{kind=link}

Global dependence on the internet is broad, but it remains uneven. Around 6 billion people were online in 2025, while 2.2 billion remained offline. Internet use reached 74% of the world’s population, up from 71% a year earlier, making access both a mature layer of social infrastructure and an unfinished development project. Mobile phones have become the de facto connection method for individuals, while robust connectivity networks now support much of the institutional work behind modern markets and public life.

Permanence changes the ecological test. A tool can be evaluated by usefulness. A permanent operating layer has to be evaluated by the resources it consumes, the dependencies it creates, and the public capacity it requires. The internet is here, in full swing, and locked into the fiber of humanity. Technology brings both good and bad impact. The positive side is that connection makes societies more aware of their problems and more capable of understanding them. The negative side is the immense resource consumption behind the digital systems now treated as normal life.

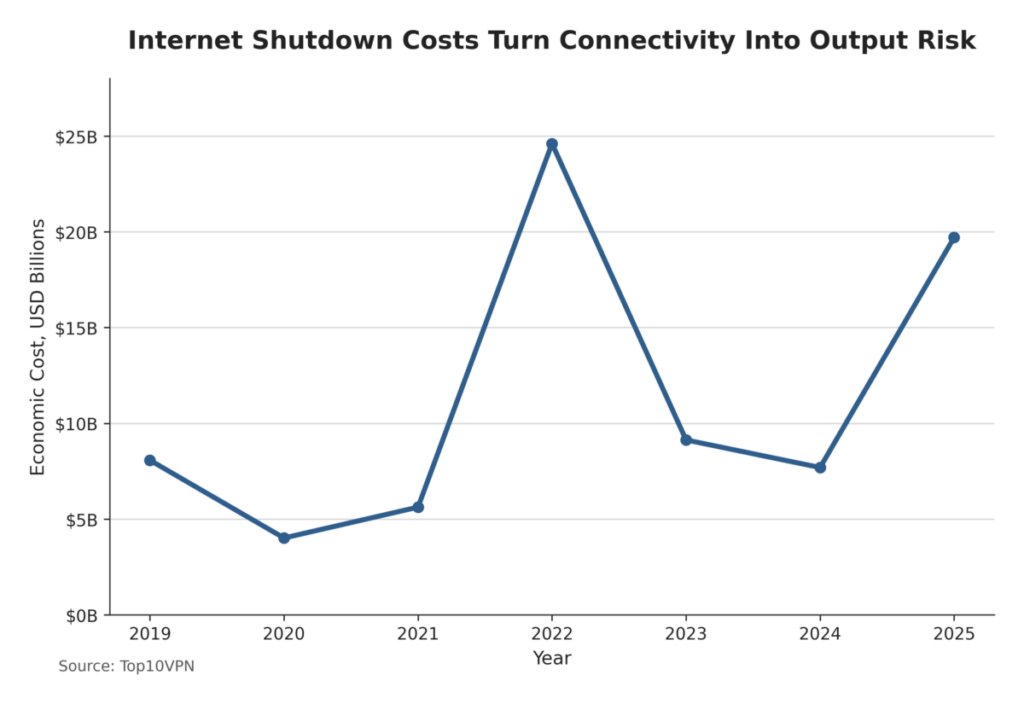

The internet now sits inside the machinery of economic life. It carries money movement and firm continuity while supporting public-service delivery, consumer access, institutional visibility, and the intelligence layer forming around AI. When the network fails, the damage no longer stays inside the technology sector. Government-imposed internet outages in 28 countries lasted more than 120,000 hours in 2025 and cost the global economy an estimated $19.7 billion, turning lost connectivity into a measurable loss of economic output. For firms and households, the practical effect is immediate: access to ordinary economic systems narrows.

By mid-2026, the story is no longer only about adoption or AI. It is about the physical balance sheet of the internet economy. Electricity consumption determines where computation can grow. Water usage has become part of the cooling, permitting, and trust equation. Carbon footprints are harder to simplify because operations, embodied emissions, hardware supply chains, and real-time grid use do not fit neatly inside one clean accounting frame. Rare earths and critical minerals tie digital growth to extraction and waste recovery. Pollution appears as emissions and as the material residue of discarded devices, packaging, logistics, and unrecovered inputs.

