4% year over year during the 2025 holiday season, turning AI discovery into a measurable commercial channel.

Payment behavior shows the same compression of intent into transaction. Mobile devices accounted for 56.4% of online holiday transactions, while buy now, pay later purchases reached $20.0 billion during the same season. The internet’s commercial layer now turns attention, recommendation, payment flexibility, and fulfillment control into one transaction environment. Returns and cross-border compliance are becoming harder operating limits, with U.S. retail returns projected at $849.9 billion in 2025 and 19.3% of online sales expected to be returned.

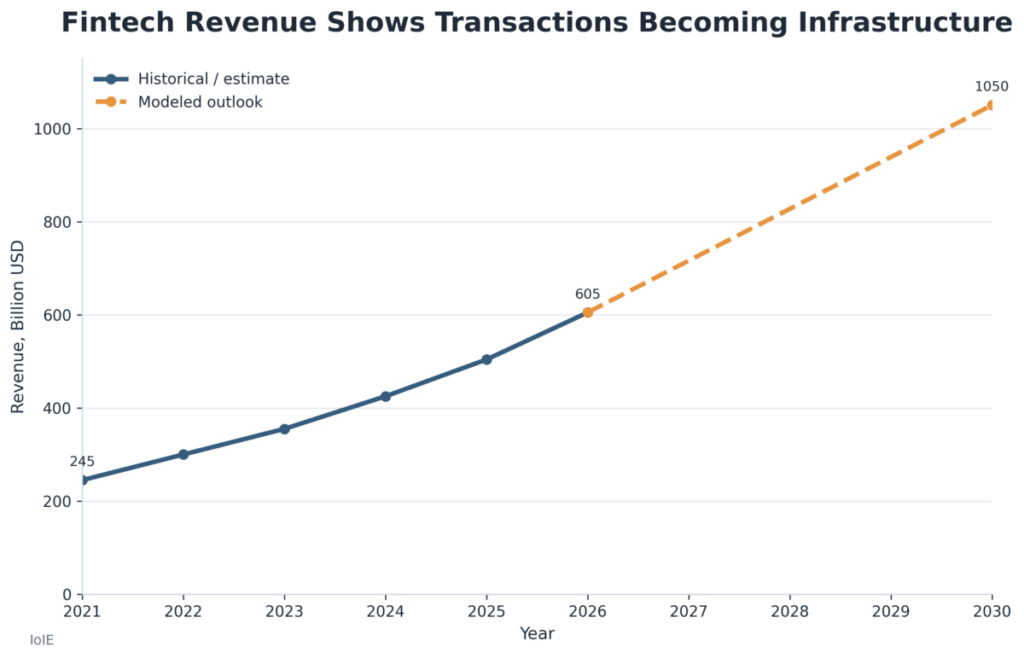

Fintech extends that environment into the movement of money itself. Global fintech revenue is moving from $504 billion in 2025 to an estimated $605 billion in 2026. Digital wallet users are rising from 4.4 billion to 4.68 billion, giving the internet’s financial interface a user base comparable to the population scale of the connected world itself.

The deeper change is timing. Mobile money transaction value is moving from more than $2.0 trillion to $2.4 trillion, while open-banking API calls are rising from 137 billion to 208 billion. The economic internet is becoming less about the digital storefront and more about transaction velocity. Money is moving closer to the moment of work, purchase, permission, and settlement.

Blockchain’s place in the internet economy is now clearer because the category has split. Bitcoin has become an institutional asset-market story. Stablecoins have become the more important settlement-infrastructure story.

Bitcoin market capitalization stood near $1.278 trillion in 2026 after $2.054 trillion in 2025. U.S. spot bitcoin ETF assets moved from $107 billion in 2025 to $99.19 billion in 2026, while the number of U.S. spot bitcoin ETF funds rose from 11 launch funds to 37 funds. These figures place Bitcoin inside conventional financial-market plumbing more than outside it.

Stablecoins point toward a different internet function. Stablecoin market capitalization rose from about $211 billion to about $317 billion, while payment stablecoin issuance rose from $250 billion to $500 billion. The relevance is no longer ideological. It is measured through custody, settlement, regulation, security, and energy. The same year that stablecoin infrastructure expanded, crypto security remained a systemic constraint, with the Bybit theft reaching about $1.5 billion and U.S. crypto mining electricity use estimated between 25 TWh and 91 TWh under EIA assumptions.

