{kind=link}

Robotics is becoming commonplace as machines grow more visible, capable, and accepted in workplaces, media, transportation systems, logistics networks, and public settings. Machines that once appeared mainly inside factories are now appearing as delivery systems, autonomous vehicles, warehouse fleets, service machines, and early humanoid platforms. The major milestone is not only that robots are improving; it is that physical automation is becoming easier for the public and the workplace to recognize.

The industry is developing from several directions at once. Humanoid and service robots are entering support environments where machines assist people directly, while mobile robotics is becoming more visible through autonomous vehicles and delivery systems. Industrial automation remains the most established path, with robots already embedded in production and supply-chain operations.

The underlying digital stack is enabling this jump by giving robots stronger connectivity, flexible cloud compute, richer sensor input, and faster machine decision systems. Modern robotics is no longer defined only by industrial machines that repeat a fixed task successfully. The category now includes functional machines that adapt, react in real time, and connect software intelligence to physical movement.

Industrial automation remains the largest measurable base of the robotics economy. Global industrial robot installations reached 542,000 units in 2024, keeping annual deployment above 500,000 units for the fourth consecutive year. The global operational stock reached 4.66 million industrial robots, creating a durable installed base inside factories and production systems. Asia accounted for 74% of new deployments, and China accounted for 54%, making industrial robotics both global in reach and concentrated in the world’s largest manufacturing centers.