The same internet that creates those frictions also gives societies stronger ecological instruments. Smart farms can use connected sensors, irrigation data, and climate information to reduce waste and improve timing. Smart oceans can use satellite-linked vessel tracking and open marine data to make commercial activity more visible across waters that were once difficult to govern. Deforestation can be monitored at planetary scale, making ecological loss harder to hide even when enforcement remains uneven. The internet’s environmental story is therefore not a simple burden ledger. It is a test of whether digital intelligence can reduce ecological waste faster than digital expansion creates new claims on resources.

AI has pushed this bargain into public view. It is cementing itself into daily work and consumer behavior, but it requires exhaustive networks, immense processing power, and a rising environmental budget. Data centers consumed about 415 TWh of electricity in 2024, roughly 1.5% of global electricity use, and are projected to reach about 945 TWh by 2030. That does not make the internet a failed ecological project. It makes it a mature economic system with a physical balance sheet.

Mid-2026 marks the point at which internet ecology became an economics story. The question is no longer whether the internet has an ecological footprint. It clearly does. The question is whether the world can manage the power, water, mineral, carbon, pollution, and waste demands of a system that has become economically permanent while preserving the ecological intelligence that makes the internet valuable in the first place.

| Infrastructure Layer | Physical Requirement | Economic Constraint | Focus |

|---|---|---|---|

| Data Centers | High-volume electricity | Grid access | 415 TWh in 2024 |

| AI Compute | Dense processing capacity | Power availability | 945 TWh projected by 2030 |

| Cooling Systems | Heat and water management | Local permitting | Water becomes trust exposure |

| Hardware Supply | Chips, servers, and equipment | Embodied emissions | Scope 3 measurement gap |

| Siting | Land, interconnection, and tolerance | Public approval | Location becomes part of the product |

Sources: International Energy Agency; Uptime Institute

The Digital Economy Became A Physical Load

Digital growth now has an industrial footprint. It depends on facilities that draw power, manage heat, secure land, connect to grids, and rely on hardware supply chains that begin far outside the software market. For the user, the network can still feel abstract. For the economy, it is increasingly physical capital.

The power bill is now large enough to define the market. Data centers consumed about 415 TWh of electricity in 2024, equal to roughly 1.5% of global electricity use. By 2030, that demand is projected to reach about 945 TWh, nearly double the 2024 level and just under 3% of global electricity use. Demand rises about 15% a year from 2024 to 2030, more than four times faster than electricity demand growth across the rest of the economy. The digital economy is no longer only a software economy. It is becoming a power economy.

AI is the visible accelerator, but it is not the only source of demand. The broader internet economy has shifted more activity into remote computing and connected commercial infrastructure. Each additional layer increases demand for computation and data movement, while each efficiency gain must now compete against a market that keeps expanding its appetite.

Compute has become an industrial load rather than an abstract service. It is shaped by electricity contracts, grid capacity, cooling design, land access, and public tolerance. Power availability has become a competitive advantage. Grid access has become a market-entry condition. Location has become part of the product.

The Economics Of Ecological Constraint

Permission to scale now depends on ecological capacity. Companies with reliable electricity, fast interconnection, favorable siting, and resilient infrastructure can expand faster than competitors waiting behind grid queues or local resistance. Data center markets are no longer governed only by software demand. They are governed by the physical and political conditions that decide whether computation can grow.

Infrastructure drag now works through ecological constraint. It shapes which companies can grow, which regions can attract investment, and which customers absorb higher digital-service costs. Power scarcity converts compute into a rationed input. Water stress converts cooling into a permitting and community-cost exposure. Carbon disclosure turns sustainability from brand language into procurement eligibility.