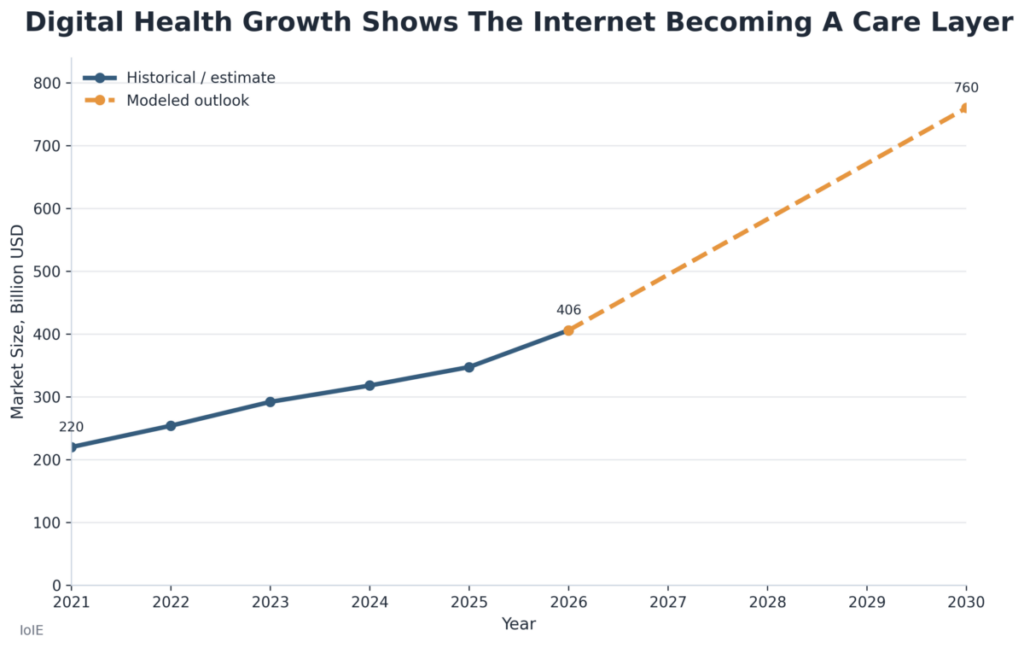

Digital health shows the internet becoming an essential-service layer. The global digital health market is rising from $347.45 billion in 2025 to $405.99 billion in 2026, with an alternate estimate moving from $347.4 billion to $428.7 billion. The internet here is not a destination. It is a care pathway, a records layer, a monitoring system, and a triage interface.

AI is making that health layer more active. The AI healthcare market is rising from $40.14 billion to $53.61 billion. U.S. adults using AI chatbots for health questions doubled from 16% to 32%, while U.S. hospitals using predictive AI in EHRs rose from 66% to 71%. Digital reimbursement is also becoming part of the infrastructure, with more than 300 U.S. billing codes supporting digital health and digital care, including 117 codes specific to software-based technologies. Digital health now sits at the intersection of patient access, institutional data systems, clinical risk, and public trust.

| Digital Transactions: Annual Statistics and 2026 Estimates | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Global retail e-commerce sales | $6.419T | $6.880T | 7.2% | IoIE |

| Business e-commerce sales | $35.9T | $39.5T | 10.0% | IoIE |

| Online shoppers | 2.77B | 2.95B | 6.5% | IoIE |

| Global fintech revenue | $504B | $605B | 20.0% | IoIE |

| Digital wallet users | 4.4B | 4.68B | 6.4% | IoIE |

| Open-banking API calls | 137B | 208B | 51.8% | IoIE |

| Stablecoin market capitalization | $211B | $317B | 50.2% | IoIE |

| Payment stablecoin issuance | $250B | $500B | 100.0% | IoIE |

* Estimate

Dependence Became The Stress Test

The internet’s new problem is not relevance. It is load. The system must carry more economic activity, more health data, more AI decisions, more machine traffic, more public reliance, and more energy demand while remaining trusted.