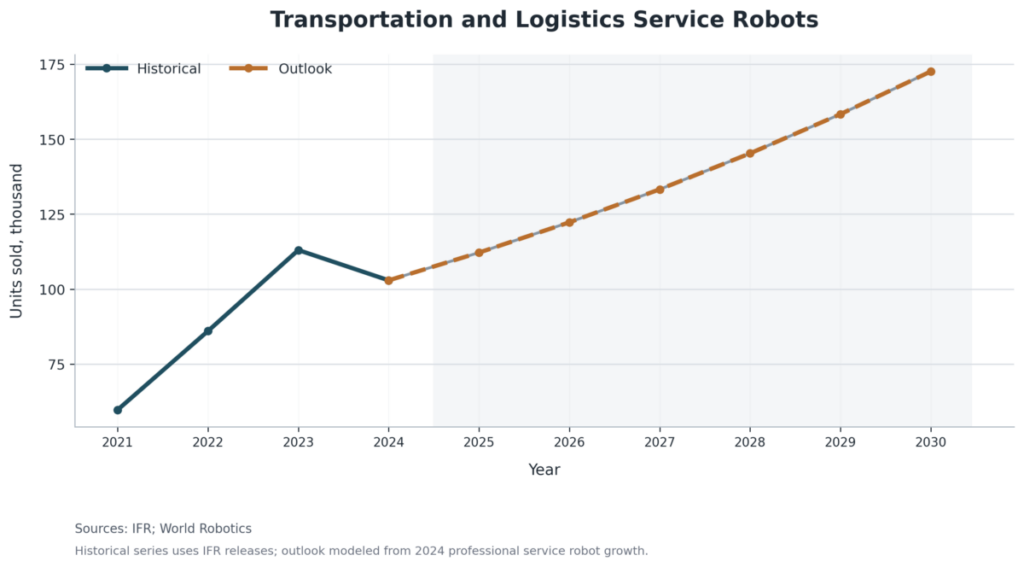

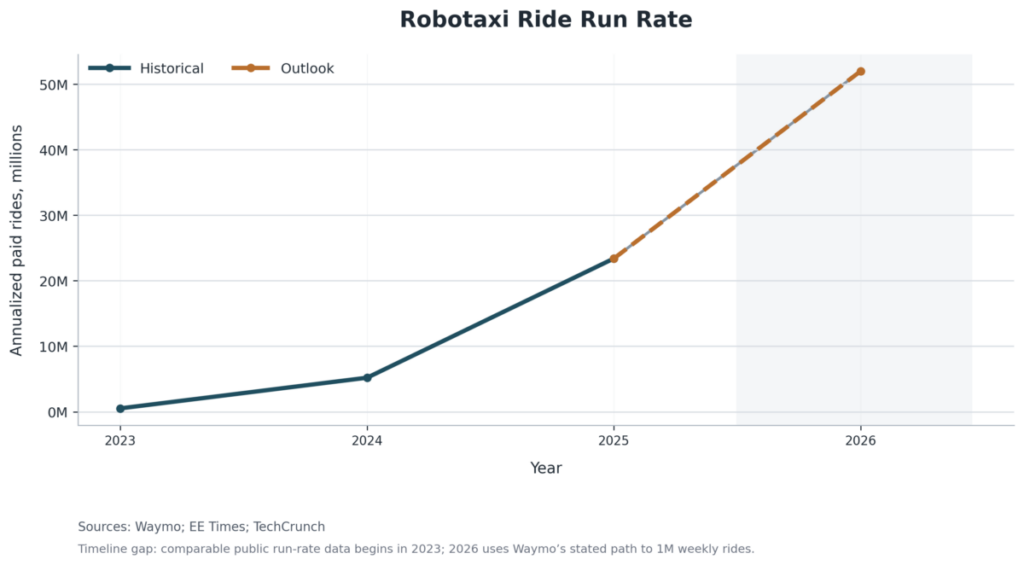

Robotics is also expanding beyond the factory floor. Professional service robots used in transportation and logistics reached 102,900 units sold in 2024, rising 14% from the prior year. Robotics-as-a-Service in that segment grew 42%, making automation easier to adopt through models that reduce upfront ownership requirements. Robotaxis are moving into recurring commercial service, with Waymo surpassing 1 million fully autonomous rides per month in 2025 and reporting more than 500,000 fully autonomous electric vehicle trips per week in 2026.

Humanoid and general-purpose robots remain earlier in commercial development, but they are becoming part of the practical automation pipeline. Planned manufacturing deployments show the category moving toward machines that can perform flexible work near people. Robotics is best understood as the physical execution layer of the internet economy: AI turns data into decisions, IoT turns physical activity into signals, IaaS supplies scalable computing capacity, and robotics turns those digital systems into movement.

Key takeaway: Robotics is becoming commonplace as the physical execution layer of the internet economy, with industrial automation providing the largest installed base while service robots, robotaxis, delivery vehicles, and humanoid systems make machine autonomy more visible in daily work and movement.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Industrial robot installations | 575,000 units | 615,000 units | 7.0% | IFR |

| Industrial robotics market | $37.3B | $41.0B | 9.9% | Grand View Research |

| Factory automation market | $275.0B | $301.4B | 9.6% | MarketsandMarkets |

| Professional logistics robots | 117,300 units | 133,700 units | 14.0% | IFR |

| * Estimate | ||||

New Trends

The clearest current trend is the movement from isolated automation toward networked physical systems. Industrial robots remain the measurable foundation, but service robotics, mobile logistics systems, and autonomous mobility are moving robotics into less controlled environments. Transportation and logistics became the largest professional service robot application class in 2024, tying robotics directly to faster fulfillment, more flexible inventory movement, and software-managed physical flow.

The economic value is shifting from individual machines toward managed robot fleets. Software now coordinates movement, monitors performance, captures operational data, and turns physical activity into a recurring service layer. Amazon’s fulfillment network shows this model at scale, with more than 1 million robots operating across its logistics system and DeepFleet reducing robot travel time by 10%. Robot fleets are becoming operating infrastructure.

Investor and deployment interest is also favoring practical automation over speculative visibility. Task-specific robots are receiving stronger near-term commercial attention because they solve narrow operational problems with clearer payback. Humanoid robotics remains important because it points toward flexible machines that can work in human-designed spaces, but the current market is still led by defined-task robots in structured environments.

Key takeaway: The new robotics cycle is defined by visibility, fleet coordination, and practical deployment, with logistics robots and autonomous vehicles making robotics more commonplace outside traditional factory cells.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Amazon robot fleet | 1.0M+ robots | 1.0M+ robots | N/A | Amazon |

| DeepFleet travel-time gain | 10% | 10% | N/A | Amazon |

| Professional logistics robots | 117,300 units | 133,700 units | 14.0% | IFR |

| Logistics RaaS growth | 42% | 42% | N/A | IFR |

| * Estimate | ||||

Major Milestones

The most important milestone is the normalization of robotics. Robots now appear in workplace planning, warehouse operations, autonomous mobility services, and public expectations about automation in ways that make the category more visible than it was a decade ago. This shift does not mean general-purpose robots have matured; it means the public and commercial presence of robotics has crossed into everyday awareness.

Industrial robotics also reached durable scale. Installations remained above half a million units in 2024, operational stock rose to 4.66 million units, and China remained the largest market with 295,045 new industrial robot installations and more than 2.0 million robots in operation. Global robot density reached 177 industrial robots per 10,000 manufacturing employees, while Korea remained the highest-density market at 1,220.