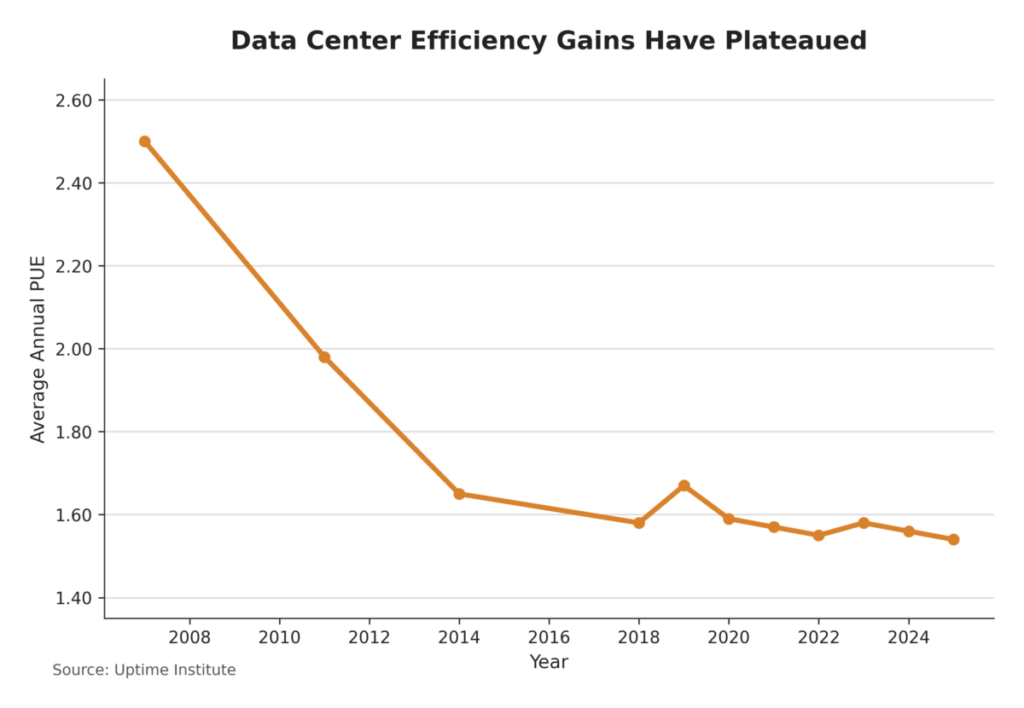

Efficiency gains still matter, but their easy phase has faded. Average data center power usage effectiveness remained around 1.56 in Uptime Institute’s 2024 survey, showing that headline facility efficiency has largely plateaued after earlier improvements. Better cooling and newer facility designs can still reduce waste. They cannot neutralize total electricity demand when computation grows faster than savings per unit.

Measurement has not caught up with the stakes. Only 18% of surveyed data center operators collected Scope 3 emissions data, even though construction, hardware, supplier energy, and equipment end-of-life can carry a major share of the digital footprint. Water is also a confidence liability, not just an engineering variable. Fewer operators collect water-use data than power data, weakening public trust in regions where cooling demand competes with local scarcity.

Ecological constraint does not end at the grid connection. The same growth model that increases demand for power also leaves a material trail through the devices that bring consumers online.

| Economic Function | Internet Role | Failure Exposure | Aligment |

|---|---|---|---|

| Payments | Carries digital transactions | Commerce interruption | Connectivity is transaction infrastructure |

| Firm Continuity | Supports remote operations | Output loss | Downtime becomes economic drag |

| Public Services | Enables digital delivery | Service access narrows | Network access is public capacity |

| AI Systems | Requires compute and data movement | Processing bottlenecks | Intelligence depends on infrastructure |

| Household Access | Connects users to economic systems | Participation loss | Digital exclusion remains development risk |

Sources: International Telecommunication Union; Top10VPN

Consumer Growth Became Material Waste

The consumer internet begins with access and ends with material residue. Mobile phones have become the de facto connection method for individuals, especially where fixed broadband is limited or unaffordable. The device is not just a screen. It is the material entry point into the network.

Every entry point has a lifecycle. Personal electronics and network hardware require extraction, manufacturing, shipping, electricity, repair, replacement, and disposal. The consumer internet grows through access, but access is delivered through objects that eventually become waste.