Bad bots account for 37% of internet traffic, and non-human activity has approached half of measured web activity in recent industry reporting. AI traffic is accelerating the shift toward a machine-mediated internet, with AI requests growing far faster than human traffic in early 2026 and AI crawlers forming the dominant share of observed AI traffic on one major edge network. Bots and AI crawlers now look less like background noise and more like a non-human demand shock on the web’s operating model.

Cybersecurity has become the economic price of dependence. AI-related vulnerabilities were identified by 87% of respondents as the fastest-growing cyber risk over 2025, and cybersecurity product and service spending is projected above $520 billion annually by 2026. The internet’s attack surface now follows the same path as its value creation. As more essential activity moves online, more of the economy becomes exposed to digital failure.

Governance follows dependence. The internet is being pulled into public law because it now carries public reliance. Cloud sovereignty, AI rules, stablecoin regulation, privacy enforcement, marketplace accountability, online safety, and health-data rules are not separate regulatory stories. They are signs that the internet has become too embedded to remain governed only by platform policy and private contracts. By 2025, internet regulation had moved beyond earlier platform-conduct debates into the economic restructuring of data, markets, infrastructure, and digital dependency.

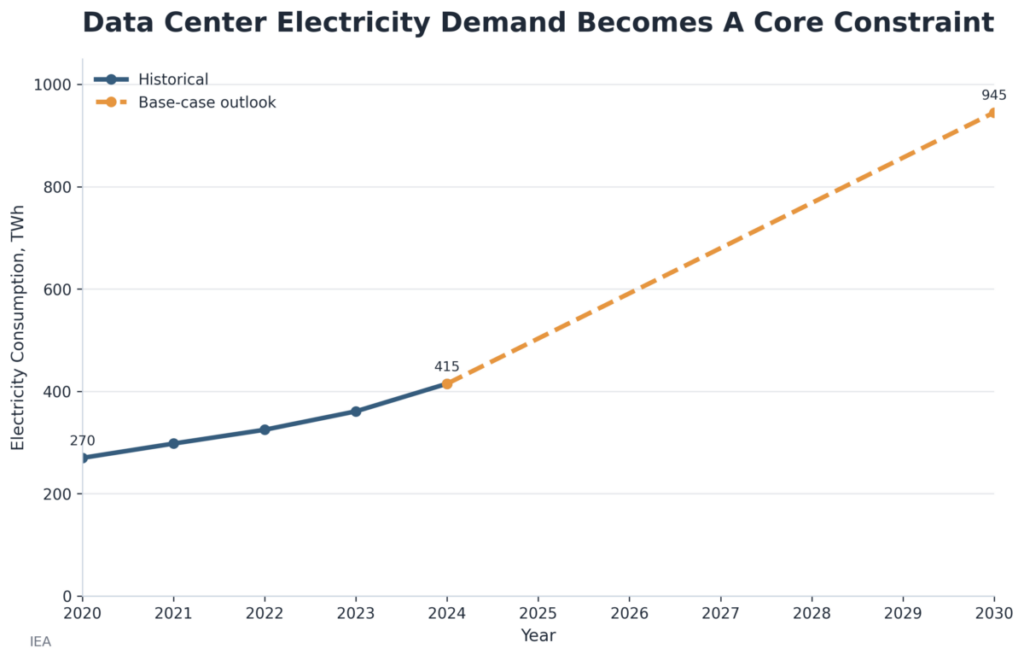

Energy is the other limiting resource. Data centers consumed about 415 TWh of electricity globally in 2024, equal to roughly 1.5% of global electricity use. By 2030, data-center electricity consumption is projected to reach about 945 TWh, or just under 3% of global electricity use. The growth is driven by cloud expansion, AI workloads, and the broader movement of economic activity into compute-intensive systems. Data-center development is also becoming geopolitical industrial policy, with compute capacity now treated as a national and regional economic asset.

The attention layer remains one of the internet’s largest economic engines and one of its most powerful social forces. U.S. internet advertising revenue approached $300 billion in 2025 after growing 13.9%. The internet does not only transmit information; it shapes what people notice, what they feel, what they buy, and what they believe is happening. AI search and recommendation systems make that layer more consequential because discovery is becoming more mediated at the same time the economic stakes of attention remain enormous.