Key takeaway: Robotics has reached a visibility milestone in daily life while industrial robot stock, installation volume, and robot density confirm a durable installed base inside production systems.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Industrial robot installations | 575,000 units | 615,000 units | 7.0% | IFR |

| Operational robot stock | 5.08M units | 5.53M units | 8.9% | IFR |

| Robot density | 189 per 10,000 workers | 202 per 10,000 workers | 6.9% | IFR |

| Robotaxi ride scale | 14M+ trips | 26M+ trips | 85.7% | Waymo |

| * Estimate | ||||

Industry Outlook

The near-term outlook is positive but uneven. Global robot installations remain high by historical standards, service robotics is growing in logistics, and robotaxi deployments are showing recurring consumer use in selected cities. The broader industrial control and factory automation market is forecast to expand from roughly $275 billion in 2025 to more than $435 billion by 2030, showing that the economic opportunity extends beyond robot hardware.

Long-term growth depends on whether robotics can keep moving from controlled settings into variable environments. Industrial robots have proven value in structured production systems, while mobile robots and autonomous vehicles are proving useful in mapped service areas and facility-based operations. Humanoid robots still face practical barriers around cost, reliability, dexterity, safety, and deployment economics.

Interoperability will shape the next stage of adoption. Multi-vendor robot fleets need common ways to exchange location, status, tasking, availability, and performance data. Shared fleet-management interfaces reduce the custom engineering burden each time a facility adds a new machine, making robotics more scalable as an operating system for physical work.

Key takeaway: Robotics is likely to keep expanding, but the pace will differ sharply between proven industrial systems, logistics robots, autonomous vehicles, and early-stage humanoid machines.

| Name | 2025 | 2026 (est)* | % Growth | Source |

|---|---|---|---|---|

| Factory automation market | $275.0B | $301.4B | 9.6% | MarketsandMarkets |

| Industrial robotics market | $37.3B | $41.0B | 9.9% | Grand View Research |

| Industrial robot installations | 575,000 units | 615,000 units | 7.0% | IFR |

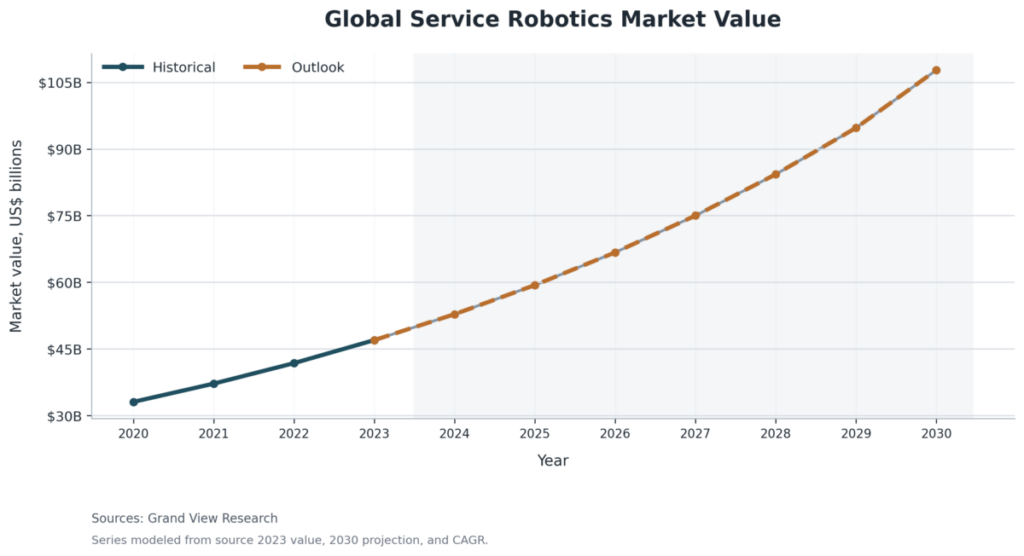

| Service robotics market | $59.8B | $67.2B | 12.4% | Grand View Research |

| * Estimate | ||||

Supplemental Information

Ecological / Environment

Robotics and industrial automation affect environmental performance through energy use, material efficiency, factory utilization, and production quality. Automated systems can reduce scrap, improve process control, and support predictive maintenance, but they also add equipment, electronics, software infrastructure, and energy demand. The available statistics do not provide a reliable global estimate for robotics-specific environmental impact.

Autonomous vehicles add a separate environmental dimension because robotaxi fleets can be electric, centrally managed, and routed through shared mobility systems. Waymo reports more than 500,000 fully autonomous electric vehicle trips per week and reports avoided emissions from its fleet operations, but those figures apply to its own operating assumptions and should not be generalized to the full robotics sector.

Key takeaway: Robotics may improve industrial efficiency, but the public data supports specific operational claims more strongly than broad global environmental claims.