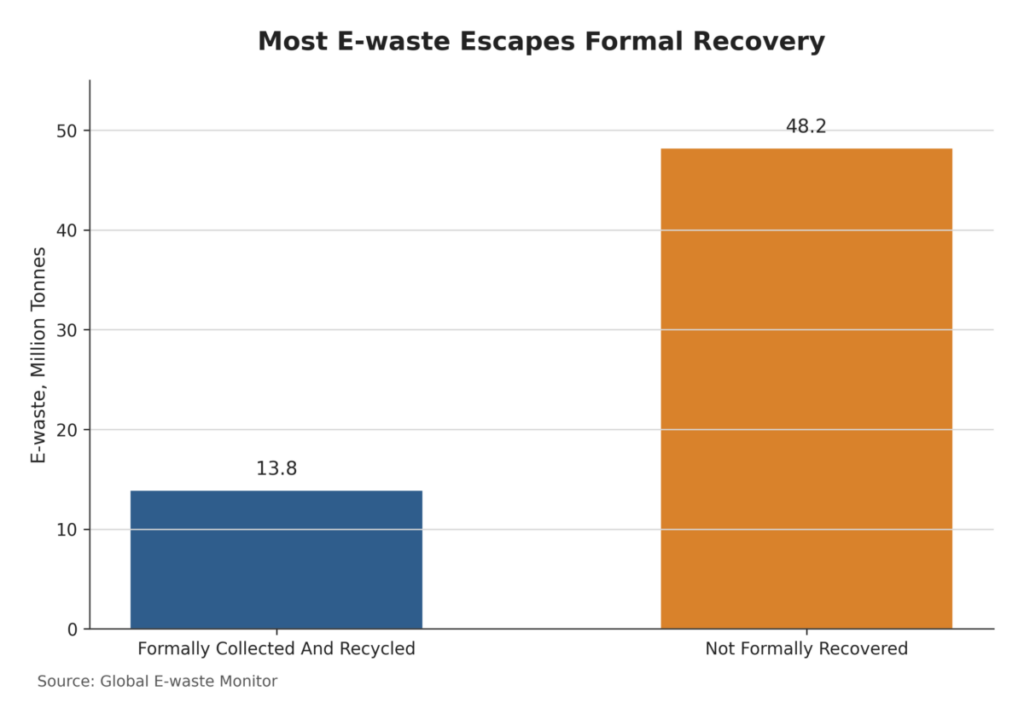

Global e-waste reached 62 million tonnes in 2022, up 82% from 2010. It is on track to reach 82 million tonnes by 2030. Only 22.3% was formally collected and recycled in 2022, which means most discarded electronics still move through weak, informal, or undocumented recovery channels. The scale is large enough to overwhelm easy metaphor: 62 million tonnes is the equivalent of 1.55 million 40-tonne trucks.

The weakness in internet ecology is that connection is sold as a service while much of its environmental burden appears later as physical waste. E-waste also represents stranded material value because recoverable metals leave the productive chain instead of returning to it. Device turnover therefore becomes both a pollution cost and a failure of residual-value recovery.

| Lifecycle Stage | Economic Function | Ecological Burden | Recovery Weakness |

|---|---|---|---|

| Device Production | Creates access hardware | Extraction and manufacturing | Materials start outside the user view |

| Network Use | Supports daily connectivity | Electricity demand | Costs are hidden in services |

| Device Turnover | Refreshes consumer capability | E-waste growth | Only 22.3% formally recycled |

| Digital Commerce | Improves discovery and payment | Packaging and reverse logistics | Efficiency depends on full operations |

| End Of Life | Returns value to supply chains | Pollution and stranded materials | Rare-earth recovery remains minimal |

Sources: Global E-waste Monitor; International Telecommunication Union

The Internet Became An Ecological Instrument

The same infrastructure that strains ecological capacity also improves ecological visibility. Environmental governance depends on measurement before it can depend on enforcement. Digital measurement has become a form of economic infrastructure because markets, regulators, and communities cannot manage what they cannot see.