The second half of 2026 is therefore less a forecast than a stress test. The growth story remains strong across users, cloud, AI, IoT, commerce, fintech, health, robotics, digital advertising, and digital money. The harder question is whether the same system can remain secure, inclusive, governable, energy-aware, and resilient.

The internet’s next chapter will not be defined only by faster networks or larger platforms. It will be defined by whether the systems already online can keep carrying the world that now depends on them.

| Trust, Governance, and Energy: Annual Statistics and 2026 Estimates | ||||

|---|---|---|---|---|

| Name | 2025 | 2026 (est)* | % Growth | Source |

| Bad bot share of internet traffic | 37% | 39% | +2 pp | IoIE |

| Cybersecurity product and service spending | $459B | $520B+ | 13.3% | Cybersecurity Ventures |

| Data-center electricity consumption | 503 TWh | 592 TWh | 17.7% | IEA |

| Internet advertising revenue | $294.6B | $326.0B | 10.7% | IAB |

| Sovereign cloud IaaS spending | $59.0B | $80.0B | 35.6% | Gartner |

* Estimate

Key Takeaways

• The internet’s main story has shifted from expansion to institutional dependence.

• More than 6.1 billion people are online, but roughly 2.1 billion remain offline.

• Connectivity quality now matters as much as basic access for economic participation.

• Cloud infrastructure has become the processing base of the internet economy.

• AI is changing the web from an information system into an action system.

• IoT and robotics are extending internet logic into physical environments.

• E-commerce and fintech are compressing discovery, payment, credit, and settlement.

• Stablecoins now matter more as settlement infrastructure than as crypto ideology.

• Digital health shows the internet becoming an essential-service layer.

• Bots and AI crawlers are creating a non-human demand shock on web systems.

• Data centers are turning internet growth into an industrial geography problem.

• The second half of 2026 will test trust, resilience, governance, inclusion, and energy capacity.

Sources

- UNCTAD; Data Centres Are Reshaping Global Investment Landscape; – Link

- GSMA; The Mobile Economy 2026; – Link

- Ericsson; Ericsson Mobility Report June 2026; – Link

- Gartner; Gartner Forecasts Worldwide Public Cloud End User Spending to Total 723 Billion Dollars in 2025; – Link

- Gartner; Gartner Says Worldwide Sovereign Cloud IaaS Spending Will Total 80 Billion Dollars in 2026; – Link

- Gartner; Gartner Says Worldwide AI Spending Will Total 2.5 Trillion Dollars in 2026; – Link

- IoT Analytics; Number of Connected IoT Devices Growing 14 Percent to 21.1 Billion Globally; – Link

- International Federation of Robotics; Global Robot Demand in Factories Doubles Over 10 Years; – Link

- Juniper Research; Digital Wallet Users to Surpass Three Quarters of Global Population by 2030; – Link

- IEA; Energy and AI Executive Summary; – Link

- IEA; Energy Demand From AI; – Link

- World Economic Forum; Global Cybersecurity Outlook 2026; – Link

- Cybersecurity Ventures; Official 2026 Cybersecurity Market Report Predictions and Statistics; – Link

- IAB; Digital Ad Revenue Climbs to Nearly 300B; – Link

- IAB and PwC; Internet Advertising Revenue Report Full Year 2025; – Link

- KFF; Tracking Poll on Health Information and Trust Use of AI for Health Information and Advice; – Link

- ASTP ONC; Hospital Trends in Use Evaluation and Governance of Predictive AI 2023 2024; – Link

- FBI; North Korea Responsible for 1.5 Billion Bybit Hack; – Link

- Reuters; US Online Holiday Spending Hits Record Levels Despite Slower Growth Adobe Says; – Link

- Reuters; EU Targets Big Tech Dependence With Made in Europe Drive; – Link

- Reuters; UN Chief Calls on AI Firms to Come Clean on Environmental Costs; – Link

- Waymo; 2025 Year in Review; – Link

- Amazon; Amazon Reaches 1 Million Robots and Launches DeepFleet AI Foundation Model; – Link

- McKinsey; The State of AI; – Link

- DataReportal; Digital 2026 Mid Year Global Update Report; – Link

- DataReportal; Global Digital Overview; – Link

Keywords: ICT, Digital Infrastructure, Internet Economy, Machine Mediated Web, Institutional Digital Dependence