Regulation and Risk

Robotics is facing a broader governance burden as machines move closer to people and public environments. ISO 10218 was updated in 2025 for industrial robot safety, and the EU Machinery Regulation 2023/1230 will apply from 20 January 2027. Modern robots are increasingly connected, software-controlled, and integrated into workplaces where human safety depends on system design, maintenance, and update governance.

Robotics governance is shifting from certifying a fixed machine at deployment to managing a software-defined system over time. Updates can change navigation behavior, speed thresholds, object recognition, task performance, and other safety-relevant functions after a robot is already operating. Robotaxis show the constraint clearly because commercial ride volumes can grow while edge cases still require software recalls, operating restrictions, and city-by-city safety validation.

Key takeaway: Robotics adoption is expanding, but safety validation, software reliability, cybersecurity, and lifecycle governance remain central constraints.

Key Global Stats

Industrial Robot Installations and Installation Value

Global industrial robot installations reached 542,000 units in 2024. That figure kept annual deployment above 500,000 units for the fourth consecutive year and established industrial robotics as the most mature measurable base of the robotics economy. The estimated global installation value reached $16.7 billion, giving the category a measurable investment base beyond unit shipments.

Key takeaway: Industrial robot installations remained above 500,000 units in 2024, confirming robotics as a recurring global capital category.

Operational Robot Stock and Robot Density

The worldwide operational stock of industrial robots reached 4.66 million units in 2024. Operational stock is more important than annual installations for understanding automation depth because it measures the robot base already active inside production systems. Global robot density reached 177 robots per 10,000 manufacturing employees, showing that automation is becoming more embedded relative to the industrial workforce.

Key takeaway: The 4.66 million robots already in operation and global robot density of 177 show that industrial robotics is now an installed infrastructure base, not only a shipment market.

Service Robots and Logistics Automation

Professional service robots used in transportation and logistics reached 102,900 units sold in 2024, rising 14% from the prior year. This made transportation and logistics the largest professional service robot application class. Robotics-as-a-Service in the same segment grew 42%, showing that adoption is beginning to shift from asset purchase toward managed automation capacity.

Amazon’s fulfillment network shows the scale effects of logistics robotics. More than 1 million robots now operate across its system, and DeepFleet reduces robot travel time by 10%. Those gains matter because small improvements in travel time, routing, and coordination can compound across high-volume fulfillment networks.

Key takeaway: Logistics robotics is becoming the strongest service-robotics category, with fleet coordination and RaaS models showing how robots become everyday operating infrastructure.

Autonomous Mobility

Waymo served more than 14 million trips in 2025 and passed 1 million fully autonomous rides per month during the year. By 2026, Waymo was reporting more than 500,000 fully autonomous electric vehicle trips per week. The robotaxi segment remains smaller than industrial automation, but it is one of the clearest examples of robotics moving into recurring consumer service.

Key takeaway: Robotaxis have moved from pilot visibility into recurring commercial use, making autonomous robotics more visible to the public even while deployment remains geographically limited and safety-constrained.

Regional Concentration

Asia accounted for 74% of new industrial robot deployments in 2024, while Europe accounted for 16% and the Americas accounted for 9%. China alone accounted for 54% of global industrial robot installations. This distribution makes robotics global in technology reach but concentrated in the regions with the deepest manufacturing ecosystems.

Key takeaway: Robotics deployment is global, but industrial robot adoption remains heavily concentrated in Asia and especially China.

Notable Country / Region Stats

China remained the dominant national market for industrial robots in 2024, installing 295,045 units and operating more than 2.0 million robots. Its scale makes China the central market for both robot demand and supplier competition. Chinese manufacturers also increased their share of the domestic market, showing that robot production capacity is becoming more localized in the world’s largest deployment base.

Japan remained the second-largest industrial robot market, while the United States, Korea, and Germany rounded out the top five. Together, the five largest markets accounted for 80% of global installations in 2024. The United States installed 34,164 industrial robots in 2024, and North America’s 2025 order rebound suggests continued investment in manufacturing, logistics, and general industry automation.

Europe’s automation market is shaped by high manufacturing density and stronger lifecycle regulation. Germany remained Europe’s largest robotics market, while the EU Machinery Regulation will become a major compliance milestone for machinery and automation systems placed on the European market from January 2027. The regional impact is also developmental: high-income economies use automation to offset labor scarcity and aging, while lower-income economies may feel robotics first through global supply-chain restructuring before local deployment becomes widespread.

Key takeaway: Robotics deployment is global in reach but concentrated in a small group of industrial economies, with China operating at a scale no other national market currently matches.

Keywords: Robotics, Industrial Automation, Physical AI, Robot Fleets, Autonomous Mobility