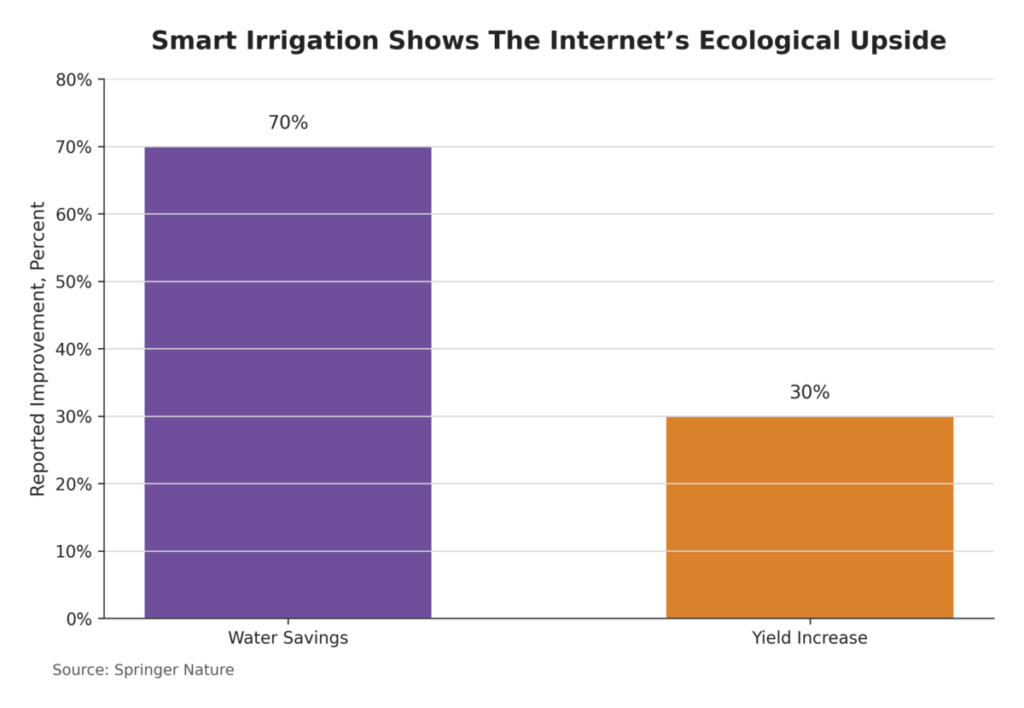

Connected agriculture shows the productive side of internet ecology. Internet-enabled irrigation can use soil and climate data to reduce waste and improve timing. A 2025 review of 56 studies found that IoT-enabled smart irrigation systems can deliver water savings of up to 70% and yield increases of 30% in studied deployments. The benefit is real when technology reduces physical waste rather than simply adding cost to already strained farming systems.

Forests show the same duality. Digital monitoring makes tree loss visible at planetary scale, but visibility does not equal protection. Global Forest Watch recorded 23 million hectares of natural forest loss in 2025, equivalent to about 9 Gt of CO₂ emissions. Tropical primary forest loss fell 36% from 2024 after a record fire year, showing both the volatility of the system and the value of continuous monitoring. Digital visibility makes ecological loss harder to hide. It still depends on enforcement, restoration, and economic pressure beyond the screen.

Oceans have become another frontier of internet ecology. Satellite-linked vessel tracking and open marine data have made commercial activity more visible across a space long treated as difficult to monitor. Industrial fishing occurs across roughly half of the ocean, yet more than half of fishing activity is concentrated in only 0.5% of ocean area. Data changes the governance problem by showing where attention matters most.

Internet ecology is therefore a resource-allocation question shaped by both consumption and intelligence. Environmental data matters most when it lowers waste, improves enforcement, changes market behavior, and directs capital toward lower-impact production.

That usefulness raises the standard rather than ending the argument. Once the internet becomes a tool for ecological intelligence, its own carbon, mineral, and governance claims become harder to treat as secondary costs.

| Ecological Domain | Digital Instrument | Economic Use | Governance Limit |

|---|---|---|---|

| Agriculture | Connected irrigation | Reduces water waste | Benefits depend on deployment quality |

| Forests | Satellite monitoring | Makes loss visible | Visibility does not guarantee protection |

| Oceans | Vessel tracking | Targets enforcement attention | Monitoring still requires jurisdiction |

| Carbon | Digital accounting | Improves disclosure | Boundaries remain inconsistent |

| Capital Allocation | Environmental data | Directs lower-impact investment | Data must change behavior |

Sources: Springer Nature; Global Forest Watch; Global Fishing Watch; World Bank

Ability and Permission To Scale

Credibility is now the internet’s mid-year test. Carbon accounting, critical minerals, and regulation determine whether digital growth can justify its next stage of expansion. Operational emissions are easier to measure than embodied emissions. Electricity use is easier to describe than chip fabrication. Renewable energy procurement is easier to advertise than real-time grid impact. Estimates of the ICT sector’s share of global carbon emissions vary from 1.5% to 4%, depending on boundaries and methodology, which shows how much the answer changes when lifecycle assumptions change.

Minerals create a related credibility problem. The internet depends on advanced electronics, and advanced electronics depend on critical materials that carry extraction, refining, trade, and environmental exposure. Demand for nickel, cobalt, graphite, and rare earths rose 6% to 8% in 2024, giving the digital economy a direct stake in mineral markets already shaped by energy transition demand and geopolitical concentration. The device feels clean at the point of use because the mine, refinery, and waste site are somewhere else.

The circular economy remains far from closing that loop. Only 1% of rare-earth element demand is met by e-waste recycling. That figure turns recycling from a moral preference into a strategic weakness. The digital economy depends on materials that it does not yet recover at meaningful scale.

Resource regulation has become internet governance. Europe has already moved in that direction through data center reporting rules for facilities with installed information-technology power demand of at least 500 kW. U.S. grid governance became a mid-2026 pressure point when federal regulators ordered all six regional grid operators to justify or reform tariffs for data centers and other large energy users.

These institutional moves are not peripheral compliance details. They show that internet growth is being absorbed into the operating logic of energy systems, permitting regimes, capital planning, and public cost allocation. Regulation now determines more than compliance. It determines market access, infrastructure timing, and public legitimacy. As internet infrastructure grows more resource-intensive, public policy will decide whether its costs remain private operating expenses, become public grid burdens, or are priced into the digital services that create the demand.

The case for internet technology remains strong. It can improve environmental awareness, strengthen climate intelligence, make ecological loss more visible, and expose inefficiency at scales that traditional inspection cannot match. The positive side of the thesis is real: as societies become more connected, they become more capable of understanding and solving shared problems. Those gains do not erase the resource bill, but they explain why the internet’s ecological future cannot be judged only by its footprint.

The negative side is just as real. Data center electricity demand is moving from about 415 TWh in 2024 toward a projected 945 TWh by 2030. E-waste is moving from 62 million tons in 2022 toward a projected 82 million tons by 2030. Internet use is moving toward universality while the remaining offline population still numbers in the billions. The internet’s footprint is not a side effect to be handled after growth. It is part of the growth model.

Mature internet infrastructure will not be judged only by speed, reach, intelligence, or convenience. It will be judged by whether it can keep expanding human capability without turning resource allocation, public legitimacy, and ecological capacity into the binding constraints on its own growth.

Key Takeaways

• Internet ecology became an economics issue because connectivity now functions as economic infrastructure.

• Internet outages created an estimated $19.7 billion in global losses in 2025.

• Around 6 billion people were online in 2025, while 2.2 billion remained offline.

• Data center electricity demand is moving from about 415 TWh in 2024 toward 945 TWh by 2030.

• Power availability and grid access are becoming market-entry conditions for digital infrastructure.

• Water stress is becoming a permitting and public-trust issue for data center growth.

• Global e-waste reached 62 million tonnes in 2022 and is projected to reach 82 million tonnes by 2030.

• Only 22.3% of e-waste was formally collected and recycled in 2022.

• Digital monitoring can improve irrigation, forest visibility, ocean governance, and carbon accountability.

• ICT emissions estimates vary from 1.5% to 4% because lifecycle boundaries remain inconsistent.

• Only 1% of rare-earth element demand is met through e-waste recycling.

• The internet’s next test is whether it can earn permission to scale within ecological and regulatory limits.

Sources

• International Telecommunication Union; Facts And Figures 2025; – Link

• Top10VPN; The Global Cost Of Internet Shutdowns In 2025; – Link

• International Energy Agency; Energy And AI; – Link

• Uptime Institute; Global Data Center Survey Results 2024; – Link

• Reuters; Texas Regulators Approve Framework To Manage Data Centers Power Demands; – Link

• Global E-waste Monitor; The Global E-waste Monitor 2024; – Link

• Springer Nature; Smart Drip Irrigation Systems Using IoT; – Link

• Global Forest Watch; Global Forest Dashboard; – Link

• Global Fishing Watch; Downloadable Fishing Effort Data; – Link

• World Bank; Measuring The Emissions And Energy Footprint Of The ICT Sector; – Link

• International Energy Agency; Global Critical Minerals Outlook 2025; – Link

• Federal Energy Regulatory Commission; FERC Launches Targeted Action To Speed Large Load Integration; – Link

Keywords: Earth And Ecology, Digital Infrastructure, Environmental Impact, Resource Allocation, Internet Economics